Fitch predicts a decade of corporate renewable power procurement growth in the US

From pv magazine USA.

There are numerous positive projections suggesting significant volumes of solar power will be deployed across the United States in the coming years. Existing state laws will be expected to drive an estimated 73 GW of renewables generation capacity through the end of the decade, there are hundreds of gigawatts more waiting in grid operator queues through the end of 2023 and of course there is the fact renewable energy is about the cheapest electricity source – and getting cheaper.

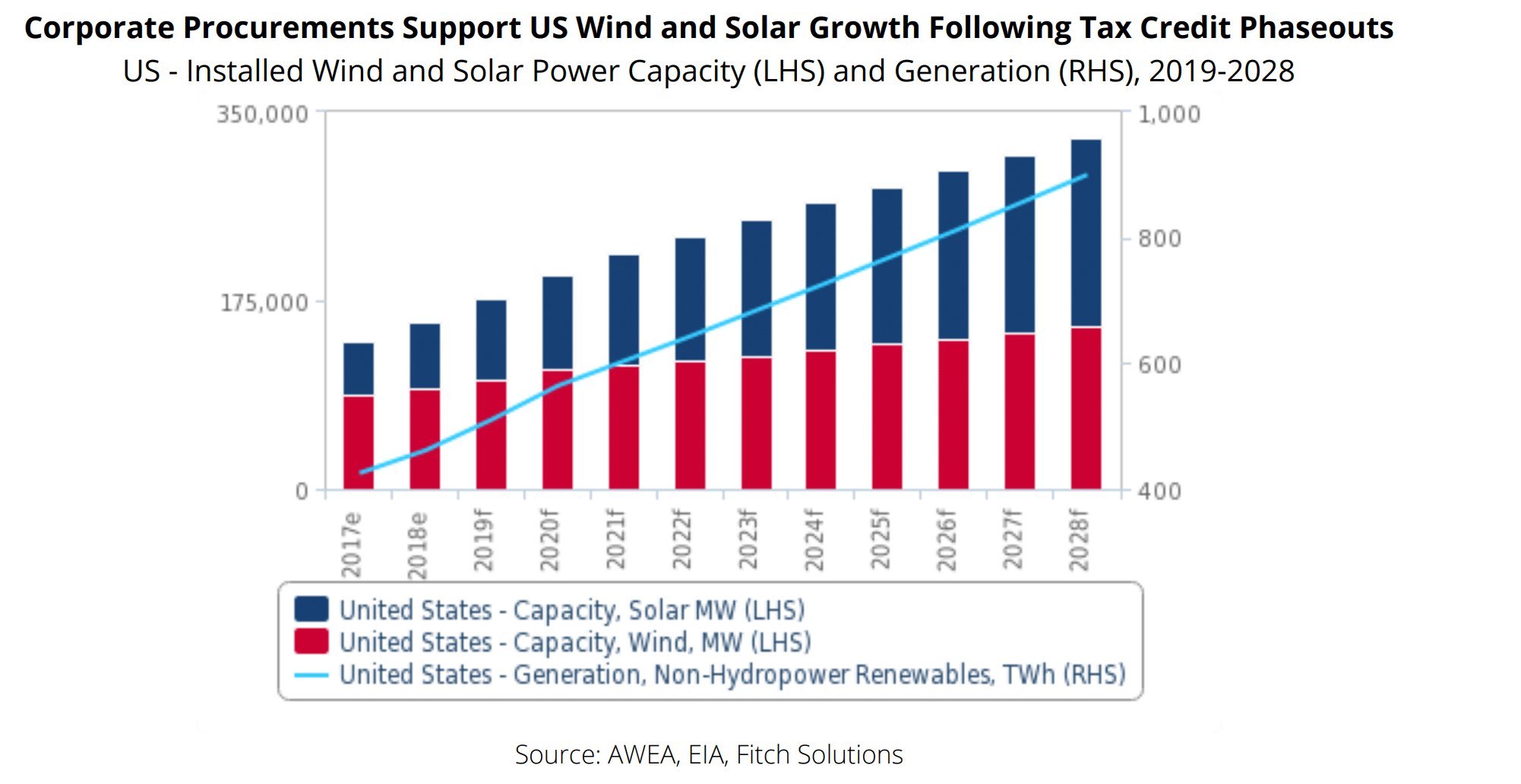

Fitch Solutions’ 10-year forecasts for the U.S. solar and wind power sectors anticipate capacity growth will average 7.9% and 3.9%, respectively, between 2022 and 2028 – with upward revisions likely as more corporations commit to renewable electricity targets and the procurement process is simplified.

As a whole (see chart below) Fitch sees U.S. renewables generation capacity rising from around 175 GW at the end of the year to just short of 1 TW in 2028. That will mean clean power generation of just over 400 TWh in 2017 will hit more than 900 TWh in nine years’ time. To put that into context, U.S. electricity use has remained steady at just short of 4 PWh for around a decade.

Fitch cites two sources for its historical data. The Rocky Mountain Institute thinktank has recorded 15.5 GW of renewables capacity from solar and wind between 2014 and last year. Business intelligence company BloombergNEF said U.S. companies procured 5.9 GW in the first half of this year – not far off the 6.5 GW bought in all of last year.

Fitch sees solar likely overtaking wind as it can more often be installed on site, has a more favorable tax credit phase-out schedule and its peak generation hours more closely align with the demand profile for many companies.

As pv magazine USA has noted, power purchase agreements (PPA) for solar have become more varied. Fitch suggested developers would increasingly seek corporate PPAs to diversify revenue, to contract with creditworthy corporate buyers and – through multi-buyer PPAs – to diversify payment default risk. The increasing flexibility offered by PPAs, such as five to ten-year terms and multiple off-takers, will only make them more attractive to commercial energy buyers.

The report noted Engie expects half its renewables projects between 2019 and 2021 to come from PPAs with companies or cities. The French power company has signed 3 GW of corporate PPAs with U.S. customers including Target, Boston University and T-Mobile.

Over the course of the period studied, solar procurement is projected to peak at just short of 15 GW in 2021 and then tail off toward 10 GW per year through 2028 – for around 117 GW of total capacity by the end of 2028.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment

[…] Source: https://www.pv-magazine.com/2019/09/19/fitch-predicts-a-decade-of-corporate-renewable-power-procurem… […]