US southeastern states take the lead in utility-scale solar as interconnection queues swell to 188 GW (w/charts)

Regions outside of California and the Southwest accounted for the lion’s share at 70% of all new utility-scale PV capacity additions in 2017, according to the new Utility Scale Solar report from Lawrence Berkeley National Laboratory (LBNL).

The Southeast accounted for 40% of all new utility-scale solar capacity in 2017. “Particularly strong showings came from the established player North Carolina (at 16%, with 20 projects in the 10-80 MWAC range), followed by Virginia, South Carolina, Florida, and Mississippi,” reads the report. Texas installed 17% of new utility capacity nationwide, while California maintained the lead at 20% of the national total. According to the report, utility-scale plants accounted for nearly 60% of all new solar capacity in 2017.

These regional trends are reflected in Figure 3, showing cumulative solar installations at year-end 2017, mapped against solar irradiance.

The report also showed 188.5 gigawatts (GW) of solar power capacity (including a small amount of concentrating solar power) within the interconnection queues, which is more than eight times the installed utility-scale solar power capacity in all the projects that LBNL has found in its study. Of that amount, 99.2 GW of solar capacity entered the queues in 2017—“the most ever”—with the Midwest queues growing the most, by 27 GW.

The report notes that not all of that capacity will be built, and shows the breakdown by region and growth since 2014 in Figure 29.

Reflecting on a decline in wholesale pricing for solar generation in California, the report notes that adding battery storage is one way to at least partially restore the value of solar. It also notes that three recent PV plus storage PPAs in Nevada (each using 4-hour batteries sized at 25% of PV nameplate capacity) suggests that the incremental PPA price adder for storage has fallen to ~$5 per megawatt-hour (MWh).

“Interest has grown both among utility offtakers (many of which now encourage all PV proposals to include a storage option) and developers (a number of which have made it standard practice to always provide a storage option),” states LBNL.

In a table below, titled “Utility-scale PV plus battery storage is on its way to becoming the ‘new normal,’” the report provides data on 16 utility-scale solar-plus-storage projects, up from four last year, noting that “many more such projects are still in the early development phase and/or making their way through solicitations.”

Meanwhile, storage capacity in the interconnection queues grew to 18.9 GW.

The LBNL analysis also showed that for utility-scale solar, median installed prices fell to $2.0/W-AC (or $1.6/W-DC) for projects completed in 2017. Prices for the lowest 20th percentile of projects were at or below $1.8/W-AC, with some as low as $0.9/W-AC. The price distribution for projects narrowed compared to prior years, as shown in Figure 9.

Installation prices varied by region. But one thing that did not vary as much was the popularity of trackers, with single-axis trackers used in nearly 80% of 2017 installations. Remarkably, projects using single-axis trackers had slightly lower prices than fixed-tilt installations, as shown in Figure 10.

The median inverter loading ratio rose to 1.32, which the report notes allowed the inverters to operate closer to (or at) full capacity for a greater percentage of the day. LBNL also found that in the future the increasing deployment of DC-coupled battery storage may continue to push the ratio of a project’s DC module array nameplate rating to its AC inverter nameplate rating higher.

Operations and maintenance (O&M) costs, from a limited sample, were about $16 per kW-AC per year, or $8 per MWh.

The average capacity factor was 27.6% on a capacity-weighted basis, about the same as in 2013, as an ongoing increase in the prevalence of tracking has been offset by a build-out of lower-resource sites. Capacity factors for cumulative installations varied by region and by whether tracking is used, as shown in Figure 15.

Most power purchase agreements (PPAs) nationwide were priced “at or below $40/MWh levelized (in real 2017 dollars), with a few priced as aggressively as ~$20/MWh.”

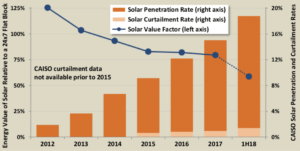

When solar is sold on the wholesale market, California solar generation has pushed down mid-day wholesale power prices and thus earned just 79% of the average price across all hours within CAISO’s real-time wholesale energy market, as shown in the graph below. Meanwhile, the report found that in other markets with less solar penetration, solar’s hourly generation profile still earned more than the average wholesale price across all hours.

The report includes a section headlined “Solar’s largely non-escalating and stable pricing can hedge against fuel price risk,” that includes price projections for solar PPAs and natural gas prices, which illustrates that solar is becoming price-competitive with gas. Based on future projected gas costs by the U.S. Department of Energy’s Energy Information Administration (EIA), the report expects the median solar PPA prices to beat out the reference case price of natural gas around 2036.

The report compiled 2017 data on 146 utility-scale PV projects—those above 5 MW-AC—totaling 3.9 GW-AC, bringing the cumulative total to 590 projects totaling 20.5 GW-AC. This includes four states—Michigan, Mississippi, Missouri, and Oklahoma—that added their first utility-scale PV projects in 2017, bringing the total to 33 states that are now home to utility-scale solar projects.

Utility-Scale Solar: Empirical Trends in Project Technology, Cost, Performance, and PPA Pricing in the United States—2018 Edition was written by LBNL staff members Mark Bolinger and Joachim Seel.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment