New annual PV installations give an important indication of the size of the pool of operating assets that are available for M&A deals today, and that will be available for future M&A deals.

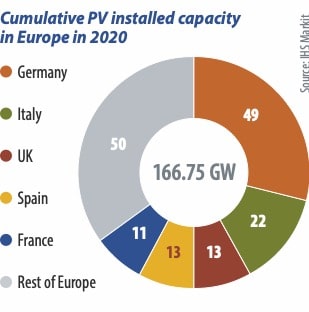

Europe saw a renaissance in 2019, when more than 24 GW of PV was installed – almost double 2018 installations. As a result, the cumulative installed PV capacity in Europe surpassed 150 GW in 2019. Nearly 40% of the capacity added in 2019 is from utility-scale solar projects greater than 20 MW. New installations are set to surpass 20 GW in 2020, with Germany and Spain accounting for 36% of the capacity additions.

Moreover, throughout the past decade, PV installations in Europe have been supported by feed-in tariffs and green certificates, and lately by tenders and PPAs, making these assets attractive to investors in the M&A market today.

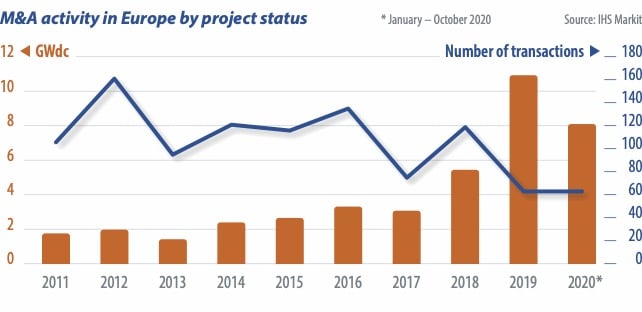

Major increase

Over time, the number of MWs transacted in the European PV market has increased. In 2019 and 2020, around 19 GW of assets or pipelines were transacted. However, the number of transactions has generally decreased, as larger PV plants or pipelines are being transacted.

Until 2017, the majority of transactions focused on operating assets installed under feed-in tariffs and green certificate schemes. To give a few examples, the United Kingdom’s Renewable Obligation Certificate (ROC) program made U.K. assets an attractive investment option up to 2017. Several U.K. assets were transferred multiple times from pre-construction to operation and have then been acquired further by companies that seek to consolidate their positions in the market. In Italy, many operating assets are benefitting from previous support schemes such as Conto Energia – therefore also attracting abundant M&A activity. A large portion of French operating assets were supported by generous feed-in tariffs and subsequently by tenders. Therefore, they have also been the focus of many M&A deals throughout the last decade.

The situation changed in 2018 when investors started buying project pipelines in anticipation of a renaissance of the European PV market.

Spain surges

Spain continues to dominate the 2019-20 M&A landscape for both operating assets and pipelines, with around 9.4 GW of assets transacted over the last two years.

Specifically, Spanish pipelines accounted for 68% of all early-stage pipeline transaction in Europe between 2019 and 2020, due to the size of its utility-scale market in 2019-20 and its expected growth in the next five years, which make it a key target market. Notable Spanish pipeline transactions include the 1.5 GW Bester Generacion pipeline acquisition by InfraRed Capital Partners in 2019 and the 1.2 GW pipeline acquisition by Total from Solarbay in 2020.

Popular content

Spain was also the largest target country for deals involving advanced-stage projects (operating, under construction, and permitted assets). Spanish assets accounted for 39% of all assets transacted in Europe over the past two years. Most of the transacted assets in Spain were built in 2019 or targeting completion in 2020 and 2021. For example, the Galp-ACS deal at the beginning of this year involved around 900 MW of projects in operation. Also in 2020, China Three Georges agreed to acquire around 500 MW of operational projects in Spain from developer X-Elio.

The Iberian country has nearly 11 GW of cumulative installed PV capacity. It had the highest annual installed PV capacity in 2019 of 5 GW – an impressive market revival after years of stagnation. It also has a significant amount of solar pipeline activity and assets under development, making it one of the top target countries for M&A deals.

Ireland enters

A new market attracting attention in 2020 is Ireland. It recently had its first renewable energy auction, which saw around 800 MW of solar PV projects assigned as part of the Renewable Electricity Support Scheme (RESS). This resulted in several acquisitions as international players entered the market. One of the largest deals includes Statkraft acquiring 275 MW of permitted assets owned by Lightsource BP, as well as several projects from local developer JBM, accounting for more than 300 MW. Four more rounds of the RESS auction will take place in the following years, so further acquisitions are expected as the solar PV market in Ireland finally takes off.

Selling to utilities

Similar to previous years, developers, EPCs, and IPPs were the major PV asset sellers in 2019 and 2020, and a significant portion of assets sold were pipelines. One of the biggest transactions was Spanish Bester Generacion’s sale of its Spain portfolio of projects, around 1.5 GW, to InfraRed Capital Partners, a global investment manager focused on infrastructure and real estate. And French PV company Urbasolar was also acquired by Swiss company Axpo. Urbasolar’s portfolio includes a 1 GW pipeline.

The top PV asset buyers for 2019 and 2020 are utilities, followed by IOCs and financial companies, and the top 10 buyers account for 60% (11 GW) of all M&A activity. The analysis upon which this article is based includes transactions up to October 2020. But the percentage of activity captured by the top 10 buyers increases significantly once the November deal between Statkraft and Solarcentury is taken into account.

In the last two years, European PV markets saw record numbers for M&A transactions in GW terms. IHS Markit expects the positive M&A trend to continue over the coming years, as the majority of European markets transition away from wide-spread support schemes, and investors continue being optimistic about the resiliency of the sector.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.