From pv magazine, October edition

Australia’s solar coaster headed south in the first half of 2019, as a perfect storm hit the industry. The first sign of trouble was the fallout when RCR Tomlinson was placed in voluntary administration in the second half of 2018. The downfall of the top utility-scale EPC contractor highlighted the construction and commissioning risks associated with PV development. Next came the New South Wales state election on March 23, 2019, in which the opposition Labor Party proposed a 50% renewable energy target by 2030, which would have been achieved through a series of reverse auctions. The party subsequently lost the election to the incumbent Liberal government, which has a zero net emissions target by 2050 and incentives for residential solar and batteries, but no utility-scale renewables incentives.

In the same month, the Australian Energy Market Operator (AEMO) published its first-round draft of Marginal Loss Factors (MLFs), which measure the impact of electricity losses along the network. However, there would be a second release in April before AEMO finalized them in June. The industry took another whack, with six solar farms in New South Wales and Victoria having their MLFs reduced by more than 10%, highlighting the risk of grid congestion.

Who’s who

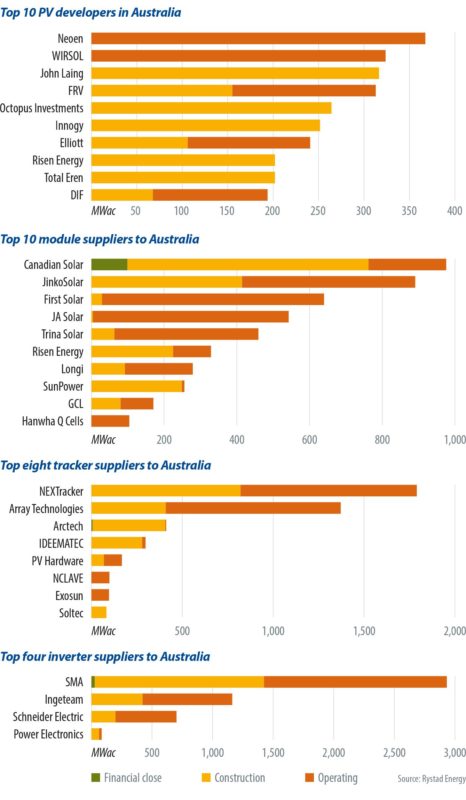

The boom in the utility-scale PV industry has attracted local and foreign participants across the industry’s entire value chain. The list of the top 10 utility-scale developers (see chart below) is a dynamic and rapidly changing one, as new, bigger projects have broken ground, particularly in the last 12 months. Neoen has been very active in the Australian market, commissioning five utility-scale PV farms in 2018, all in New South Wales, with a combined capacity of just over 250 MW (AC). In 2019, Neoen commissioned a further 100 MW of PV in particularly in the last 12 months in Numurkah, Victoria. The French developer also tops the list of lithium-ion battery developers and ranks within the top 10 wind developers.

Familiar names make up the top 10 module suppliers to the utility-scale PV market in Australia. Canadian Solar takes the top spot, as it is currently supplying modules to several large-scale projects including Darlington Point (275 MW), Kiamal stage 1 (200 MW) and Finley (133 MW). JinkoSolar is a close second, as it has supplied the 200 MW Maoneng Sunraysia project and all of the utility-scale PV in South Australia (Bungala Phase 1 and 2 and Tailem Bend).

The majority of utility-scale solar farms in Australia utilize single-axis tracking to minimize their LCOE. Although this may seem obvious in the Australian market, single-axis tracking has yet to take off in neighboring markets such as Malaysia, the Philippines or Vietnam. The tracker supplier market is dominated by Nextracker and Array Technologies, but in the past 18 months, several new companies have entered the market, including Arctech Solar, Ideematec, Exosun and Soltec.

Popular content

The inverter market is by far the most concentrated of the major segments. SMA currently has a 60% market share, while second-place Ingeteam controls 23% of the market. The remainder is mostly covered by Schneider Electric (15%), which pulled out of the utility-scale inverter business earlier in 2019, and Power Electronics, which has supplied two projects in Queensland (Rugby Run Stage 1 and Barcaldine).

Short-term hurdles

The renewables industry went through a record period of construction and commissioning activity in 2018-19, transitioning from a megawatt-scale market to a gigawatt-scale one. Moving forward, the industry will grapple with the challenges surrounding transmission constraints and securing offtake. Yet positives remain, including recently announced reverse auctions from the Australian Capital Territory, AEMO ISP Group 1 investments (synchronous condensers in South Australia, congestion reduction in Northwest Victoria and interconnection upgrades), five-minute settlements coming in 2021, and the shutdown of the 500 MW Liddell coal power station in 2022-23.

Bright future

There is no denying that predicting the future even just one or two years ahead is challenging. The key challenges of simply getting enough transmission capacity built to get renewable generation to load remains, as well as a political environment that is less than favorable toward renewable energy. However, a whole host of positive factors will drive longer-term growth. These include a massive number of projects that have yet to break ground (>100 GW), the continuously improving economics of PV/wind/storage, the retirement of coal and the high price of gas. Most notably, the declining cost of lithium-ion batteries has led to the pipeline expanding from less than 2 GW at the start of 2018 to more than 11 GW at the time of writing. The cost reductions of lithium-ion batteries are being driven by mass manufacturing, mainly in China, for use in electric vehicles. Their cost reductions will begin the next big wave of firmed renewables, which is expected to start in the early 2020s.

About the author

David Dixon has an undergraduate degree in Petroleum Engineering, with a Masters of Photovoltaic Engineering from the University of New South Wales. He has seven years of experience in the energy industry (upstream oil/gas and solar), with Shell, Woodside and Solgen Energy. He joined Rystad Energy in 2018 as a renewables analyst covering the Australian market and is based in Rystad’s Sydney office.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.