Module Price Index: 2020 – Taking the time to say ‘thanks’…

From pv magazine 01/2021

Back in early 2019, module manufacturer Hanwha Q Cells revealed that it had filed a patent lawsuit on three continents against competitors Longi Solar, JinkoSolar, and REC. A little more than a year later, in July 2020, the courts handed down their first rulings. In the United States, the lower court ruled against the plaintiff, but in Germany it ruled in the plaintiff’s favor. The judges granted Hanwha Q Cells an injunction, to which all defendants immediately appealed. JinkoSolar alone had affirmed from the beginning of the proceedings that the products it currently supplied were not affected by the lawsuit. The other two competitors remained tight-lipped in this regard. Nevertheless, the same companies took precautionary measures to at least limit the damage should the ruling be upheld. Longi Solar temporarily halted shipments of certain products, while REC reduced its product range to the Alpha series.

In November, there was some further movement in the dispute after the Chinese patent office rejected nullification proceedings initiated by Longi Solar in late 2019. However, the office only reviewed the legal validity of the two patents at issue in China and declared them partially invalid. Currently, a review before the European Patent Office is also in progress, but its final decision is still pending. Longi Solar wants to prevent the initiation of additional “needless” patent lawsuits. This dispute will therefore drag on for a while, and the outcome remains uncertain.

In November, there was some further movement in the dispute after the Chinese patent office rejected nullification proceedings initiated by Longi Solar in late 2019. However, the office only reviewed the legal validity of the two patents at issue in China and declared them partially invalid. Currently, a review before the European Patent Office is also in progress, but its final decision is still pending. Longi Solar wants to prevent the initiation of additional “needless” patent lawsuits. This dispute will therefore drag on for a while, and the outcome remains uncertain.

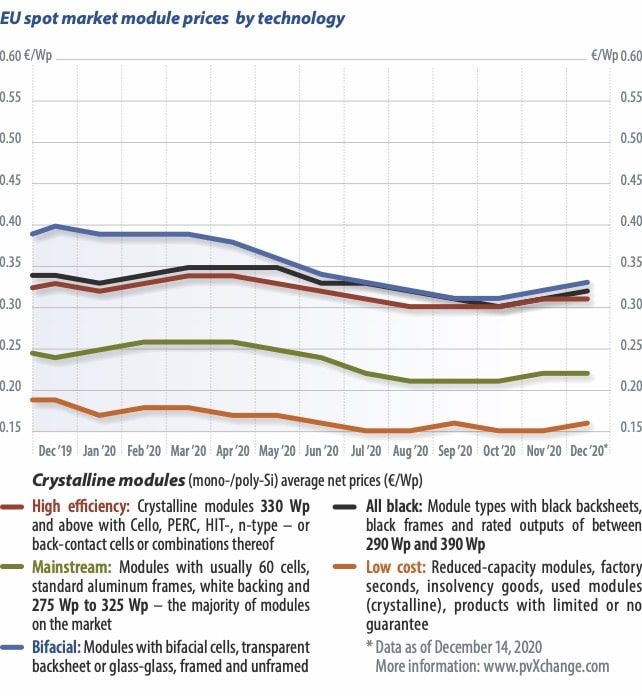

August

In August and September, module prices across the board reached all-time lows. For projects in the megawatt range, prices well below $0.18 were no longer the exception, even for monocrystalline modules. Following pandemic-related shutdowns in the spring, most PV manufacturers had resumed normal production operations. Raw material prices for silicon wafers and solar glass were also moderate, and the dollar exchange rate was balanced. However, this was to change significantly in the months that followed.

Driven by the chaos of an out-of-control Covid-19 pandemic in the United States and by President Donald Trump, the dollar exchange rate continued its slide. This exchange rate weakness made dollar-based solar panels from China somewhat cheaper. In addition, there is currently a shortage of polysilicon and solar glass. By the end of the year, manufacturers had already made several upward price adjustments of 10% or more. This trend will probably not reverse until the second quarter of 2021.

October

In the fourth quarter, the question was whether Covid-19 would leave its mark on the PV industry in 2020. There were studies indicating that up to 15% of all renewable energy projects in Europe were delayed or failed completely due to the crisis. However, this assessment mainly applied to medium and large-scale projects, often with transregional participation. In Germany, the government responded by extending the completion deadlines for tenders awarded by up to six months.

In the small to medium-sized PV systems sector, there was scarcely any discernible negative impact resulting from the pandemic, at least in Germany. Particularly systems combining PV with energy storage and/or charging infrastructure for e-mobility enjoyed growing popularity. Many consumers seemed to want to increase their level of self-sufficiency using their own solar power system at a high self-consumption rate. This provided full order books for many solar installers, who have been and continue to be among the winners in the crisis.

November

For exactly 20 years, we have known that the first PV systems to be subsidized under Germany’s Renewable Energy Sources Act (EEG) would cease to be eligible for compensation from the grid operator on Jan. 1, 2021, after 20 years in operation. Nevertheless, the German government has not managed to present a consensus-worthy follow-up regulation in time. This and a number of other important issues were supposed to be addressed by the amendment to the law, which was to take effect in 2021 and finally passed in November. The bill presented to the public by the German coalition parties in September was an unambitious, half-baked draft that triggered widespread indignation in the industry. Introduced without comprehensive changes, it threatens not only a collapse in installation figures, but also the loss of existing PV capacities. The continued operation of plants coming up on their 20-year mark would simply be uneconomical for many operators.

Since the introduction of the draft, associations, the opposition, and the governing coalition have been discussing the far-too-modest expansion targets, excessive measurement and regulation requirements, the counterproductive EEG surcharge for small systems, the extension of the tendering obligation to smaller PV systems, as well as the treatment of 20-year-old, or post-EEG, systems. An end has been in sight since Dec. 14, and at least some improvements are in the offing. We were all waiting with bated breath for the final text of the law.

Outlook

Our two strong German women in Berlin and Brussels, Angela Merkel and Ursula von der Leyen, are standing up to the political machos elsewhere in the European Union and trying to implement the principles of the rule of law, a humane refugee policy, and more ambitious climate targets, through the Green Deal, for instance, to the extent politically possible at the moment. The issue of climate change has not completely dropped off the radar, despite the pandemic. Instead, parallels are pointed out and appeals are made to common sense and for people to listen to science much more closely than in the past when prioritizing measures and combating crises. Ultimately, the Covid-19 protection measures, the restrictions up to and including the hard lockdown, have made everyone around the world aware of what is important and what we can do without, if necessary, permanently.

Our Western society – no, the entire human race – is unlikely to be the same before the crisis once the pandemic has been dealt with, which will hopefully proceed apace in the coming year. Business and politics will also no longer fall back into their old, outdated patterns; I am optimistic about that. We will rethink many things, doing them differently and hopefully better as a result. This is an opportunity that has been given to us unexpectedly and that we should urgently take advantage of. For that I would just like to say, thank you!

Read previous module price indexes

About the author

Martin Schachinger has been active in the field of photovoltaics and renewable energy for more than 20 years. In 2004 he founded the internationally renowned online trading platform pvXchange.com, where wholesalers, installers, and service companies can purchase standard components, solar modules, and inverters that are no longer manufactured but are urgently needed to repair defective PV systems.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment