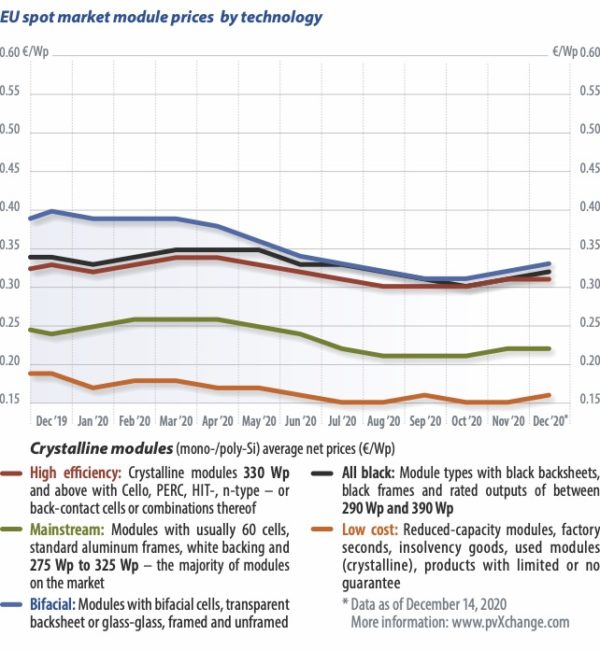

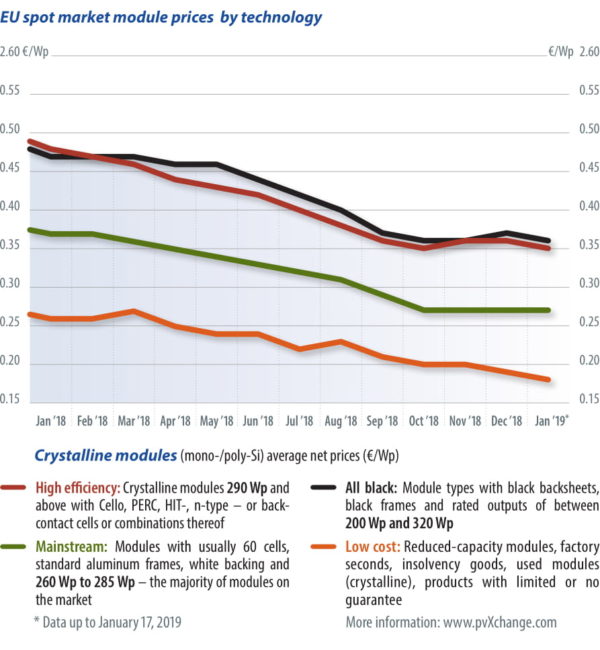

January 2021: 2020 – Taking the time to say ‘thanks’…

Alongside all of the problems, 2020 has brought us a few promising initiatives and developments. Martin Schachinger of pvXchange.com looks back over the second half of the year and offers a quick look at what could be in store for 2021.

Alongside all of the problems, 2020 has brought us a few promising initiatives and developments. Martin Schachinger of pvXchange.com looks back over the second half of the year and offers a quick look at what could be in store for 2021.

Back in early 2019, module manufacturer Hanwha Q Cells revealed that it had filed a patent lawsuit on three continents against competitors Longi Solar, JinkoSolar, and REC. A little more than a year later, in July 2020, the courts handed down their first rulings. In the United States, the lower court ruled against the plaintiff, but in Germany it ruled in the plaintiff’s favor. The judges granted Hanwha Q Cells an injunction, to which all defendants immediately appealed. JinkoSolar alone had affirmed from the beginning of the proceedings that the products it currently supplied were not affected by the lawsuit. The other two competitors remained tight-lipped in this regard. Nevertheless, the same companies took precautionary measures to at least limit the damage should the ruling be upheld. Longi Solar temporarily halted shipments of certain products, while REC reduced its product range to the Alpha series.

In November, there was some further movement in the dispute after the Chinese patent office rejected nullification proceedings initiated by Longi Solar in late 2019. However, the office only reviewed the legal validity of the two patents at issue in China and declared them partially invalid. Currently, a review before the European Patent Office is also in progress, but its final decision is still pending. Longi Solar wants to prevent the initiation of additional “needless” patent lawsuits. This dispute will therefore drag on for a while, and the outcome remains uncertain.

August

In August and September, module prices across the board reached all-time lows. For projects in the megawatt range, prices well below $0.18 were no longer the exception, even for monocrystalline modules. Following pandemic-related shutdowns in the spring, most PV manufacturers had resumed normal production operations. Raw material prices for silicon wafers and solar glass were also moderate, and the dollar exchange rate was balanced. However, this was to change significantly in the months that followed.

Driven by the chaos of an out-of-control Covid-19 pandemic in the United States and by President Donald Trump, the dollar exchange rate continued its slide. This exchange rate weakness made dollar-based solar panels from China somewhat cheaper. In addition, there is currently a shortage of polysilicon and solar glass. By the end of the year, manufacturers had already made several upward price adjustments of 10% or more. This trend will probably not reverse until the second quarter of 2021.

October

In the fourth quarter, the question was whether Covid-19 would leave its mark on the PV industry in 2020. There were studies indicating that up to 15% of all renewable energy projects in Europe were delayed or failed completely due to the crisis. However, this assessment mainly applied to medium and large-scale projects, often with transregional participation. In Germany, the government responded by extending the completion deadlines for tenders awarded by up to six months.

In the small to medium-sized PV systems sector, there was scarcely any discernible negative impact resulting from the pandemic, at least in Germany. Particularly systems combining PV with energy storage and/or charging infrastructure for e-mobility enjoyed growing popularity. Many consumers seemed to want to increase their level of self-sufficiency using their own solar power system at a high self-consumption rate. This provided full order books for many solar installers, who have been and continue to be among the winners in the crisis.

November

For exactly 20 years, we have known that the first PV systems to be subsidized under Germany’s Renewable Energy Sources Act (EEG) would cease to be eligible for compensation from the grid operator on Jan. 1, 2021, after 20 years in operation. Nevertheless, the German government has not managed to present a consensus-worthy follow-up regulation in time. This and a number of other important issues were supposed to be addressed by the amendment to the law, which was to take effect in 2021 and finally passed in November. The bill presented to the public by the German coalition parties in September was an unambitious, half-baked draft that triggered widespread indignation in the industry. Introduced without comprehensive changes, it threatens not only a collapse in installation figures, but also the loss of existing PV capacities. The continued operation of plants coming up on their 20-year mark would simply be uneconomical for many operators.

Since the introduction of the draft, associations, the opposition, and the governing coalition have been discussing the far-too-modest expansion targets, excessive measurement and regulation requirements, the counterproductive EEG surcharge for small systems, the extension of the tendering obligation to smaller PV systems, as well as the treatment of 20-year-old, or post-EEG, systems. An end has been in sight since Dec. 14, and at least some improvements are in the offing. We were all waiting with bated breath for the final text of the law.

Outlook

Our two strong German women in Berlin and Brussels, Angela Merkel and Ursula von der Leyen, are standing up to the political machos elsewhere in the European Union and trying to implement the principles of the rule of law, a humane refugee policy, and more ambitious climate targets, through the Green Deal, for instance, to the extent politically possible at the moment. The issue of climate change has not completely dropped off the radar, despite the pandemic. Instead, parallels are pointed out and appeals are made to common sense and for people to listen to science much more closely than in the past when prioritizing measures and combating crises. Ultimately, the Covid-19 protection measures, the restrictions up to and including the hard lockdown, have made everyone around the world aware of what is important and what we can do without, if necessary, permanently.

Our Western society – no, the entire human race – is unlikely to be the same before the crisis once the pandemic has been dealt with, which will hopefully proceed apace in the coming year. Business and politics will also no longer fall back into their old, outdated patterns; I am optimistic about that. We will rethink many things, doing them differently and hopefully better as a result. This is an opportunity that has been given to us unexpectedly and that we should urgently take advantage of. For that I would just like to say, thank you!

Martin Schachinger

Martin Schachinger has been active in the field of photovoltaics and renewable energy for more than 20 years. In 2004 he founded the internationally renowned online trading platform pvXchange.com, where wholesalers, installers, and service companies can purchase standard components, solar modules, and inverters that are no longer manufactured but are urgently needed to repair defective PV systems.

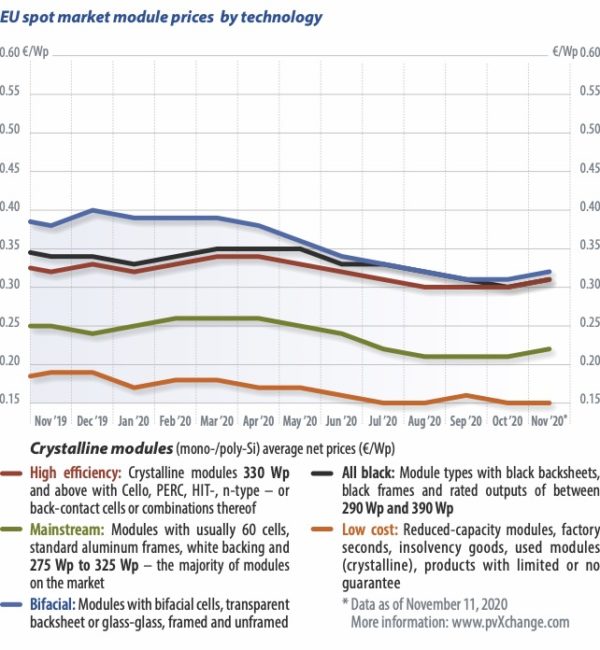

December 2020: 2020 was off to a good start, and then…

This year’s retrospective kicks off with a line that sounds like it’s right out of a pop song: Last spring, it all felt so right. And yet, what followed was not only one of the hottest years on record, but also one of the craziest in recent decades. This month and next, Martin Schachinger of pvXchange looks back at how European PV markets have developed under the pall of the pandemic and climate change.

This year’s retrospective kicks off with a line that sounds like it’s right out of a pop song: Last spring, it all felt so right. And yet, what followed was not only one of the hottest years on record, but also one of the craziest in recent decades. This month and next, Martin Schachinger of pvXchange looks back at how European PV markets have developed under the pall of the pandemic and climate change.

Mild weather rang in the new year and business was excellent for installers everywhere. The result in Germany, however, was a looming threat that the upper limit of PV capacity eligible for incentives under the country’s renewable energy act (Erneubare Energien Gesetz, or EEG) would quickly be reached. Some forecasts projected this would happen as early as the second quarter. That triggered a race to install the final few megawatts eligible for subsidies. At the same time, module availability was poor, and capacities for installers were tight. A bad situation was made worse by the reluctance of decision makers in the government to lift the 52 GW cap in the EEG. Unfortunately, the governing parties took no substantial steps to fulfill promises made in the 2019 climate package. The industry was confronted with very little security, prompting a battle cry: The cap must go!

February

Following devastating forest fires in Australia, the spread of Covid-19 began to dominate media coverage in China, and then in Europe. At that time, few could imagine how severe the pandemic would be. Negative impacts were initially limited to factory workers in China being sent on compulsory leave or prevented from starting work after the Lunar New Year holidays. As a result, the supply chain for raw materials virtually collapsed, and Asian cell and module production, among other things, came to a standstill.

The bottleneck led to fears that short-term prices would increase by up to 20% – fears which fortunately proved unfounded, as the maximum price increase for individual module technologies and brands was 10% for a brief period. However, the emerging crisis was a wake-up call for the solar industry and underscored our dependence on the “Chinese workshop.” The upshot was an uptick in plans to build new European production facilities for PV modules and energy storage.

March

As the pandemic progressed, parallels emerged with the threat of advancing climate change. In the media excitement about the virus, however, the climate crisis increasingly receded into the background. To curb the rate of infection, politicians ordered increasingly drastic measures. Unfortunately, the Fridays for Future movement also fell victim to these restrictions. The protests, held regularly for more than a year, could no longer take place. Though the movement continued in social networks, it did not have the same impact as mass protest in the streets.

Nevertheless, we can learn a great deal from the pandemic. We were made painfully aware of the instability of some industries and our system as a whole. We have seen how entire branches of the economy, which thrived financially and were so influential in a society of abundance, reached the verge of collapse within a few weeks and can now only be saved with massive government assistance.

May

The trend toward larger module formats began. Producers announced new module power ratings north of 500 W. Of the better-known brands, Longi Solar and Trina Solar led the way, with the trend culminating in JA Solar’s unveiling of an 800 W module in August. This increase in surface area was made possible with larger wafers and cells. Half-cut cells became more common; some even divided cells into thirds or quarters, using high-density interconnection technology in the modules. This took place almost exclusively in monocrystalline cells, with multicrystalline products increasingly disappearing from the market.

Since buyers do not pay for the module itself, but for the output, continuing to increase output per module was the obvious choice for manufacturers. This meant more money could be demanded for a module at the same cost, even as the per watt price stayed the same or fell. In fact, after almost a year of stagnation, wholesale prices for high-efficiency modules slowly started to fall again.

June

On the evening of June 18, 2020, the time had finally come, and the German parliament decided to remove the 52 GW cap on PV installations. Had they waited just a few more weeks, the limit would have been reached, and no new PV systems would have been eligible. The only reason subsidies were not stopped much earlier was the delay caused by Covid-19 and the associated restriction of supply chains. At the same time, however, the German government announced a more comprehensive revision of the EEG for the fall. We had to wait until October to realize with horror the “dirty tricks” that our politicians had come up with in this context.

A look back at the second half of the year, and forward to 2021, will follow next month.

Martin Schachinger, pvXchange.com

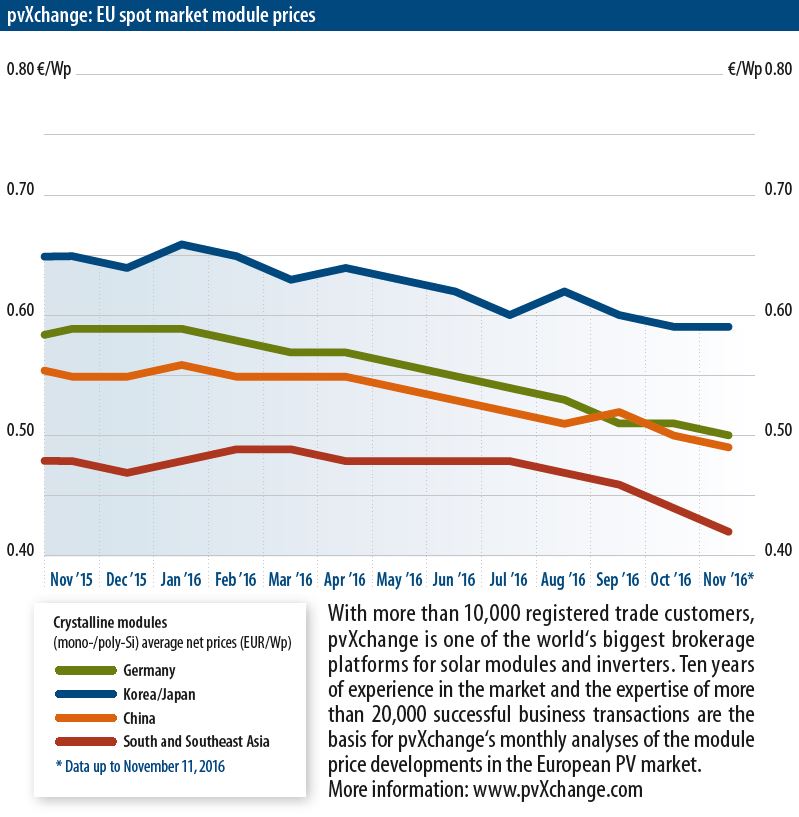

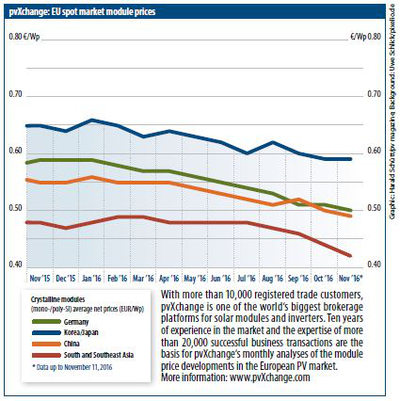

November 2020: Will Covid-19 continue to weigh on the PV industry?

As much as 15% of all renewable energy projects in Europe could be delayed or canceled due to the coronavirus crisis, according to a recent warning issued by McKinsey & Company. The pandemic has also had a negative impact on the energy markets themselves, says the consultancy. Persistently lower commodity prices made conventional energy more attractive, and the expansion of renewables less popular.

As much as 15% of all renewable energy projects in Europe could be delayed or canceled due to the coronavirus crisis, according to a recent warning issued by McKinsey & Company. The pandemic has also had a negative impact on the energy markets themselves, says the consultancy. Persistently lower commodity prices made conventional energy more attractive, and the expansion of renewables less popular.

As low electricity prices chip away at future profitability of PV and wind energy, incentives for investment have failed to materialize. And this, in turn, has deterred project developers from concluding new power purchase agreements. Martin Schachinger of pvXchange examines the ongoing effects of Covid-19.

Although the recent McKinsey & Company assessment, forecasting a downturn for PV project development may be correct, it paints an incomplete picture. The delay it describes primarily affects medium to large projects, often with supra-regional participation. The degree to which current restrictions have crippled the installation segment is something I will return to later. After all, under normal conditions, hard-working installation crews mainly from Eastern European regions move from one major construction site to the next in their daily work. We do not see this practice in the disributed PV segment, since for economic reasons companies tend to work with their own people or those in the immediate vicinity.

In the small to medium-sized PV systems segment – in Germany, at least – there has scarcely been any discernible negative impact from the pandemic so far. Sustained demand for high-efficiency modules is leading to price stagnation. Smaller projects are usually planned and built by a single provider. If necessary, the contractor will pitch in if there is a shortage of personnel. The greatest concern with such projects is the delayed delivery of components. Storage systems in particular have been a bottleneck for small PV plants throughout 2020. Fortunately, a plant can be completed and connected even without the planned storage system. The battery is simply delivered later and integrated into the system.

Nevertheless, demand for storage is holding steady. In Germany, residential storage is enjoying growing popularity. One almost has the impression that faced with a pandemic and the threat of a lockdown, many are not only stocking up on food and toilet paper, but also trying to become more energy independent. This trend has filled the order books of many installers this summer.

Furthermore, a trend is emerging of companies gaining easier access to financing through crowd-investing. Numerous platforms offer companies, often in the startup scene, the opportunity to raise funds on fair terms without the need for a costly financing round or an IPO. Hundreds of private investors can pledge small amounts, which then earn moderate interest over the subsequent years before the initial investment is repaid in the context of another, larger financing transaction or an IPO. Of course, for the small investor, there is always the risk of a total loss of the investment. Nowadays, however, you take the same risk when you book a flight with the wrong provider.

In the longer term, the solar industry as a whole could benefit from the knock-on effects of the pandemic. The coronavirus has led many regional governments to loosen their purse strings a bit – running up debts is no longer frowned upon. Some of the money released in the current pandemic budget will now be channeled into the expansion of renewable energy. Politicians are apparently slowly beginning to see the connection between environmental destruction caused by the nuclear and fossil-fuel-based economy and the growing number of natural disasters and worldwide viral epidemics.

All in all, the solar industry is fortunate to have escaped with just a black eye so far. Limiting ourselves to absolutely necessary business trips, shifting office work to the home, and foregoing trade shows and indoor events has not really hurt us. Productivity may even have increased at many companies, while costs have often come down. Digitalization was unstoppable even before the pandemic – it has simply overtaken us a bit more brutally and quickly.

Once the crisis has died down, we may also be able to look forward to some new, qualified and motivated workers from other industries who have fared less well. Former employees from the automotive sector or the steel industry who are fed up with uncertain conditions could soon put an end to the shortage of skilled workers in the solar industry. That would be good news for once!

Martin Schachinger

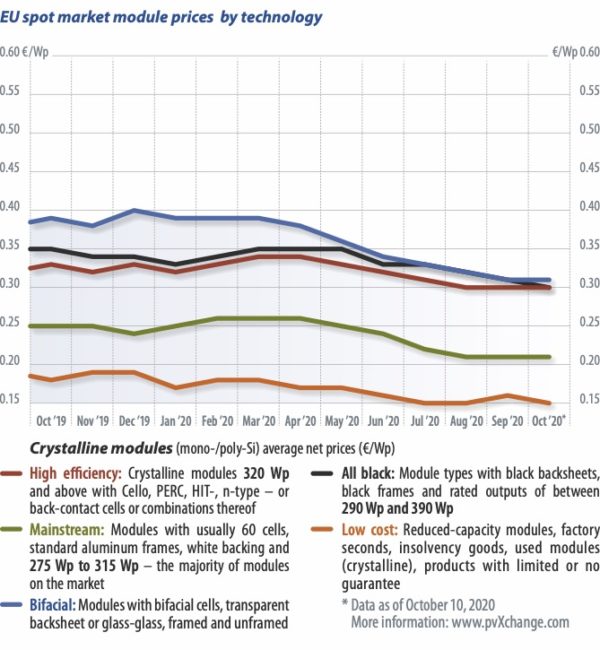

October 2020: EEG 2021: The destruction of renewables

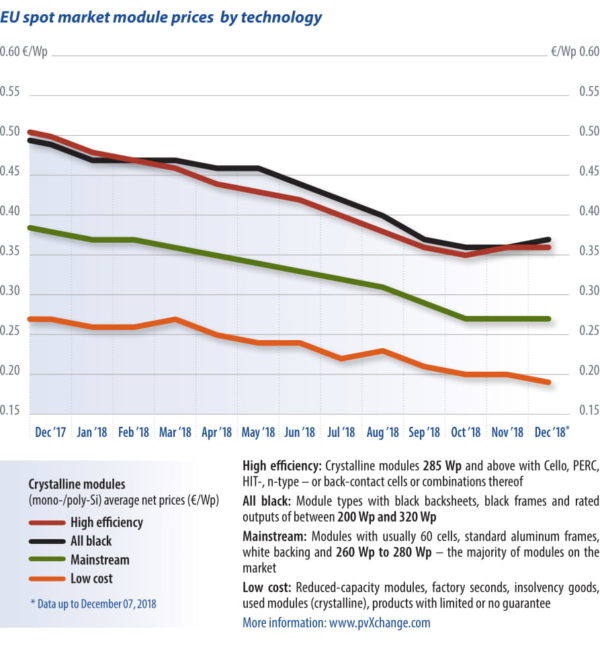

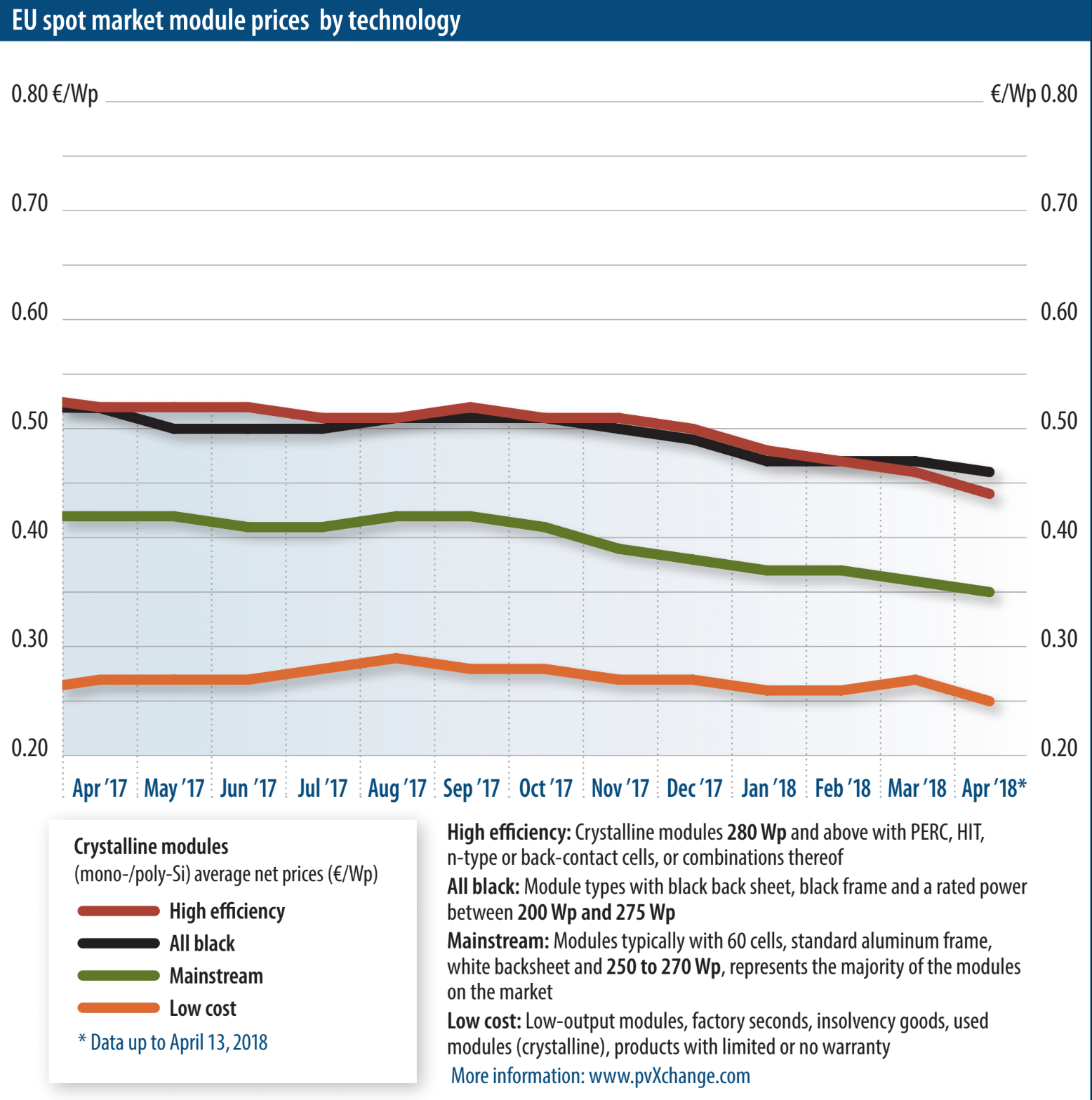

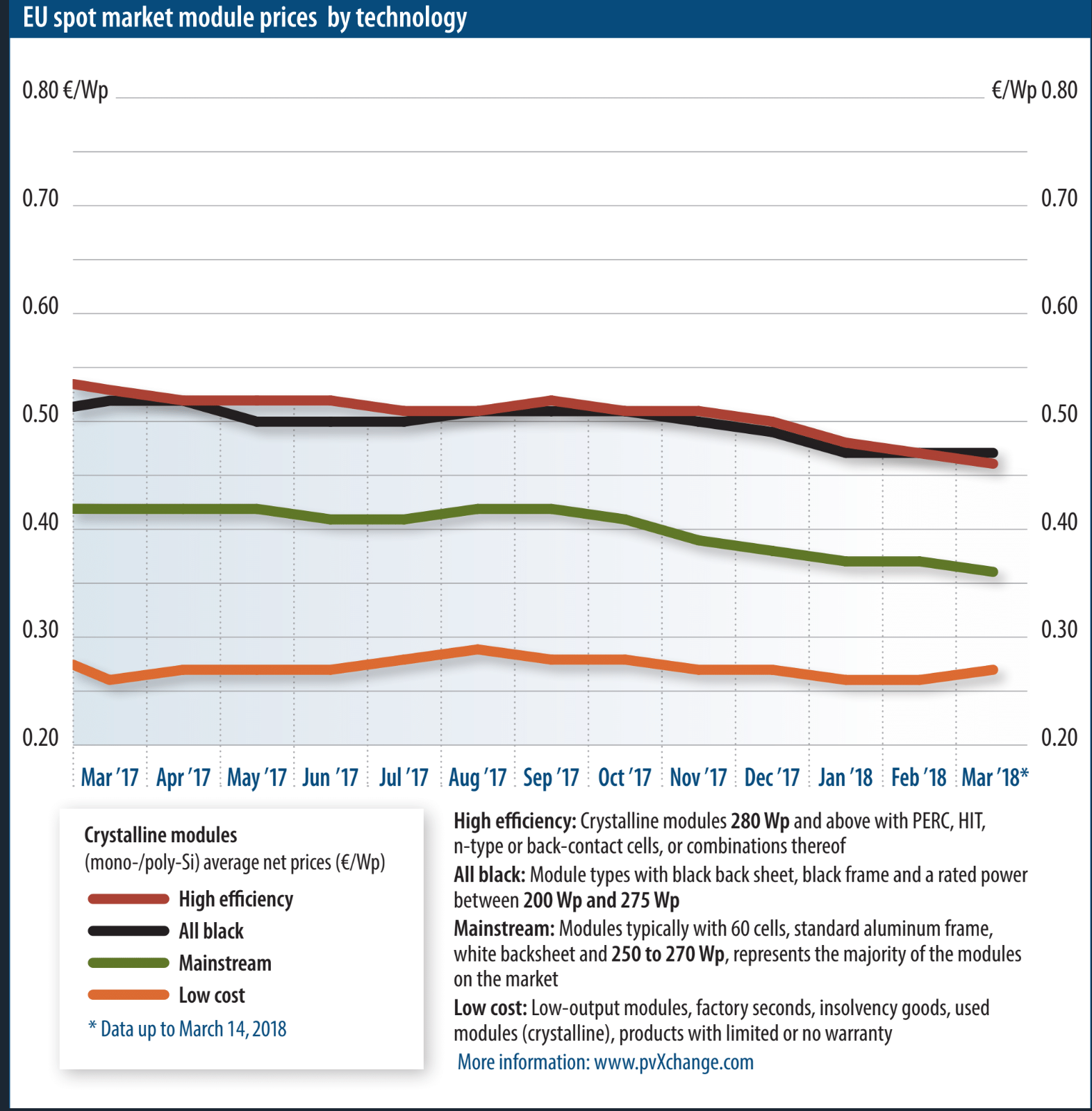

In the years ahead, we will not see a significant drop in prices for PV installations like those of the past decades. For small- to medium-sized systems, at least, prices have now reached a level that will be difficult to undercut. Also, the module prices themselves have stabilized across nearly all technologies over the past few weeks. Some manufacturers of both PV panels and inverters are even attempting to push through slightly higher prices, which they justify with production-capacity bottlenecks or swelling demand from Asia, of which there was scant evidence in September. Nevertheless, the nosedive in prices of the past few months has leveled out. However, module classes were adjusted slightly upward since the trend toward ever-higher power ratings has continued, without any notable change in the absolute cost of the individual modules.

In the years ahead, we will not see a significant drop in prices for PV installations like those of the past decades. For small- to medium-sized systems, at least, prices have now reached a level that will be difficult to undercut. Also, the module prices themselves have stabilized across nearly all technologies over the past few weeks. Some manufacturers of both PV panels and inverters are even attempting to push through slightly higher prices, which they justify with production-capacity bottlenecks or swelling demand from Asia, of which there was scant evidence in September. Nevertheless, the nosedive in prices of the past few months has leveled out. However, module classes were adjusted slightly upward since the trend toward ever-higher power ratings has continued, without any notable change in the absolute cost of the individual modules.

Points of criticism

Firstly, Germany’s expansion targets are too low – only about 5 GW of PV and 3.7 GW of wind per year, despite respected studies which have concluded that if we want to achieve the 1.5-degree target from the Paris Agreement, we will need much more ambitious expansion. Although there is some evidence of concepts for sector coupling and integration of generation-consumption systems, these are not yet mature. Fixed levies and overly complicated measurement and control requirements – among them, the broadening of the requirement to install smart metering on systems over 1 kW – present another problem. That even violates the regulations of the EU Renewable Energy Directive, which prohibits the imposition of fees and levies on self-consumption from PV plants up to 30 kW. In fact, the German federal government has until mid-2021 to transpose this into law.

Furthermore, the government wants to keep pressure on PV system costs by extending the requirement for public tenders. Up to now, PV plants larger than 750 kW could only be built and receive a fixed feed-in tariff if they were awarded a contract through a public tender, and the winners of such contracts have usually been ground-mounted systems. The plan for the future is to have separate auctions for rooftop systems and then for all projects larger than 500 kW with a gradual reduction of the limit to 100 kW. The Bundesverband Solarwirtschaft (BSW) and others see this plan as the biggest obstacle, since this segment accounts for up to half of annual PV expansion. In France, such tenders have already failed.

Finally, there is the over-20 crowd – that is, the post-EEG PV plants, and what the future holds once they are dropped from the EEG incentives. Once the 20-year period expires, network operators are no longer obliged to purchase or even accept power from these plants, many of which are still in good working order. Although the new draft bill does contain some proposals for the continued operation of these facilities, they could be characterized as “immature” at best. For operators of small plants, who will initially be affected the most, all of the proposed schemes – grid feed-in at market value, minus a marketing fee of €0.004/kWh, or self-consumption subject to additional taxes and fees – are nonstarters economically. Unless these proposals are improved, many old PV plants will likely be taken offline and then dismantled.

It is absolutely essential that Federal Minister of Economics Peter Altmaier summons the courage for meaningful, forward-looking EEG reforms, and does not once again cave in to the wing of his party that is driven by business interests, which apparently would prefer not to bear any of the costs of the energy transition. The hydrogen strategy – indeed, the entire energy policy of the federal government – is not yet a sustainable climate protection policy.

Yet, without a dramatic increase in the pace of renewables expansion, which is also increasingly being demanded by the EU, it will no longer be possible to change course.

Martin Schachinger, pvXchange.com

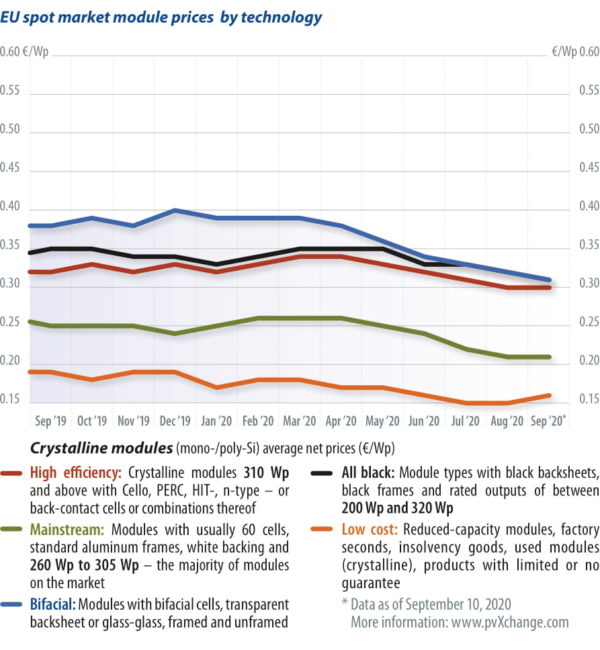

September 2020: Hot summer – hotter fall?

In Germany at least, the pace of new PV construction has continued unabated in recent months. According to recent surveys, the 52 GW upper limit once set by the German federal government for state-funded systems would already have been reached, but fortunately the scare was eliminated before it came to that. Now that the handbrake that many companies had pulled as a precaution has been released, the run on available capacity is in full swing. Even the less popular consignments of multicrystalline modules in the lower performance classes have now disappeared from the market, apart from a few containers-full. All that remains for project planners eager to build is to rely on new orders. However, since most solar panels have to be imported from Asia, longer lead times and higher prices can be expected.

In Germany at least, the pace of new PV construction has continued unabated in recent months. According to recent surveys, the 52 GW upper limit once set by the German federal government for state-funded systems would already have been reached, but fortunately the scare was eliminated before it came to that. Now that the handbrake that many companies had pulled as a precaution has been released, the run on available capacity is in full swing. Even the less popular consignments of multicrystalline modules in the lower performance classes have now disappeared from the market, apart from a few containers-full. All that remains for project planners eager to build is to rely on new orders. However, since most solar panels have to be imported from Asia, longer lead times and higher prices can be expected.

Price increases

Change in global demand for modules has always been a key driver for price adjustments. At present, however, there are different trends and contradictory forecasts of demand. In Europe, the solar PV industry is booming – at least it is in those areas where it is possible to work efficiently despite coronavirus-related restrictions. High demand is expected above all from China itself, and this should already be in full swing, but it has not yet been felt on the world market. I already reported last month on the incentive programs that have yet to be fully utilized this year and which could absorb up to 40 GW. At present, however, the supply situation for new orders for delivery in the last few months of the year is still quite relaxed, making it increasingly unlikely that the forecast volumes will actually be reached.

The situation in North and South America, usually key markets for PV panels, also speaks against any dramatic shortage of supplies. Steadily rising numbers of Covid-19 infections are causing problems for many companies, resulting in installation figures that fall short of expectations. Some manufacturers are reporting deliveries that have either been significantly delayed or canceled altogether, especially from their customers in the United States and Brazil.

One factor in the pricing of solar products, at least in Europe, is the U.S. dollar exchange rate. Following a relatively weak euro at the beginning of the year due to the threat of a dire economic situation triggered by the escalating pandemic in many European countries, the pendulum is now swinging in the other direction. President Trump seems to have neither the spread of the virus nor the economic decline under control. Consequently, the dollar is also coming under increasing pressure, which is causing a drop in module prices in Europe, which are mostly calculated on a dollar basis. But this trend may well weaken or reverse over the course of the year.

On the coronavirus front, everywhere in the world the daily number of new infections is still high. With Europe already well on the way to containing the coronavirus crisis, many now fear that a second wave will either come on the heels of the summer travel season or is already gathering steam. China alone seems to have low figures, and the crisis there is rarely discussed in public. Yet, this does not seem entirely credible, given the conditions prevailing in the rest of the world. According to China’s manufacturers, solar production is back to normal.

Investor response

As is so often the case, a two-pronged approach is not a bad idea. For important projects or those which are not so price-sensitive, materials should be procured immediately, but buyers should not be eager to agree to price increases, however justified. At the moment there is no real urgency, but there is still a lot of room for manufacturers to interpret future market developments. For projects that are only attractive once prices come down, the spot market should be the preferred option. In the coming months, there will certainly be the odd batch that can be purchased at an attractive price.

Martin Schachinger, pvXchange.com

August 2020:Clash of the titans reloaded

The overall decline in prices that has set in over the past months continues for the time being – price reductions in the upper single-digit percentage range are evident across all technologies. Although demand in the European market is stable to growing, there are still large-volume surplus stocks in many places, which have piled up due to coronavirus-related delays in project implementation and are only slowly being drawn down again. The usual end-of-quarter inventory adjustments have prompted broad-based price cuts, which continue to dominate the market at the beginning of the second half of the year. Manufacturers and dealers are undercutting each other for in-stock items available at short notice to make room for new shipments. This trend will be short-lived, in Europe at least, as the race to catch up is already in full swing. EPC and project companies at home and abroad have full order books, while banks and licensing authorities are also working off their backlogs quickly. The satisfaction of a well-functioning market is clouded, to say the least, by the uncertainty among some banks and investors arising from the ongoing patent dispute.

The overall decline in prices that has set in over the past months continues for the time being – price reductions in the upper single-digit percentage range are evident across all technologies. Although demand in the European market is stable to growing, there are still large-volume surplus stocks in many places, which have piled up due to coronavirus-related delays in project implementation and are only slowly being drawn down again. The usual end-of-quarter inventory adjustments have prompted broad-based price cuts, which continue to dominate the market at the beginning of the second half of the year. Manufacturers and dealers are undercutting each other for in-stock items available at short notice to make room for new shipments. This trend will be short-lived, in Europe at least, as the race to catch up is already in full swing. EPC and project companies at home and abroad have full order books, while banks and licensing authorities are also working off their backlogs quickly. The satisfaction of a well-functioning market is clouded, to say the least, by the uncertainty among some banks and investors arising from the ongoing patent dispute.

In the meantime, the so-called bankability of the three accused manufacturers has been called into question, and investors for projects using their products have threatened to pull financing. JinkoSolar, for one, has asserted from the very beginning that its current module production, or rather its currently available products, were not affected by the lawsuit. The other two competitors have remained cautious in this respect and have preferred to refrain from making public statements. But the word on the street is that REC has reduced its product range to the Alpha series, which uses n-type cells, which for technological reasons cannot be affected by the legal dispute. Longi Solar is also likely to reduce the delivery volumes of specific products for the time being until there is greater clarity in the proceedings, but in particular, until the demands of Hanwha Q-Cells are made public.

Court ruling

Buyers who want to play it safe with new orders should seek a binding clarification of the patent situation from their supplier in the form of a separate written confirmation. This document is particularly useful in cases where there is no existing supply contract containing clauses on the legality of the technologies used. Under no circumstances should the buyer hastily agree to a change in the supply terms and conditions without reviewing the legal consequences. There have been cases where manufacturer representatives have advised their customers to buy directly from the Asian parent company rather than from their German supplier. The patent lawsuit would only be valid in Germany. But in this case, the problem will just resurface again – at the latest when the modules are delivered to Germany and installed there – and then it will be the buyer’s problem. As the importer, the purchaser then assumes liability for the dubious products. Even for an installation in another European country, the buyer is unlikely to be automatically off the hook since the patent is a European one, and Hanwha Q-Cells can extend its claim at any time.

Clearly formulated statements of confirmation quickly dispelled concerns of the banks and investors in the cases submitted to me, clearing the way of any obstacles to the progress of the projects. In any case, it is important to be vigilant in the selection of suppliers and products. For the time being at least, the patent dispute has not had any effect on the availability of monocrystalline modules in the European market or on product prices – other mechanisms are at work here.

How much farther can prices drop? At present, there seem to be no downward price limits, even for products from the top manufacturers – price reductions in the megawatt range below €0.18/W are no longer the exception. This sell-off, which could be the downfall of some smaller manufacturers with a low capital base, is unlikely to cover costs at all. If this situation continues for a prolonged period, market adjustments will inevitably occur.

Only the financially stable manufacturers can survive a phase of low prices, such as the one we are currently witnessing. However, stabilization is generally expected due to increasing demand, especially in China. Funding programs are in place there, and so far, the uptake of these programs has been sluggish, but they still need to be utilized by the end of the year. There is talk of installation volumes in the 25 GW to 40 GW range for the third and fourth quarters. It doesn’t take an expert to imagine what this will mean for the global market. Any module not tied to a binding purchase agreement at an early stage will not leave Asia, as the Chinese market will absorb any production capacity. However, we know from past experience that such forecasts are not always accurate. Nevertheless, provisions should be made quickly for projects scheduled for completion in the short to medium term in order to avoid unpleasant surprises. Betting on further falling prices is pure gambling.

Martin Schachinger, pvXchange.com

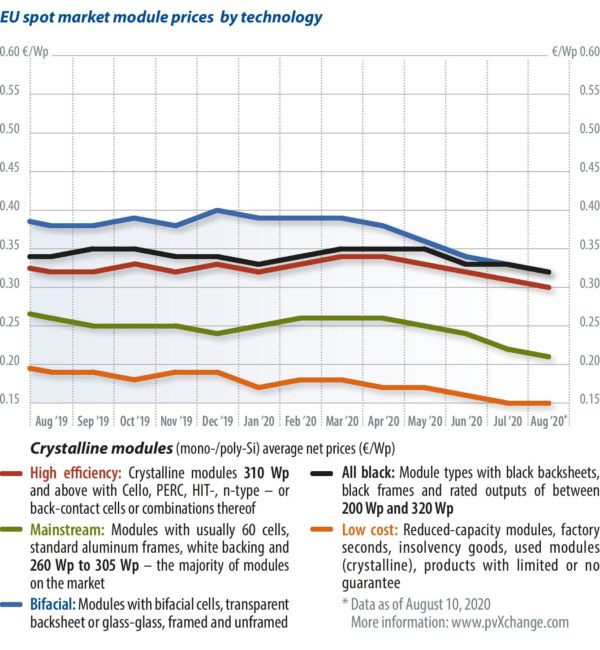

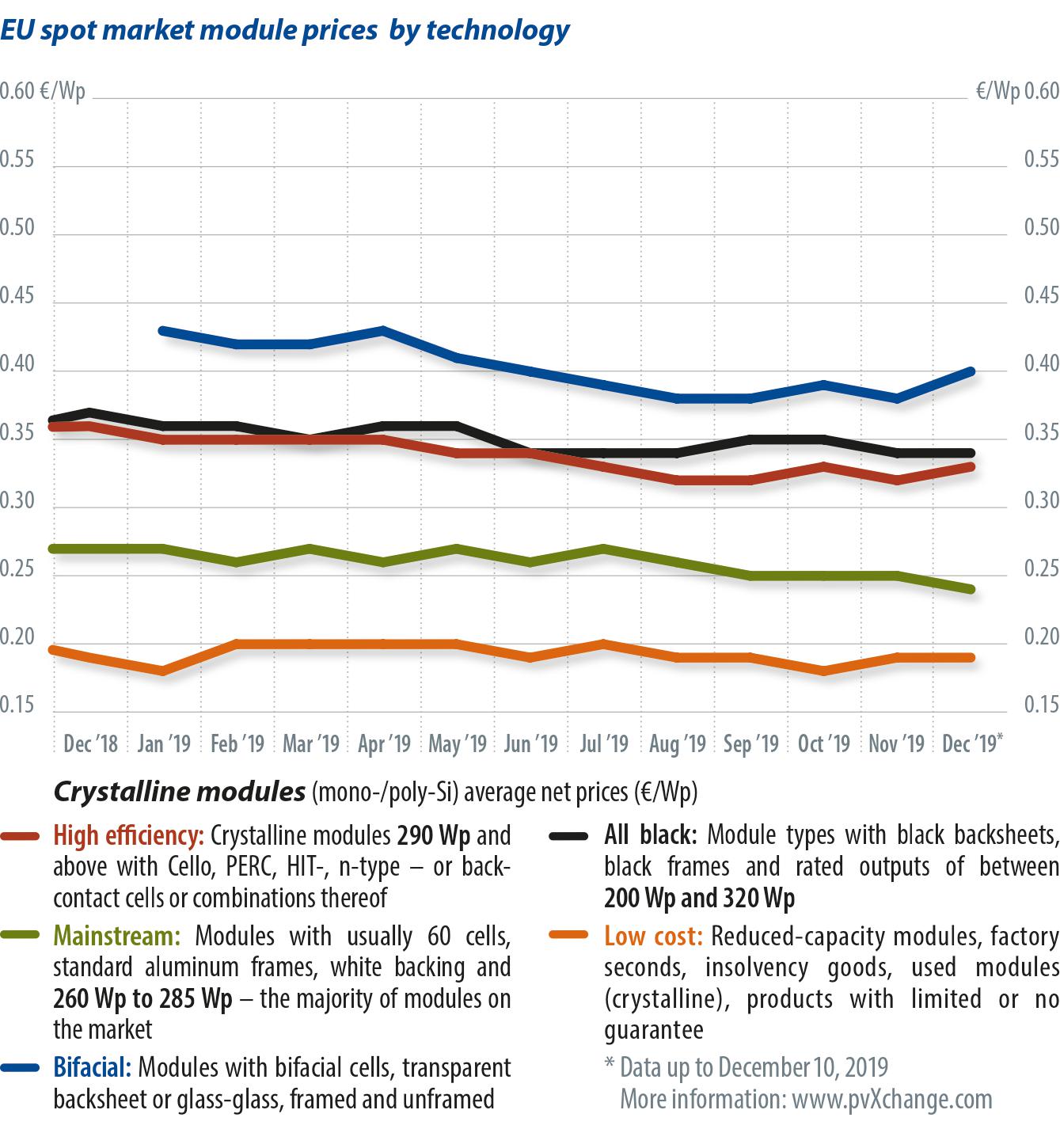

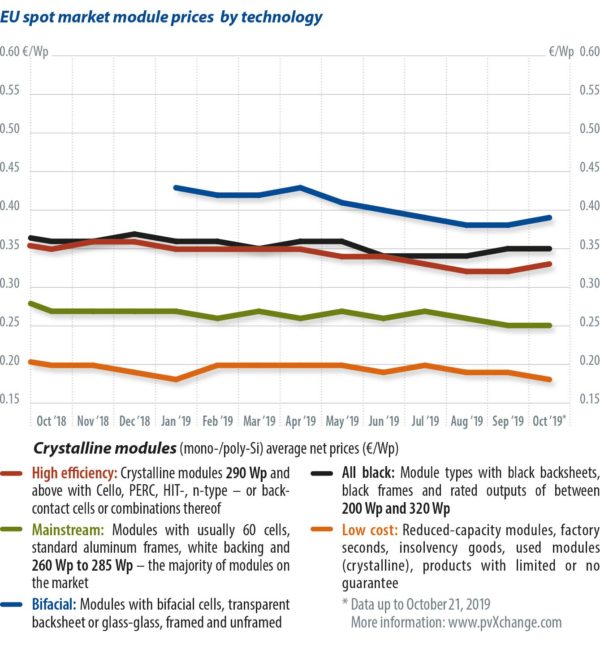

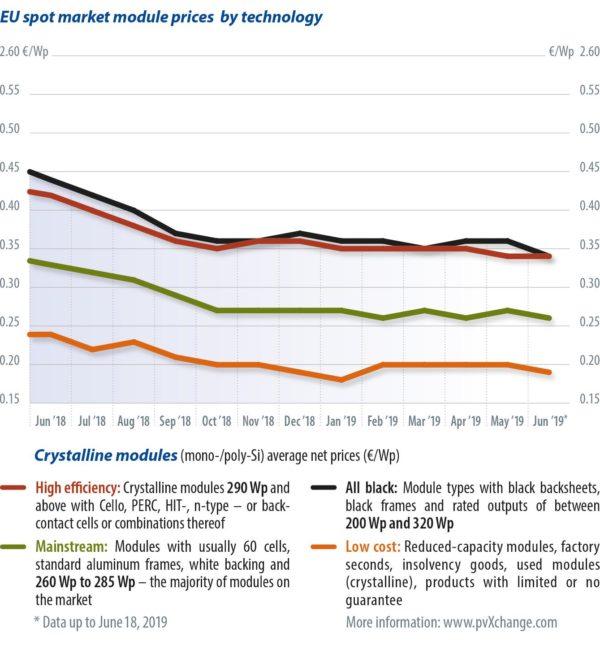

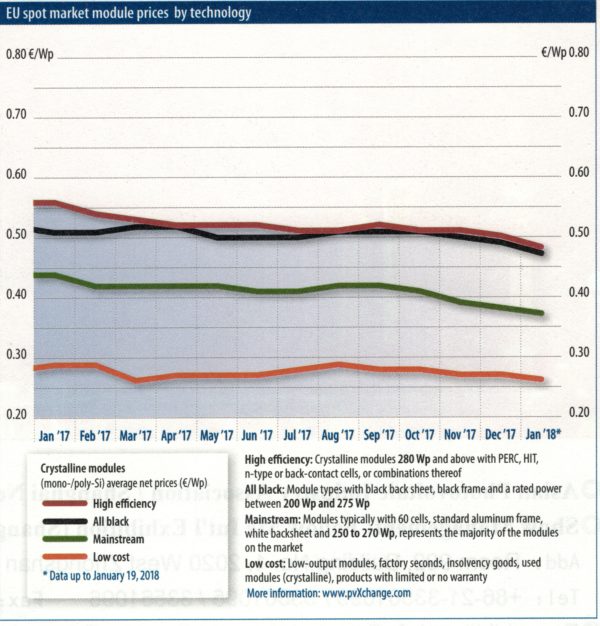

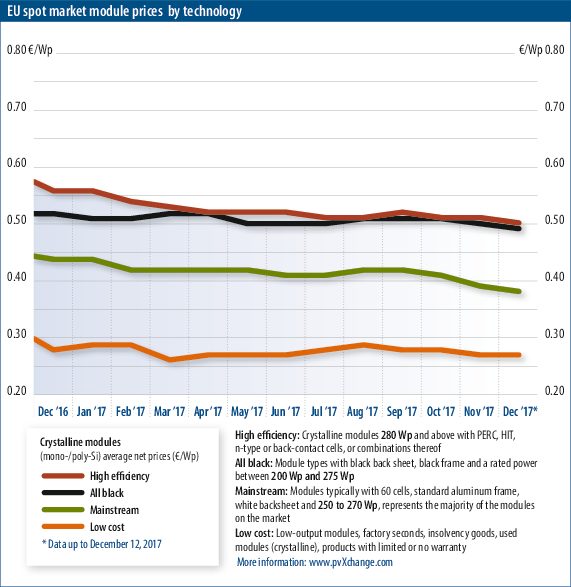

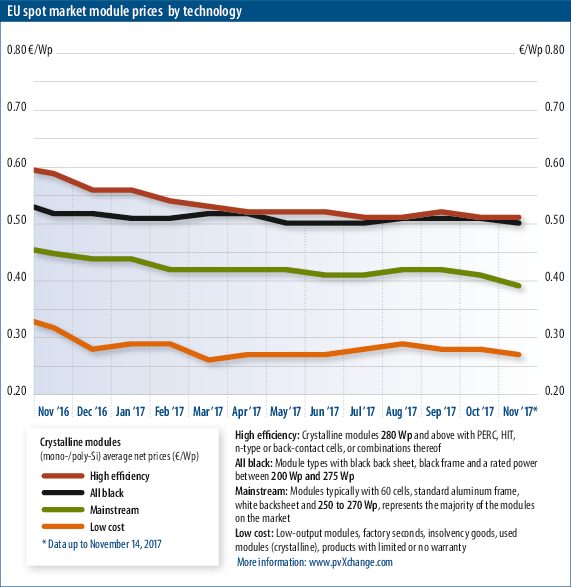

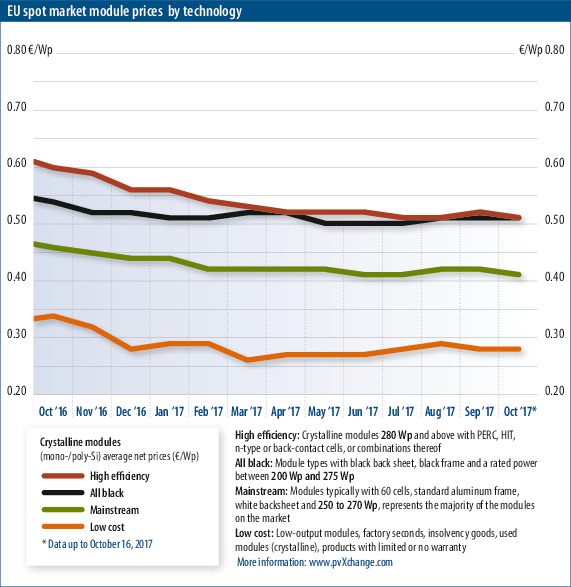

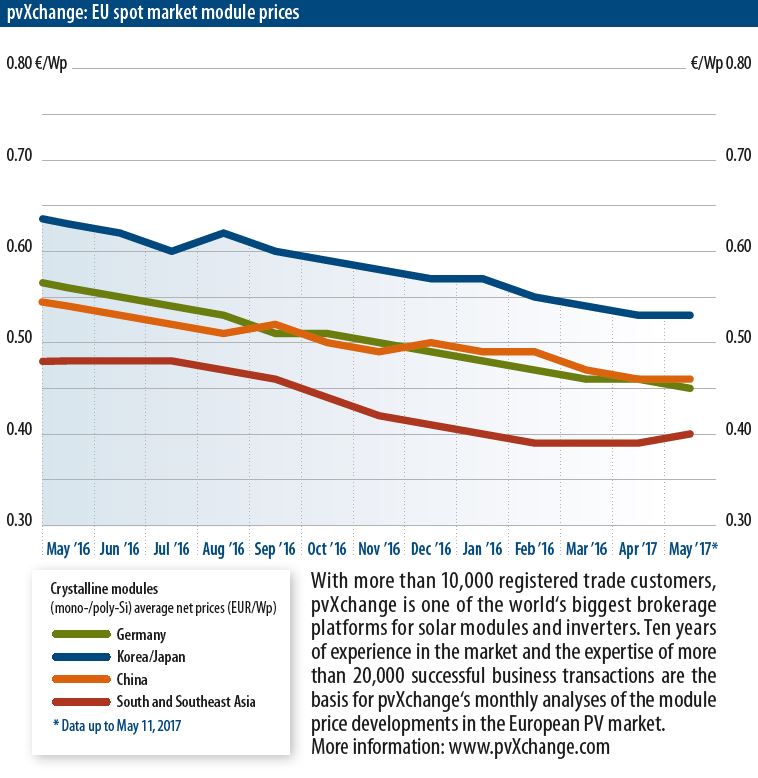

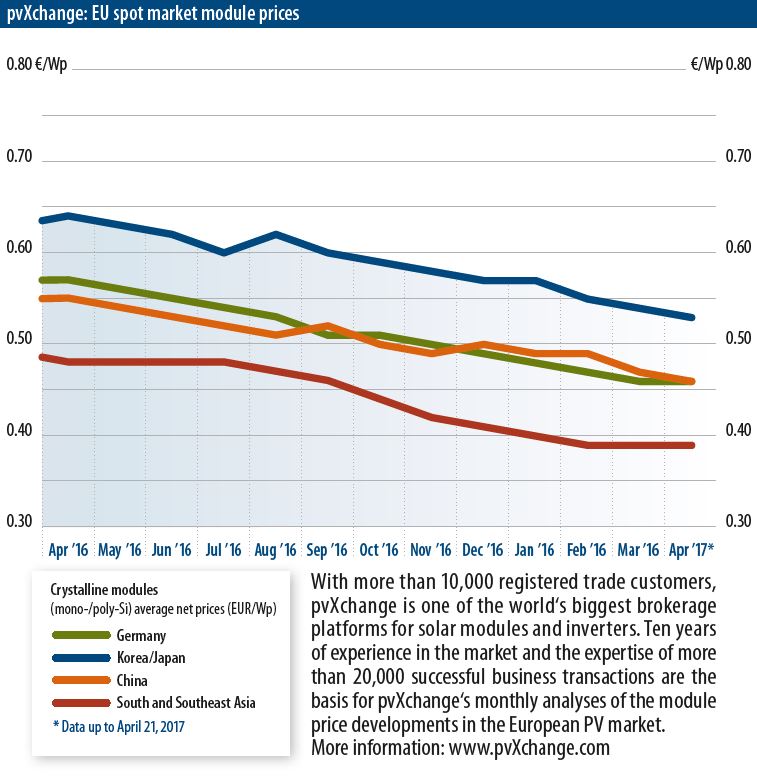

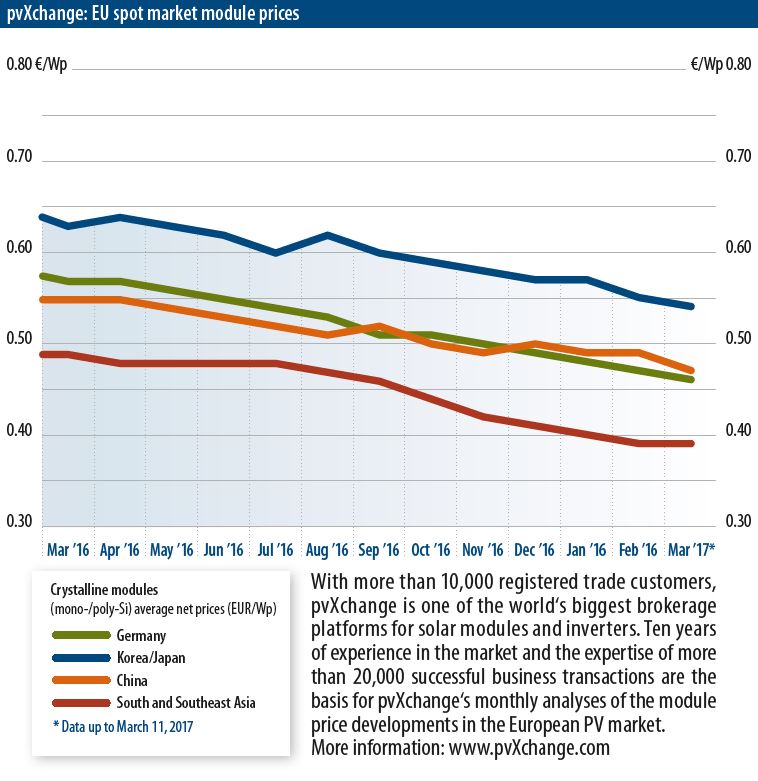

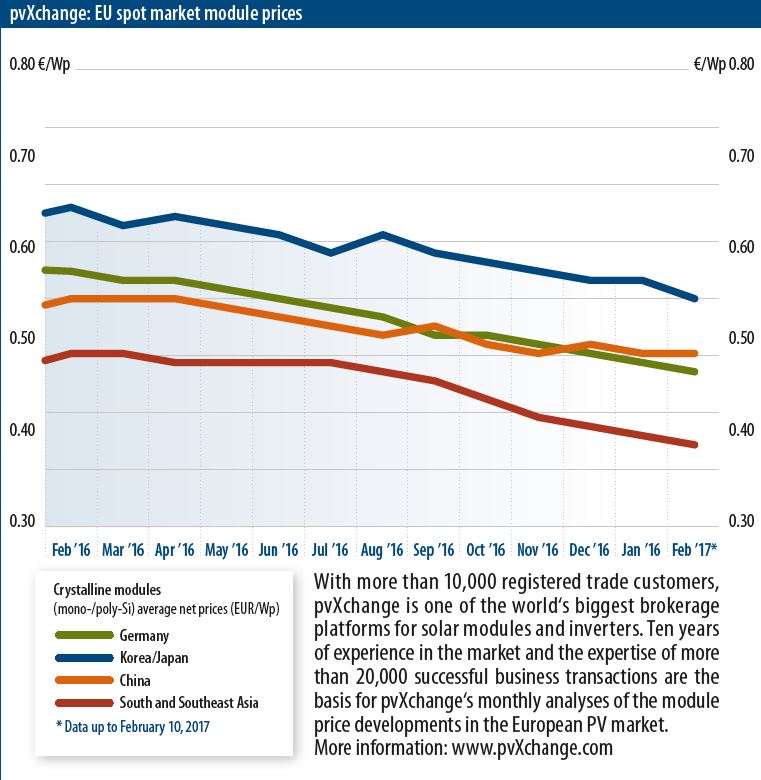

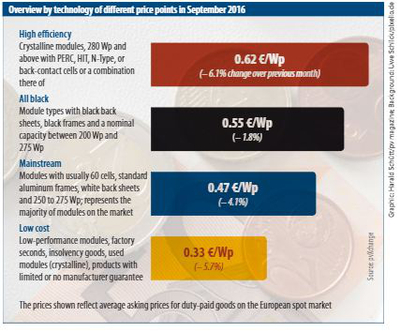

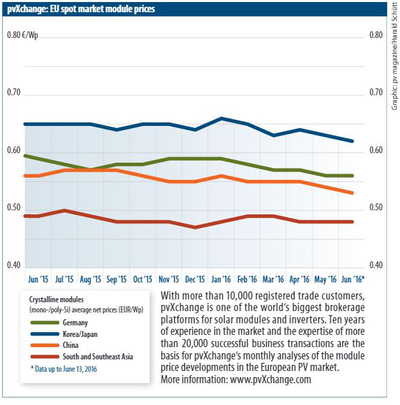

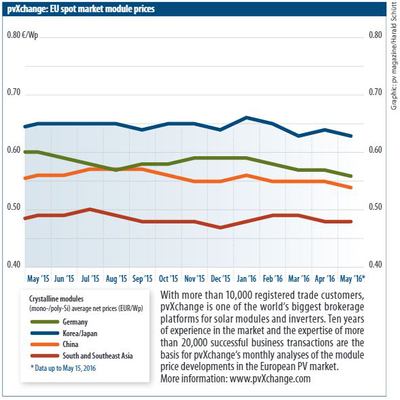

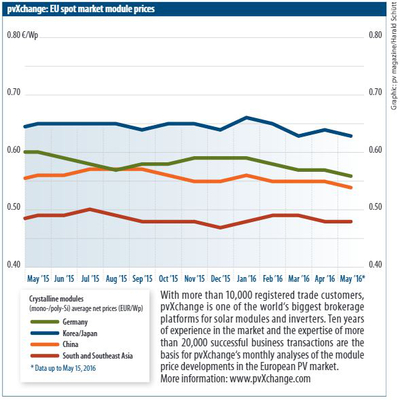

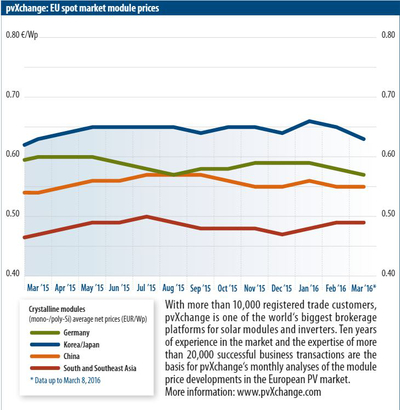

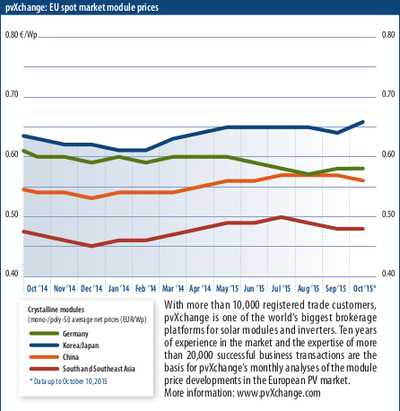

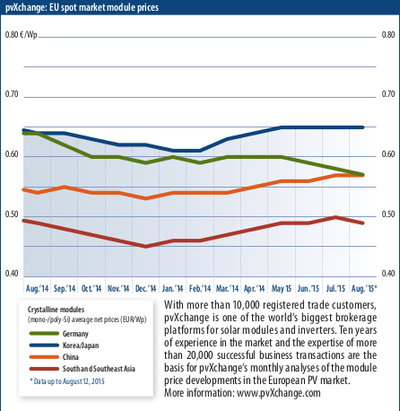

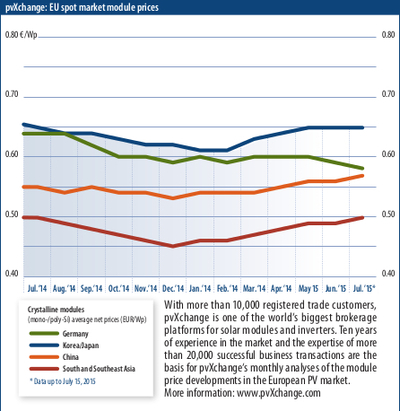

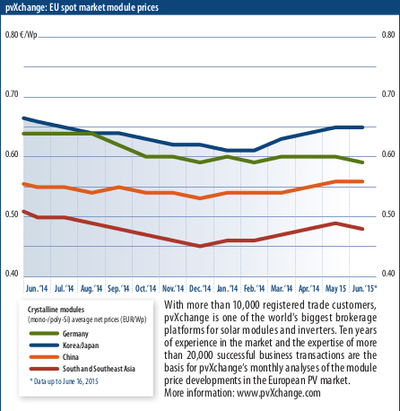

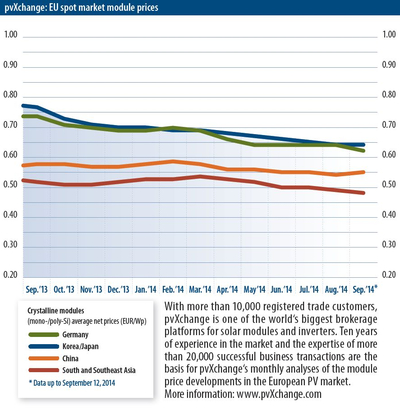

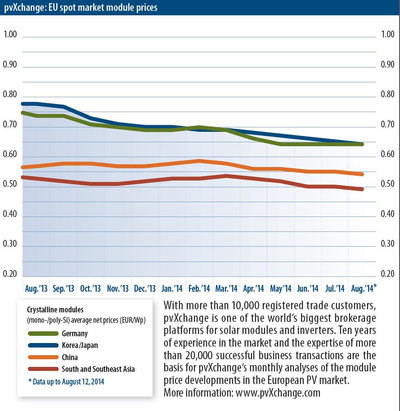

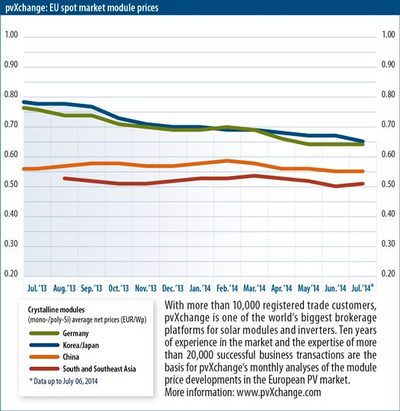

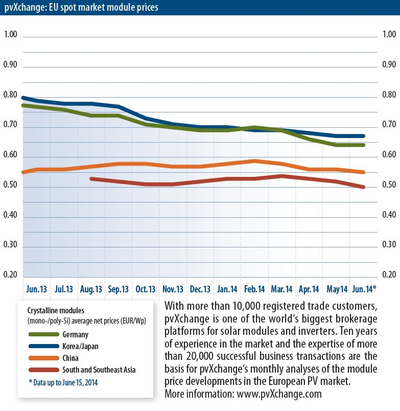

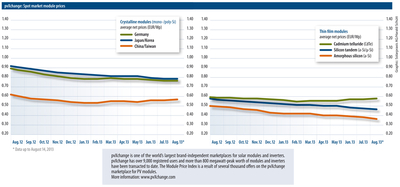

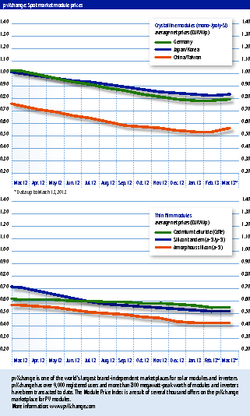

| Overview of the price points broken down by technology in June 2020, including changes over the previous month (as of July 14, 2020): | ||||

| Module class | €/Wp | Trend since June 2020 | Trend since Jan. 2020 | Description |

| Crystalline modules | ||||

| Bifacial | 0.33 | -2.9% | -15.4% | Modules with bifacial cells, transparent backsheets or glass-glass, framed and unframed |

| High efficiency | 0.31 | -3.1% | -3.1% | Crystalline panels at 295 Wp and above, with PERC, HJT, n-type or back-contact cells, or combinations thereof |

| All black | 0.33 | 0.0% | 0.0% | Module types with black backsheets, black frames, and rated power between 200 and 320 Wp |

| Mainstream | 0.22 | -8.3% | -12.0% | Modules typically featuring 60 cells, standard aluminum frames, white backsheets, and 270 to 290 Wp – this represents most modules on the market |

| Low cost | 0.15 | -6.3% | -11.8% | Factory seconds, insolvency goods, used or low-output modules, and products with limited or no warranty |

| Notes: Only tax-free prices for PV modules are shown, with stated prices reflecting average prices on the European spot market (customs cleared) Source: pvXchange.com | ||||

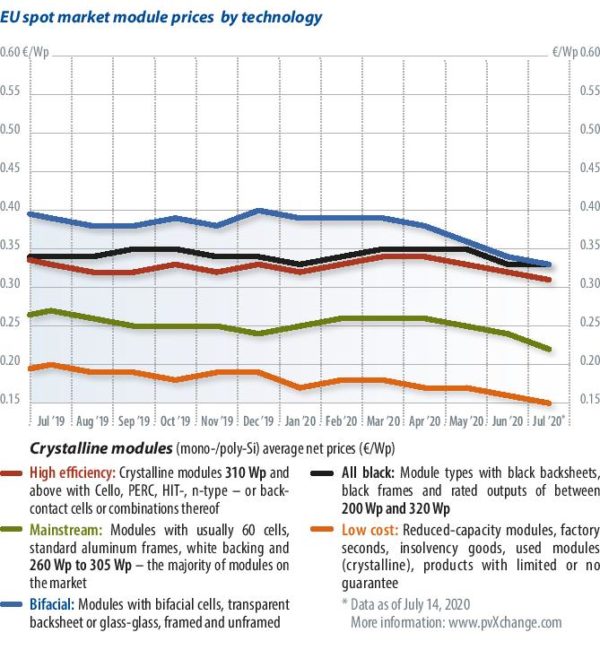

July 2020:A new boom, or the same old?

Many EPCs and installers in Germany’s small- to medium-sized segment boast impressive project pipelines. The only factors likely to slow the current boom are the approval authorities, which are still not operating at full capacity due to the pandemic, and the continuing degression of feed-in tariffs, which is making PV plants purely financed under Germany’s Renewable Energy Sources Act (EEG) increasingly uneconomic. At the current rate of plant construction, this shrinks feed-in tariffs by 1.4% per month, which puts the squeeze on prices for materials, planning, and installation services.

Many EPCs and installers in Germany’s small- to medium-sized segment boast impressive project pipelines. The only factors likely to slow the current boom are the approval authorities, which are still not operating at full capacity due to the pandemic, and the continuing degression of feed-in tariffs, which is making PV plants purely financed under Germany’s Renewable Energy Sources Act (EEG) increasingly uneconomic. At the current rate of plant construction, this shrinks feed-in tariffs by 1.4% per month, which puts the squeeze on prices for materials, planning, and installation services.

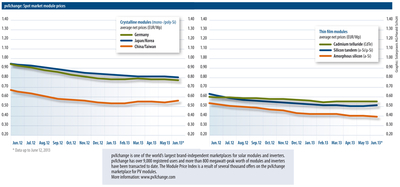

Fortunately, recent weeks have brought considerable price adjustments from module and inverter manufacturers – and they are heading down. Price reductions that had already started showing up in May finally reached the market in June – at least for current orders with delayed delivery dates. And that brings us to the crux of the matter: Anyone who is expecting to pay the same price for solar panels delivered today as those quoted for PV modules with delivery in the fourth quarter will likely be sorely disappointed.

Although there are currently no bottlenecks – products from all technology sectors and numerous brands are sufficiently available – the modules currently available often have production dates that lie far in the past. In recent months, it has taken modules much longer than usual to travel from Asia to Europe – courtesy of Covid-19. In the spring, however, raw materials prices were still significantly higher and the shutdown and ramp-up of production has entailed considerable additional costs. The potential for price reductions for these goods, which are now available at short notice, is therefore severely limited.

Post pandemic

Now that the viral problems have been solved – for the time being at least – prices are falling for all technologies, especially for monocrystalline modules (high efficiency, all black, and bifacial). For all appearances, the index price for high-efficiency panels is only 3% below the previous month’s price, but this is due to a necessary change to the range of products included in this class – it now starts at 310 W, rather than 300 W. Otherwise, all price corrections are in the range of 4% to 6%. Reference values also had to be adjusted because more and more module formats are being introduced to the market, resulting in higher outputs per module but without a significant increase in efficiency by area due to the larger surface of these panels. Supposed price reductions per watt peak are therefore more cosmetic in nature (see pv magazine 06/2020).

Leading the renewed fall in prices are the top six producers in the industry, measured by reported production capacity. Trina Solar, Hanwha Q Cells, Canadian Solar, JA Solar, JinkoSolar and especially Longi Solar are continuously increasing production capacity and module size while aggressively marketing their products at attractive prices that none would have thought possible until recently. It is highly doubtful whether many of the smaller manufacturers will be able to withstand this price war. We are likely to see the beginning of a market shakeout in the second half of the year.

Hanwha Q Cells is still hoping to gain the upper hand over some competitors in its patent dispute on cells with back emitter passivation. Even though the first round of court proceedings in the United States ended in defeat, it has now scored success in a German court. It is still unclear whether this victory will have any impact on the market or products of the defendant competitors, Longi Solar, JinkoSolar and REC Group. In a press release following the ruling, JinkoSolar said it would no longer produce or offer for sale cells and modules affected by the patent lawsuit. At the time of writing, the other defendants had not yet issued statements.

Second half

All of the conditions are in place for a hard-charging German market – high demand, good availability at attractive prices, and a stable policy framework. Right up to the last minute, however, the German solar industry was shaking in its boots and worrying whether the government would act before the 52 GW cap was reached and implement the policy change it had announced many months ago. After all, the summer recess for the government and parliament will soon begin.

Now, although the decisive step has been taken, a painful ending may yet be in the offing. A further amendment to the EEG has been definitively announced for the fall. It remains to be seen what “dirty tricks” politicians will come up with by then to make life unnecessarily difficult for solar activists.

We’ve already been on so many rollercoaster rides, and we’ve had to weather heavy seas for so long that the belief in calm waters has almost completely evaporated. Please surprise us this time, dear Grand Coalition!

Martin Schachinger, pvXchange.com

June 2020: Is size all that matters?

Along with new innovations and the renaissance of well-known cell technologies such as heterojunction and n-type, we are seeing an increase in module surface area with the introduction of ever larger cells. Just a year or two ago, modules on the market were almost exclusively made from so-called M2 wafers, in both full and half-cell variants. Now we seem to be entering the era of XXL cell formats. This development is taking place almost exclusively with monocrystalline cells – there have been hardly any advances in multicrystalline products.

Along with new innovations and the renaissance of well-known cell technologies such as heterojunction and n-type, we are seeing an increase in module surface area with the introduction of ever larger cells. Just a year or two ago, modules on the market were almost exclusively made from so-called M2 wafers, in both full and half-cell variants. Now we seem to be entering the era of XXL cell formats. This development is taking place almost exclusively with monocrystalline cells – there have been hardly any advances in multicrystalline products.

JinkoSolar has been using cells with an edge length of 158.75 mm for about two years in its Cheetah series. Trina Solar uses this cell format in products, such as the Honey DE06M series, while JA Solar uses it in the S09 and S10 series. The output of modules using these cells ranges from 325 W to 345 W, and the dimensions are about 10 mm to 30 mm larger than those of a conventional 60-cell module, depending on the version – which means they are still very easy to handle and process.

Longi Solar manufactures 166 mm edge-length wafers, using these in its LR4-60HPH and LR4-72HPH series, among others. These are 120-cell panels typically rated at 350 W to 380 W, or 144 cells at 425 W to 455 W, because this size cell can only be processed once they are sliced in half. If whole cells were used, the current would be so high that available inverters would not be able to handle it. Trina Solar also offers products such as the Honey DE08M with half-cut cells in this format, as does Hanwha Q Cells with its Q.Peak DUO G8 series. Modules of these types are as wide as 1,030 mm to 1,040 mm and 1,750 mm to 2,100 mm long, depending on the version.

Supersizing to 500 W

From today’s perspective, the latest products in the race for the most powerful module, recently introduced by JinkoSolar and Trina Solar and scheduled to be launched in the fall, are likely to prove unwieldy. Trina Solar unveiled its Vertex 500 W panel this spring. It apparently uses M12 wafers manufactured by Zhonghuan Semiconductor with a whopping 210 mm edge length. The resulting cells each have an output of more than 10 W at a rated current of 18 amperes. Trina Solar simply divides the cells into thirds and incorporates 150 of them into its module, five columns side by side, which delivers 480 W to 505 W modules.

JinkoSolar followed suit with its own giant module using a somewhat smaller, yet more exotic cell format of around 180 mm by 9 mm. The brand-new series, called Tiger Pro, offers a version with 144 tiled cells, which should generate 510 W to 530 W, and 555 W to 575 W in the 156-cell version. With dimensions of 2,385 mm x 1,122 mm, this product is aimed squarely at the ground-mount market, where the bifacial version will likely be particularly attractive – a bifaciality of only 6% would be sufficient to exceed the 600 W mark.

From a manufacturer’s point of view, this development may be reasonable. The market demands ever cheaper modules. For years, price reduction has been achieved by optimizing and scaling production. However, the capacities of individual companies are now so huge that even in terms of scale, only slight cost reductions can be expected.

Since the market does not pay for the module per se but for its average power output, it makes sense to continue to increase peak power per module. This means that more and more money can be demanded per module at the same unit cost, which in turn increases return on investment, which has been extremely meager in recent years. In fact, after nearly a year of stagnation, we can see that prices for highly efficient modules are slowly starting to fall again. At present, this is still influenced by the difficult supply situation, but it is already making itself felt in contract prices with longer lead times. However, producers are still reluctant to pass on all of the cost advantages of the new module types with higher rated output to the market.

The upsizing is less pleasing for installers, however, as they have to adapt to new formats that change in rapid succession. Handling in accordance with a manufacturer’s instructions is just one aspect. Larger solar module surfaces with the same or smaller frame thicknesses also place new demands on the substructure, which may have to be redesigned. Also, inverter design sometimes changes fundamentally in response to shifting electrical specifications.

It does not always have to be cheaper, although many may find it strange to read this coming from me. Nevertheless, I’d like to make a brief appeal for proven technology with consistent quality, reliability and ease of maintenance. These are also values that need to be taken into account for sustainable PV market development that determine overall cost – the so-called levelized cost of electricity (LCOE) of a project – of an installation over its lifetime. Some technological concepts advocated on the basis of reduced LCOE can become a one-way street in the medium to long term.

Martin Schachinger, pvXchange.com

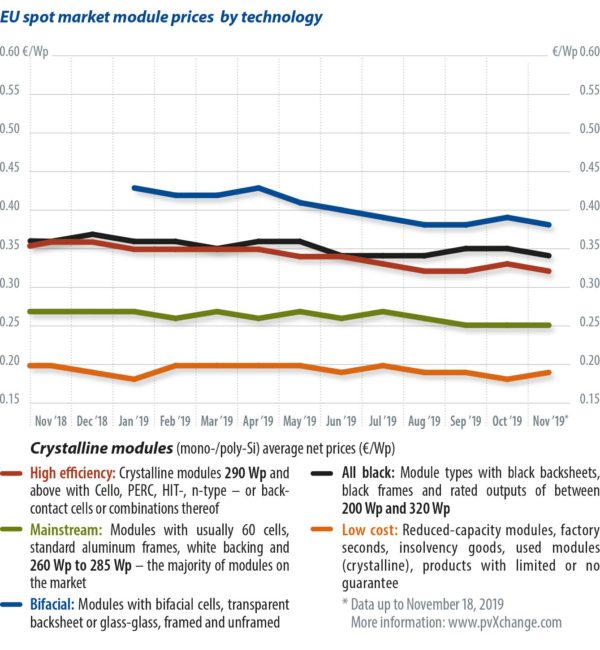

May 2020: The post-EEG age might come sooner than expected

In contrast to feeding all of a PV plant’s power into the grid, contemporary strategies envisage an upgrade for power plants that have already been amortized and will supply most of their energy at zero cost in the future. The switch to on-site consumption through the integration of energy storage in small private PV systems, direct supply, and intelligent balancing of generation and consumption in industry – as well as “power-to-X” applications – are just a few of the concepts being discussed, prepared and implemented.

With manageable investments, these facilities could then provide useful service for a few more years. Unfortunately, for many applications the legal framework is still lacking, meaning that some wind farms will be threatened with complete decommissioning. Most of these plants, however, are not facing a deadline for a subsequent use concept before the end of 2021. In the coming years, more and more systems will be affected, in line with installations added in the years after 2001.

There are already projects, primarily PV, that manage completely without statutory feed-in tariffs, but these are mostly very large solar farms. Smaller installations still prefer to take advantage of Germany’s Renewable Energy Sources Act (EEG), at least as a fallback solution. At present, however, we are sliding into a situation which makes the future of PV and wind seem anything but certain. Of course, there is still talk about the 52 GW cap for PV in Germany, which was supposed to be eliminated as part of the climate package put together by the government in 2019. Yet there is still no framework in sight for implementing this decision.

Draft bills have been submitted to the German parliament several times, but voting has been repeatedly postponed. Behind the scenes, there is still rumored haggling over distance regulations for onshore wind turbines – the cap on solar has apparently become a bargaining chip. The fact that the Covid-19 crisis has brought many other important issues to the desk of Federal Minister of Economics Peter Altmaier has also contributed to the delay. Yet the fact that the cap has still not been done away with can be considered grossly negligent, as the decision to do so was made long ago. There is far more at stake here than numerous jobs in the renewable energy sector.

Current situation

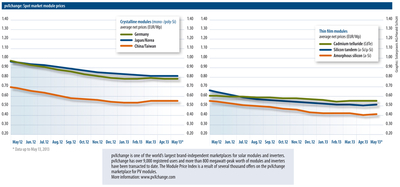

It can be concluded that the solar cap is perceived as a bigger problem within the industry than Covid-19. The effects of the pandemic are generally limited to slightly more difficult working conditions and a shortage of labor for medium- and large-sized projects, which often involve foreign workers who are now lacking due to border closures. The supply situation for modules, inverters and storage systems, which are primarily manufactured in China, is also somewhat tense. In April and May, the temporary shutdown in Q1 started to bite, and that has kept module prices stable for the moment. By June at the latest, however, the situation will have returned to normal if – yes, if – there was no solar cap!

Despite the crisis, the order situation is very good, at least in the small- to medium-sized systems segment. Order books are full and the mood among installers and dealers is good. Worries over an end to the EEG are not widespread in these circles, perhaps because for many small- and medium-sized plants, feed-in remuneration is no longer a primary concern. Savings achieved through covering on-site consumption are probably already more attractive than selling electricity, meaning an end to the solar incentive is not seen as very menacing in this case.

The situation is quite different for installers of larger rooftop and ground-mounted systems, whose business model is largely based on the existence of a FIT. This provides a long-term return, albeit very low, on which other sources of income can be built. Without this state-guaranteed security, many projects are simply not financially viable. At the current pace of expansion, it has now become very likely that the cap will be reached by the beginning of the second half of the year. Many players in this sector therefore have serious concerns about the future, as urgently needed orders are simply no longer being placed. A pragmatic optimism along the lines of “it’ll all work out” is increasingly giving way to bewilderment over the government’s approach.

The great death spiral for solar companies has not yet returned, but it will not remain distant without immediate action. In southern Europe the Covid-19 lockdown has already brought the solar industry to a standstill. In Germany it could be a combination of both the lockdown and the end of the EEG law, but mainly the latter. This time around it could take a very long time for the industry to sort itself out again in a post-EEG era. But at some point, it really will be too late.

Martin Schachinger, pvXchange.com

April 2020: Covid-19 beats Fridays for Future

I am not alone in seeing parallels between the threat posed by the virus and the need to advance the fight against climate change. Unfortunately, the only fundamental difference between the two crises is how we deal with them. To contain the spread of Covid-19, heads of state and regional politicians are imposing measures that become more drastic by the day. But when it comes to the climate crisis, hope seems to be the guiding principle. At some point we will come up with something that prevents or reverses climate change; the main thing is to keep the economy roaring and to not make any serious changes.

The volume of traffic on the road, in the water and in the air has fallen sharply, since people started limiting their travel to what is really necessary. People vacation mainly in their own countries, undertake long-distance travel only once a year at most, and then with the smallest possible carbon footprint. Consumption is regionally focused to strengthen the local economy. Slightly higher prices are not a problem at all, because everything superfluous and wasteful is avoided. A nice steak or some exotic fruit or vegetables are an occasional treat. On the whole, people enjoy the unhurried pace of society, friendly interaction at the office and in the streets, and emission-free fresh air.

This may sound like a distant utopia, but it could soon be reality if we can finally learn from the current crisis and take the right course of action. But will the coronavirus really have the power to bring about these economic and social upheavals in a more extreme and rapid way than a youth and climate movement could ever do?

When each and every one of us, including the decision-makers themselves, is directly affected – a number of prominent politicians are already infected with the novel coronavirus – it is suddenly possible to impose and implement cuts that would have been completely unthinkable before. And yet the consequences of climate change and pollution of our air and water are already far more deadly than a viral infection ever will be. Every day, countless people – young and old – die as a result of our destructive actions and unbridled consumerism. The big difference is only that it is happening far away and almost unnoticed, and that a large part of the populations of wealthy industrial nations do not seem to be affected by it. Currently, the coronavirus is public enemy No. 1, though in truth climate change has long since held that dubious distinction and will continue to do so for a long time to come.

Dress rehearsal

“Covid-19 beats Fridays for Future” applies in two ways. The pandemic and associated restrictions have achieved what many critics and some politicians have failed to do: The Friday demonstrations have been canceled! Now the protests continue on social networks, but of course this does not have the same impact as mass rallies on streets around the world.

The current situation seems like a preview of what we could face were the climate crisis to escalate; a kind of dress rehearsal, if you like. However, our performance here still leaves much to be desired. Our civilization has been caught off guard by the epidemic, and the scale and scope of the necessary response has for some time been greatly underestimated. The countermeasures came suddenly and inevitably led to chaotic conditions.

We are witnessing a demonstration of the fragility of our economic system and how quickly it can be thrown off kilter by an unexpected event, causing people and markets to react irrationally. Few seemed prepared for such a crisis; there were no fully developed plans for dealing with a pandemic affecting nearly every aspect of the globalized, networked world. Initial panic and chaos are understandable; after all, our jobs, our consumption, our social contacts – in short, our very freedom and prosperity – are likely at stake.

Another way

Now, hopefully we will learn a lesson from this, make a genuine fresh start after the pandemic, and not revert completely to old patterns of behavior and our resource-destroying lifestyle. We are beginning to realize that there is another way. The world will not come to an immediate end if we consume a little less, travel a little less, or party a little less. To restore stability to our system, we need to make even greater adjustments – we now face the challenge of radically transforming our economic system. Resilience is a much-cited term in connection with the local economy, but it also applies to ecosystems. It describes the ability to overcome disruptions and difficult life situations without lasting damage. This is something our system clearly lacks. But we can learn a lot from the present crisis; all we need is the courage to do the right thing and let something new, more resilient, and more sustainable emerge from it.

At the moment it still seems there is no political will to enforce what is right and necessary, but only what meets with a broad consensus. For government officials, maintaining power and electability always seems to win out over the common good. Protecting the population from coronavirus is apparently a matter of consensus and justifies drastic measures. But so much more is possible. Once this crisis is behind us, many restrictions should of course be lifted again. What should remain, however, is an awareness of the impending threat of climate change. The experience that life goes on, even when consumption is constrained, should be drawn upon – we just need to get organized and help each other. We need to continue digitalizing the world of work, while at the same time reducing our dependence on international flows of goods. Both of these things, if implemented properly, will produce deep cuts in CO2 emissions.

Let’s be honest: The coronavirus pandemic has a much greater positive impact on global CO2emissions than a whole year of Friday demonstrations and political work by the environmental movement combined – let’s take advantage of it.

Martin Schachinger, pvXchange.com

March 2020: The coronavirus wake-up call

The coronavirus (Covid-19) outbreak is now dominating daily headlines from China to Europe. There is also increasing talk that the long-underestimated and downplayed epidemic, which likely originated in the Chinese city of Wuhan, is having a negative impact on the global economy. Although we may all be suffering from information overload about this terrible news by now, the impact of the virus on the solar industry is, unfortunately, a sad reality, and the full extent of its devastation is just beginning to reveal itself.

The coronavirus (Covid-19) outbreak is now dominating daily headlines from China to Europe. There is also increasing talk that the long-underestimated and downplayed epidemic, which likely originated in the Chinese city of Wuhan, is having a negative impact on the global economy. Although we may all be suffering from information overload about this terrible news by now, the impact of the virus on the solar industry is, unfortunately, a sad reality, and the full extent of its devastation is just beginning to reveal itself.

The Chinese authorities have quarantined entire cities, restricted delivery traffic between special economic zones and ports, and imposed house quarantine rules on their own people in an attempt to control the rapid spread of the coronavirus. But the consequence is that production workers have been sent on forced leave or have not been able to restart work since the Chinese New Year holiday. In addition, the supply chain for urgently needed raw materials has nearly collapsed, with the result that cell and module production has not been able to recommence at all since the beginning of February. Goods that have already been produced that are stored in factories or are already at port are being blocked from delivery – or are only being delivered after considerable delays.

It has been just a few days since the news that individual production lines were being ramped up again. But it will be a very long time before existing manufacturing capacity can be fully utilized again, so huge backlogs of orders can be cleared, and cell and module production can return to orderly conditions, because nobody can say when the coronavirus epidemic will peak. Experts expect that the turning point may not be reached until April, if not later. Due to the strong dependence of the European solar industry on Chinese imports, local manufacturers of modules, inverters, and storage systems are unfortunately equally affected. Solar glass, EVA, cells, electronic components – everything is sourced to a large extent from Asia, and in particular from China.

Market impact

In short, there will be chaos. All manufacturers, including the last remaining German producers, are currently juggling the remaining goods in their warehouses, in port or in transit at sea. Available goods are scarce and quickly sold out. Since a reliable resupply date is anyone’s guess at present, major customers are bringing forward some of their already confirmed consignments and are being given preferential treatment. Smaller companies or customers wanting to place new orders have been left in the lurch. The supply situation for the well-known brands can safely be described as bleak. Switching to less well-known brands is only possible to a limited extent because many of the off-brand manufacturers have not yet supplied sufficiently large quantities to the European market. And freshly manufactured goods from China are then naturally subject to the same constraints as the products of the major players.

Although inverter and storage system suppliers have not been affected by the crisis so far, the deteriorating resupply situation has become apparent there as well. Particularly sought-after types of inverters, especially those for the commercial sector, will no longer be available for the foreseeable future. Also, the availability of some types of domestic storage systems, such as those from Chinese manufacturer BYD, has not really improved since the end of last year and has again reached a low point. It’s hard to predict how long this crisis will last, but it is conceivable that the catastrophic supply situation for products with Chinese content will continue for months to come and that the general situation will not improve before the middle to end of the third quarter of 2020.

Taking precautions now and hoarding modules and accessories is hardly possible – it is already too late for that. If you have not yet purchased the products for projects to be completed in the next three to four months, the only remaining option is to buy them on the spot market. But since this is largely determined by supply and demand, the conditions for hotly sought-after products will not always be customer friendly. As early as February, prices were on the rise across all technologies almost without exception. Further short-term price increases of up to 20% in the coming months are entirely conceivable. The economic viability of some projects is likely to suffer as a result, and their completion may be in the balance. Whether this will lead to a general market collapse remains to be seen.

However, postponing projects planned in the short term to the second half of the year, or even further, is difficult to implement – at least in Germany. There is the monthly reduction of the feed-in tariff, as well as the still-existing 52 GW cap for PV systems to contend with. However, the abysmal supply situation is affecting almost all market stakeholders, which means that quickly reaching the legally defined maximum cap on subsidized installations will simply be pushed further down the road. Nevertheless, it would be advisable to consider a short-term adjustment in order to prevent further economic damage to operators and investors of newly constructed PV plants. Likewise, those awarded contracts in the 2018 round of tenders who have to bring their projects online on time over the course of this year are unlikely to be very happy with the current situation.

The coronavirus crisis and all the adversities and limitations associated with it once again demonstrate our dependence on “workshop China”. All previous measures to end or at least reduce this dangerous dependence – the protectionist measures of the EU Commission between 2013 and 2018, for instance – have unfortunately failed miserably.

The current situation in the renewable energy sector – and in many other industries, for that matter – is alarming and illustrates that more value-added manufacturing is urgently needed within Europe. Such incidents – epidemics, natural disasters, political unrest – can be expected to occur in parts of the world important for Europe’s economic development at various times in the future.

Martin Schachinger, pvXchange.com

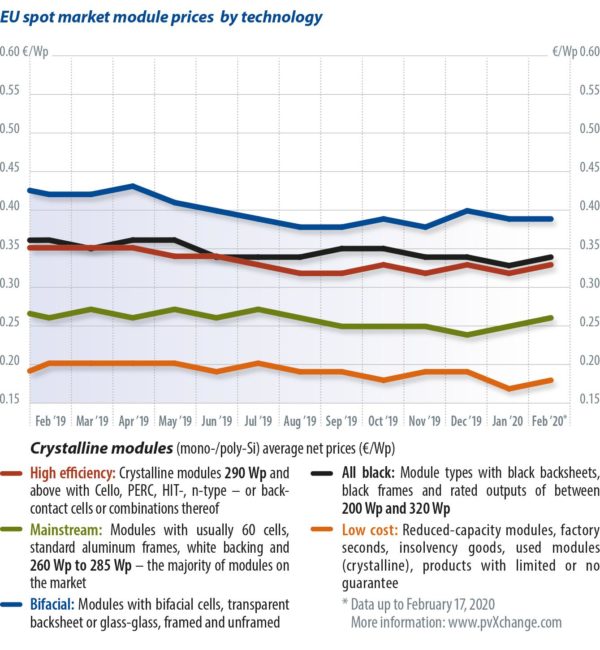

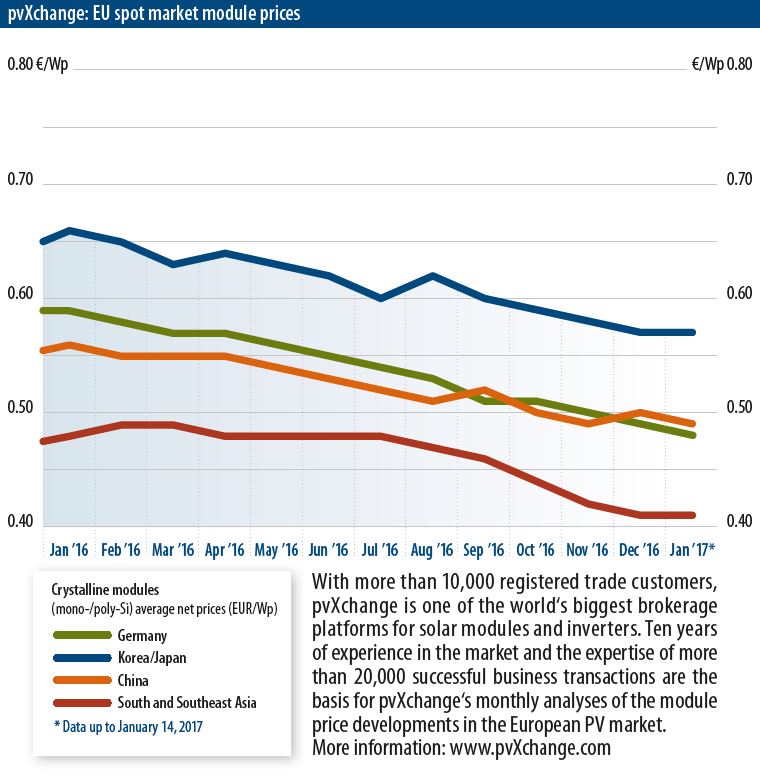

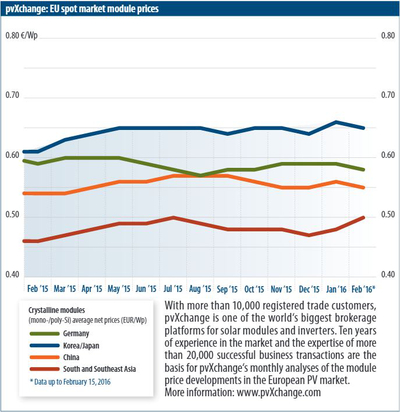

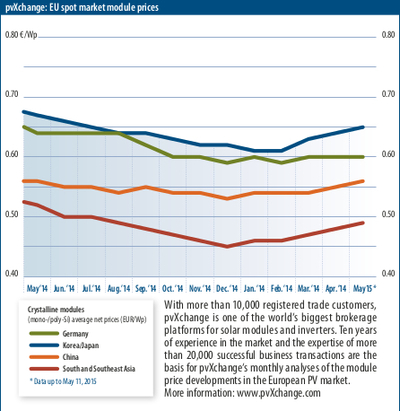

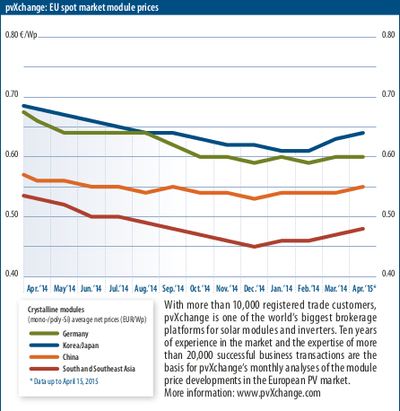

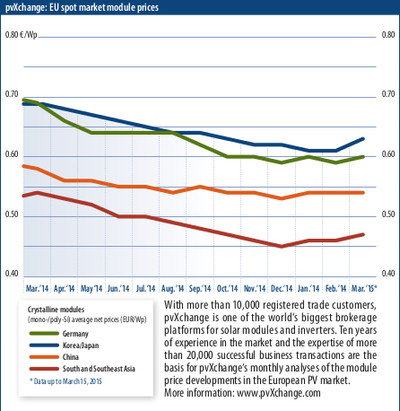

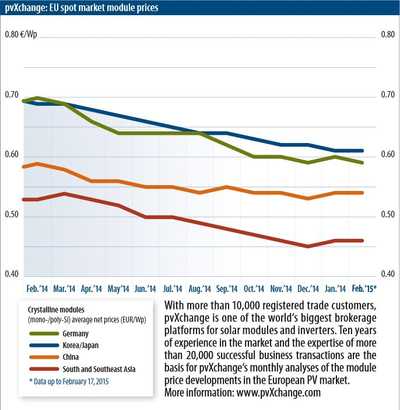

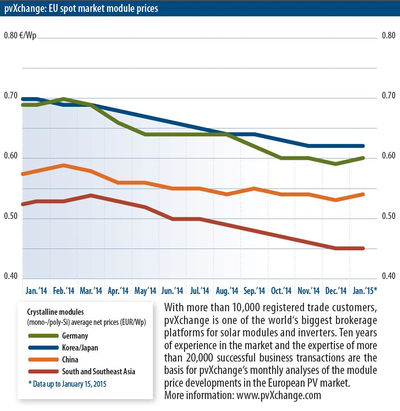

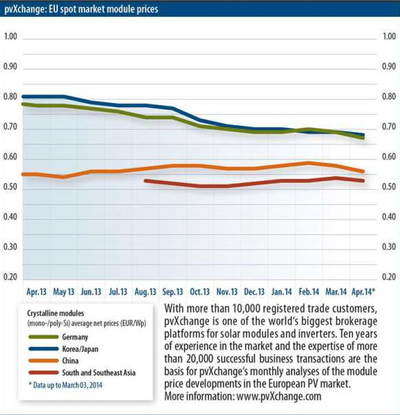

February 2020:Remove the cap to sure up PV sector

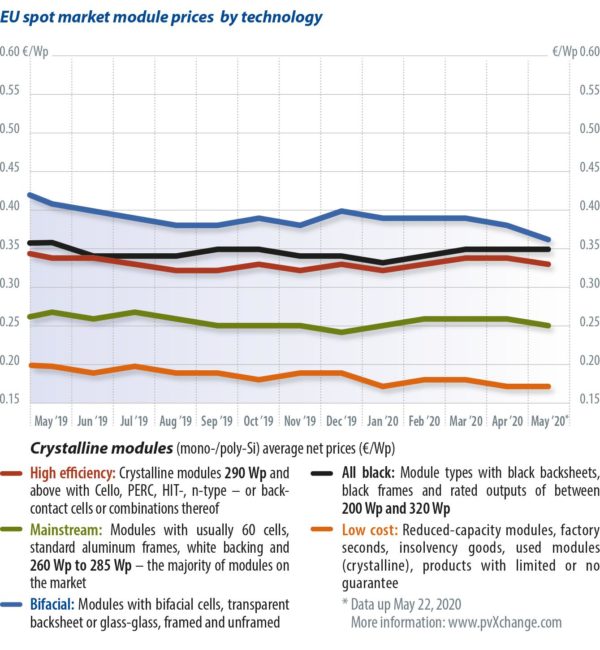

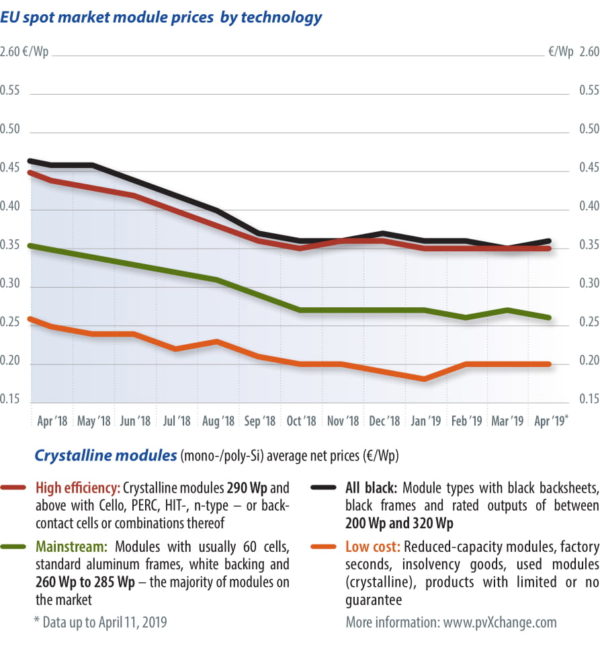

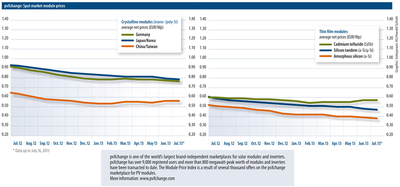

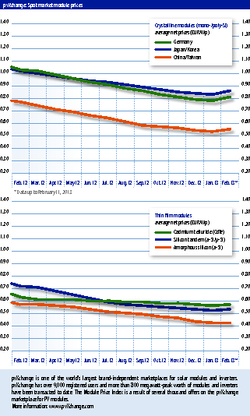

Will 2020 turn out to be a good year? What challenges will PV have to contend with? Will Germany’s political elite finally come to its senses? Let’s start by looking at current module price trends.

As can be seen from the chart below, there was a slight drop in prices across almost all module technologies, triggered by recent selloffs of manufacturer and dealer product inventories remaining after the holidays at the turn of the year. This trend will not continue – at least not in the first half of the year – but high demand at the beginning of January has already led to bottlenecks in certain areas. Once again, there is a long wait to purchase, particularly for popular brands and performance classes. Manufacturers such as Trina Solar, JA Solar, and JinkoSolar are currently only accepting orders for April, May or even June delivery. It therefore seems advisable for project planners and installation companies to take precautions if they do not want to be left without high-quality modules in the coming months and then have to take whatever happens to be available.

In the case of cheaper mainstream modules, there has already been a supply problem for some time, due to the systematic conversion of module fabrication lines to monocrystalline cells, mostly with PERC technology. However, the price increase in this index essentially reflects a shift in the boundaries between the various classes.

The lowest performance class for high-efficiency modules now starts at 300 W, with most of the products in this class available on the market offering outputs between 325 and 340 W. Crystalline modules with outputs below 275 W, on the other hand, will fall into the “low cost” class in the future; that is, in the same category as clearance items and low-output modules. In this category, last month, there were a number of large volume lots of older stock, as well as used modules from plant decommissioning, resulting in a major price decrease. Unlike the prices for the other module classes, this price point is determined exclusively by offers on the spot market.

Grave threat

Of course, it is – once again – the refusal of decision makers in Germany’s coalition government to eliminate the 52 GW cap on PV in the German Renewable Energy Sources Act (EEG). Unfortunately, since the government parties promised to do away with the cap as part of the country’s climate package, to date it has been all talk and no action. There is occasional mention of lowering the limit on tenders to compensate for the elimination of the cap, and sometimes further cuts to onshore wind development is mooted. But a deal at the expense of the already hard-hit wind industry is simply unacceptable. Germany needs a mix of all known renewable energy sources and often derided decentralization in order to achieve supply security at reasonable costs, both now and in the future.

At the moment, however, we are heading for a very dangerous situation. The 52 GW cap is still in place, but fortunately demand for PV systems is high and the order books of installation companies everywhere are solid. What this means is that the statutory upper limit for PV capacity eligible for feed-in tariffs under the EEG will soon be reached in Germany – some forecasts project that this could happen as early as the second quarter.

At the same time, modules are becoming increasingly scarce, and available capacities of skilled trades are scarcely sufficient to handle their current project pipelines in a timely manner. I already addressed the shortage of skilled solar-industry workers in an earlier commentary (see pv magazine 01/2020). According to surveys by installer platform, www.installion.eu, many installation companies have already stopped accepting orders for the first half of 2020.

Rising uncertainty

So, once again, we find ourselves in a situation with very little planning certainty. How can investors decide whether to risk their capital if they do not know whether a newly installed PV plant will receive a guaranteed feed-in tariff, if for the aforementioned reasons it cannot be installed and connected to the grid before the second half of the year? Nevertheless, many medium-sized PV systems from 100 to 750 kW are still being designed and built in Germany as pure EEG-compensated systems.

Due to government inaction, this segment could be all but dead, or at least close to dying out. As a result, many companies committed to this segment, slowly getting back on their feet since the major clearing of the field after 2012, are likely to be dogged by intense fears over the future.

So, if the positive developments in the solar energy industry are not to be abruptly curbed once more, we need to set a political course immediately and create a secure legal framework. We cannot wait indefinitely for an EEG amendment, which has not yet been announced. We need a faster pace of expansion if we are to avoid missing the government’s climate targets. We need a strong solar sector and a strong wind power industry that can offer secure jobs to more and more people. What we do not need at all, however, is an upper limit for PV in the German EEG. In this spirit – once again – an urgent appeal: The cap must go!

Martin Schachinger, pvXchange.com

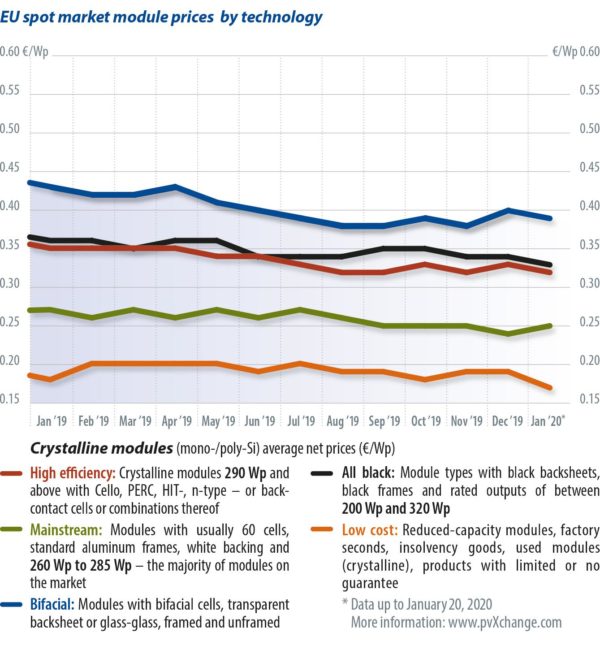

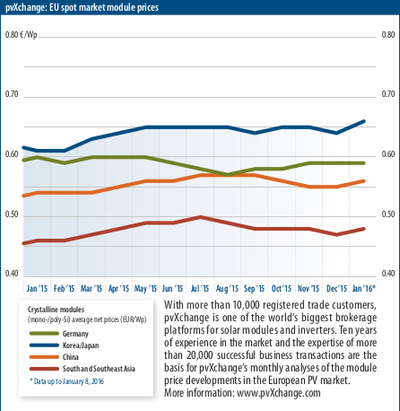

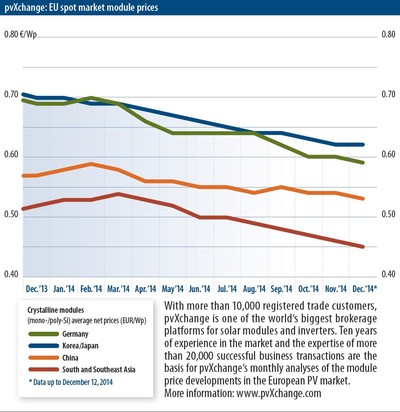

January 2020: A year of change: Part 2

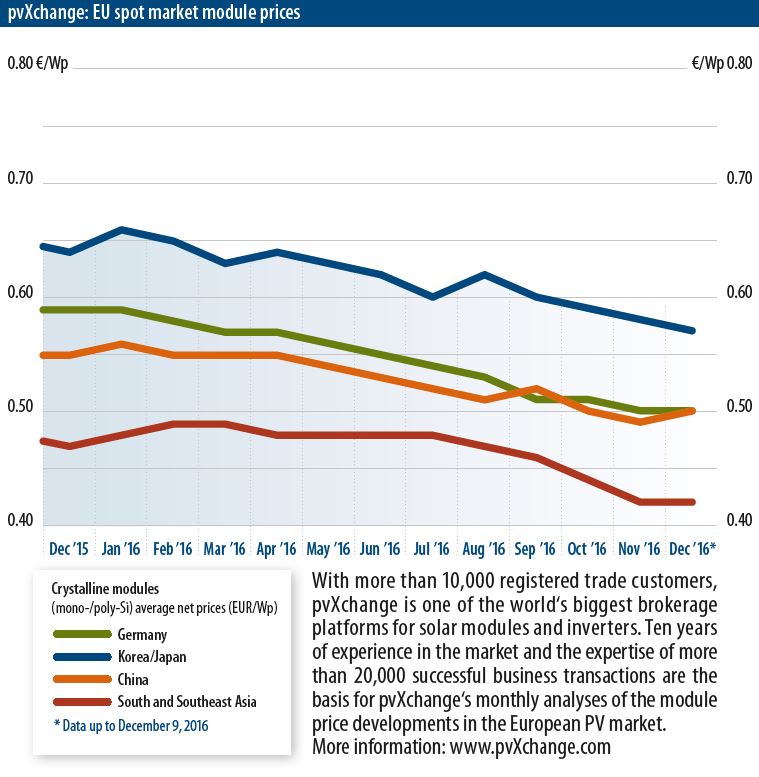

We can look back on an unusually quiet end to 2019, as the final weeks of the year lacked the usual hustle and bustle of the global PV market. As a result, there are no significant price cuts in sight for 2020. Martin Schachinger of pvXchange looks back over the second half of the past year, and what’s to come in the months ahead.

We can look back on an unusually quiet end to 2019, as the final weeks of the year lacked the usual hustle and bustle of the global PV market. As a result, there are no significant price cuts in sight for 2020. Martin Schachinger of pvXchange looks back over the second half of the past year, and what’s to come in the months ahead.

How did the solar industry fare in 2019? It was a year of climate strikes, falling module prices, feed-in tariff cuts, and patent lawsuits. Here, I’ll continue to shed light on the situation, based on key events throughout the second half of the year.

July 2019

Thanks to cuts in the incentives for new medium to large installations introduced to the German market in April, small systems – preferably with hybrid inverters in combination with storage – increasingly caught the attention of those interested in photovoltaics. Many installers, in Germany at least, almost exclusively built small plants up to 30 kW this year. Although German inverter manufacturers such as SMA and Kostal face increasing pressure from major Chinese suppliers, they have managed to retain a large market share in the small-plant segment. Even so, established inverter manufacturers seem to have been caught off guard by the uptick in demand, with the result that most devices in the 5 to 25 kW range sold out very quickly in the June-July time frame. Suddenly there were delivery delays of several weeks or even months in the PV industry again.

It is not easy to understand why this bottleneck occurred, as the forecasts for 2019 had predicted precisely this. Storage systems for PV plants in this size category were also scarce at times, and still are in some cases. At mid-year, however, there were also fears that modules were headed for a bottleneck. News from China suggested we could see an unprecedented year-end rally. After a comparatively weak first half, subsequent auctions were held for systems with a total capacity of around 22.7 GW. At the same time, the forecast for 2019 in China was raised to around 40 GW. It has now become clear, however, that this boom failed to materialize, and the feared shortage of modules was unfounded.

August 2019

Numerous social and interest groups, such as the German Solar Industry Association (BSW), had been calling on the German government for months to remove the 52 GW cap in the Renewable Energy Act (EEG). Volker Quaschning of the Berlin University of Applied Sciences (HTW) sent Federal Economics Minister Peter Altmaier a discarded toilet lid with the inscription “Get rid of the PV lid.” There were also voices within the GroKo (Germany’s Grand Coalition) that the CDU/CSU parties, the senior partner in the coalition, would ultimately have to abandon its blockade of lifting the cap.

There was broad speculation about the consequences of retaining the cap: The fixed upper limit, which would abruptly cut off incentives under the legislation, would have an increasingly negative effect on decisions to invest in PV plants.

Meanwhile, although elimination of the 52 GW cap has been incorporated into the climate package, the question of a possible follow-on regulation has not been conclusively settled, and no concrete date has been set for doing so.

October 2019

Because no module bottleneck occurred, inverters and storage systems became available again – so what else could stand in the way of installing photovoltaics on every available surface, thus facilitating the rapid implementation of the energy trangsition? A lack of qualified technicians!

Following the huge collapse in the solar industry after 2011, solar electricians moved to other segments, with the result that – in Germany, at least – there was a shortage of workers and specialists in the PV sector. Many installation jobs could not be taken on or, if they could, only with long delays – lead times for electricians’ work rose steadily to as much as five months in September. This bottleneck alone has given rise to fears that if climate targets in the electricity sector are to be reached at all, it will only be with considerable delays. In the coming years, huge investments will have to be made in research, and in training new skilled workers. For this purpose, the German government has earmarked …nothing.

December 2019

Leaders had another chance to set a decisive path forward at the UN Climate Change conference in Madrid last month. To encourage delegates to take action, there was another major climate strike on Nov. 29, with hundreds of thousands of participants worldwide. Once again, however, only half-hearted declarations of intent were drawn up and the much-needed drastic changes in our resource-consuming economic system were neglected. So the groups working against climate change will probably have to continue striking. Because there is no alternative, even if many people may still hope for a miracle. The negative signs of global warming are already clearly visible.

Future outlook

Renewable energy will play a major role in the sector; this is now the broad consensus. To this end, the obstacles that currently hinder their use outside the government-sponsored framework must be quickly removed. These include bureaucratic hurdles in the implementation of tenant electricity models and citizen energy systems, excessively high grid transmission fees, and taxes.

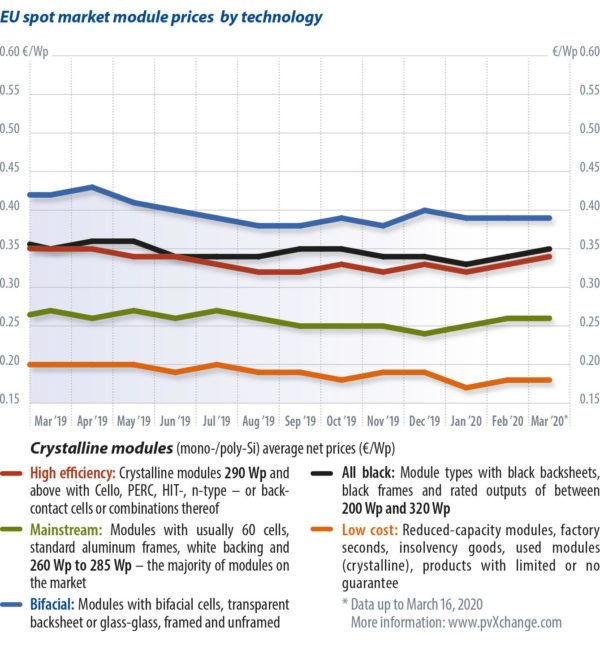

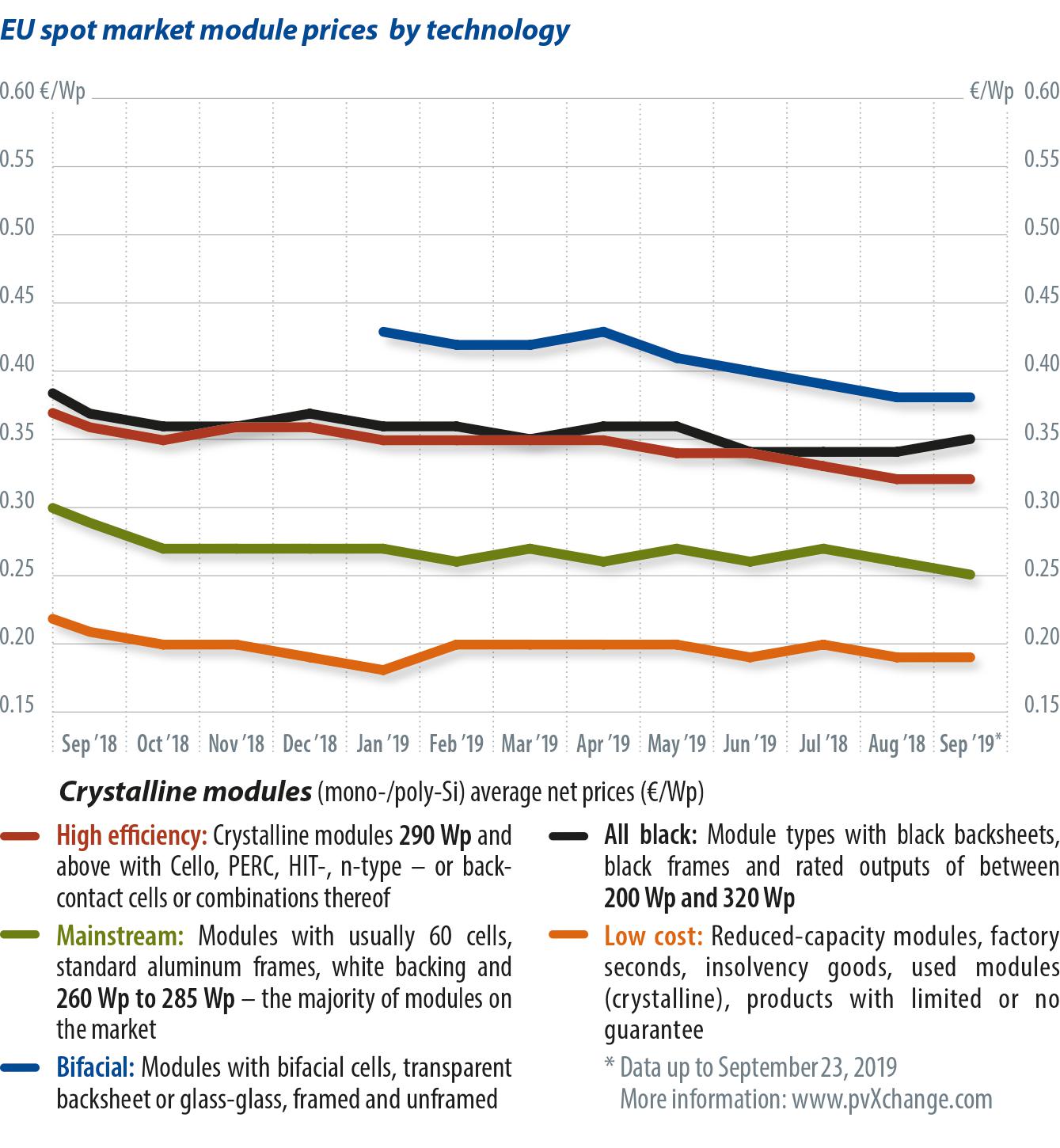

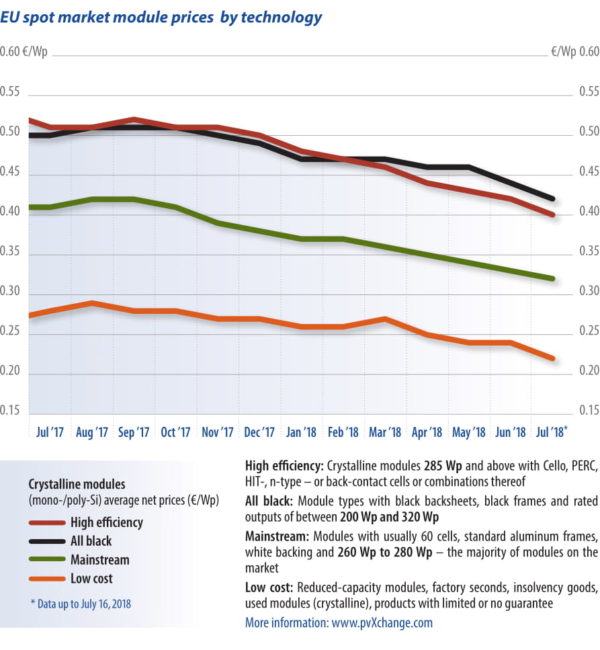

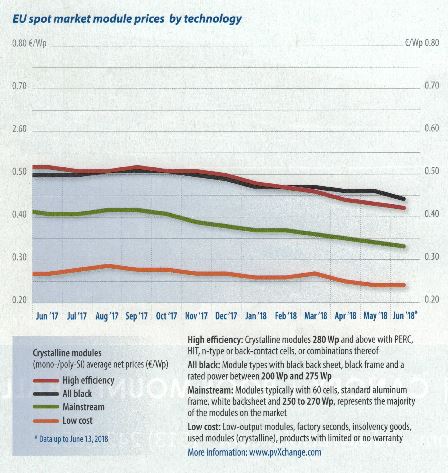

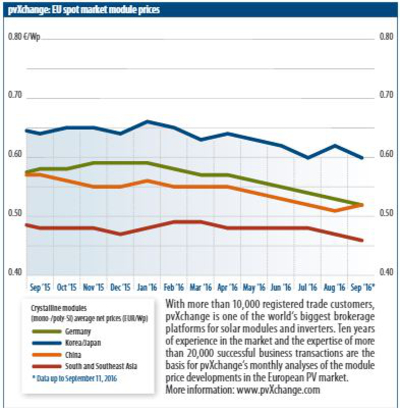

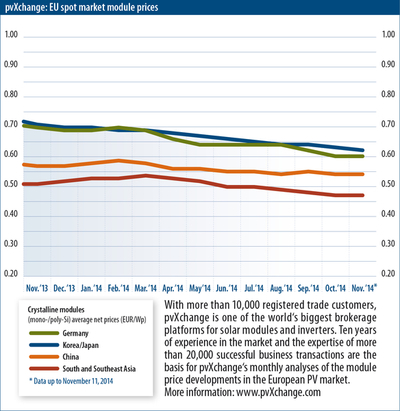

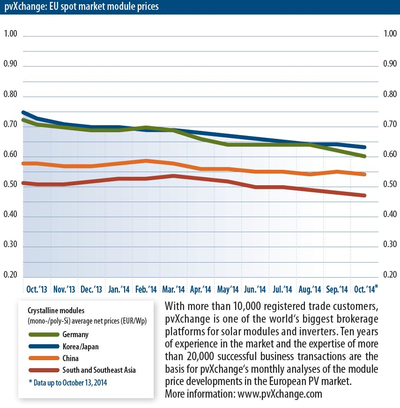

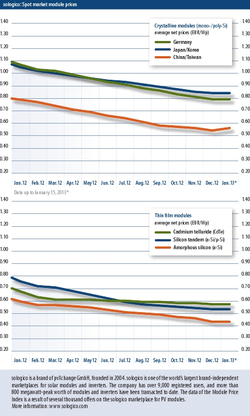

On the technology side, we will see a further increase in module efficiency, although multicrystalline’s days are probably numbered. Nearly all major manufacturers have converted to purely monocrystalline. Price levels will at best continue to decline slightly – that is, apart from inventory clearance or emergency sales. The end of the downward price spiral seems to have been reached, at least for silicon products, due to more efficient production technologies, and above all economies of scale. This is shown in the graphs in the pvXchange price index, which have been moving sideways for months.

An interesting trend in the wind sector was seen at this year’s New Energy World Forum in Berlin: floating wind turbines. The elimination of foundations anchored in the seabed allows the development of new offshore areas and the expansion of wind turbines beyond the 10 MW capacity limit. Nevertheless, hope remains that the new distance regulation for onshore wind turbines in Germany will be reconsidered. These turbines help to avoid oversized and expensive power lines, which have similar public acceptance problems as large modern wind turbines. The involvement and financial participation of local residents is an effective means of improving acceptance. In this area, we can look forward to more new ideas and innovative models in the future. The climate crisis cannot be tackled by individuals; it has to be a group effort.

Martin Schachinger, pvXchange.com

December 2019: A year of change – part 1

To hear our policymakers talk, the energy transition – an unprecedented, radical and rapid transformation of our energy and economic systems – is now in full swing. So much is being reformed and so much is being accomplished – we can’t possibly do more! But reality paints a completely different picture. Even for the big energy companies, which once leaned on the brakes in the face of change, the current pace of the federal government has become too sluggish. The utilities have started to set the pace for change to prepare quickly for a future in which emissions-free energy will be generated exclusively from renewable sources. With or without climate targets, for the utilities it is a matter of developing a survival strategy in a disruptive market.

To hear our policymakers talk, the energy transition – an unprecedented, radical and rapid transformation of our energy and economic systems – is now in full swing. So much is being reformed and so much is being accomplished – we can’t possibly do more! But reality paints a completely different picture. Even for the big energy companies, which once leaned on the brakes in the face of change, the current pace of the federal government has become too sluggish. The utilities have started to set the pace for change to prepare quickly for a future in which emissions-free energy will be generated exclusively from renewable sources. With or without climate targets, for the utilities it is a matter of developing a survival strategy in a disruptive market.

At the end of 2019, we can look back on a year of public protest in the form of climate strikes and roadblocks, which began with Greta Thunberg in Sweden and have now spread across the globe. Young people are no longer standing idly by and watching as policymakers and businesspeople frivolously jeopardize their futures by continually adhering to conventional energy sources and mobility concepts.