European B2C photovoltaic market lacks truly dominant players

Many market studies rely on estimates, secondary sources and proxies, though this is rarely disclosed as transparently as in the Solarmonitor, from the Center for Sustainable Transformation at Quadriga University of Applied Sciences in Berlin.

Now in its third edition, the report covers the European B2C market for photovoltaic systems and related technologies including heat pumps and energy management systems. While it aims to identify leading providers in the sector, the authors note that the underlying data remains “inconsistent and partially incomplete.”

The main reason is limited willingness among providers to share information. Responses were often missing data or explicitly declined, the study states. As a result, estimates were required in several cases, alongside data drawn from press releases, media reports and company websites.

The study highlights structural challenges in market segmentation. Large companies such as France’s EDF, for example, report photovoltaic revenues but do not separate residential and commercial segments. For players including Enerix, Energieversum, and 1Komma5°, the number of newly installed systems in the 2025 reporting year is either estimated or not available.

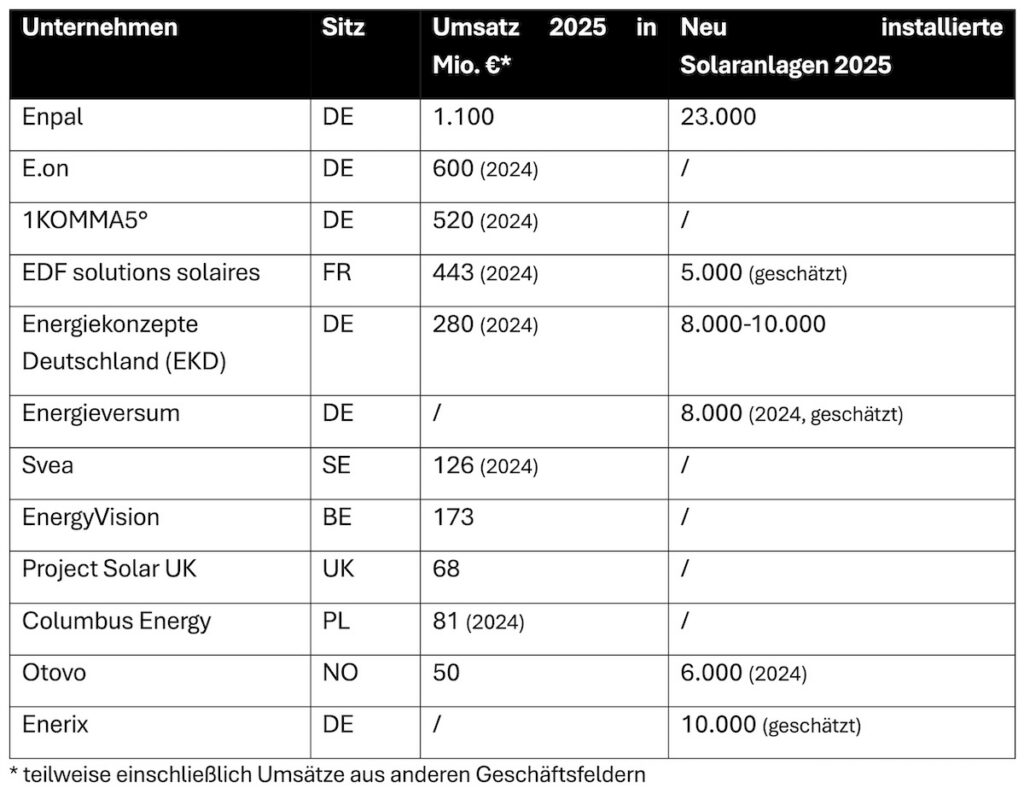

With these limitations, the study derives a list of the largest European B2C providers, led, as in the previous year, by Enpal, E.ON and 1Komma5°. EDF Solutions Solaires is the first non-German player in the ranking, placing fourth.

Large players with small market shares

The Solarmonitor covers twelve B2C solar companies. It also includes chapters on the five largest residential heat pump providers: Enpal, Thermondo, Octopus Energy, 1Komma5° and Aira.

The analysis concludes that, despite consolidation trends, “there are still no companies with a truly dominant Europe-wide market share.” In Germany, the top ten providers account for only around 14% to 17% of the B2C market combined, based on 2024 data, with market leader Enpal holding no more than 4%. Comparable Europe-wide data, however, is not sufficiently robust.

Diversification of offerings and consolidation through acquisitions or strategic investors – such as Pemberton’s investment in German company EKD in March 2025 – are two typical reactions to the fact the residential market has shrunk significantly since 2023, even for major players. The Solarmonitor defines another reaction as strategic realignment through increased cooperation with local installers, a strategy Enpal has been pursuing strongly since 2025.

The study states elsewhere that the latter is not solely due to the reduced market volume, which also affects smaller players. “Installation business is inherently local-intensive: sales, planning, installation and service require physical presence and customer trust, which favors local brands,” the report reads.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment