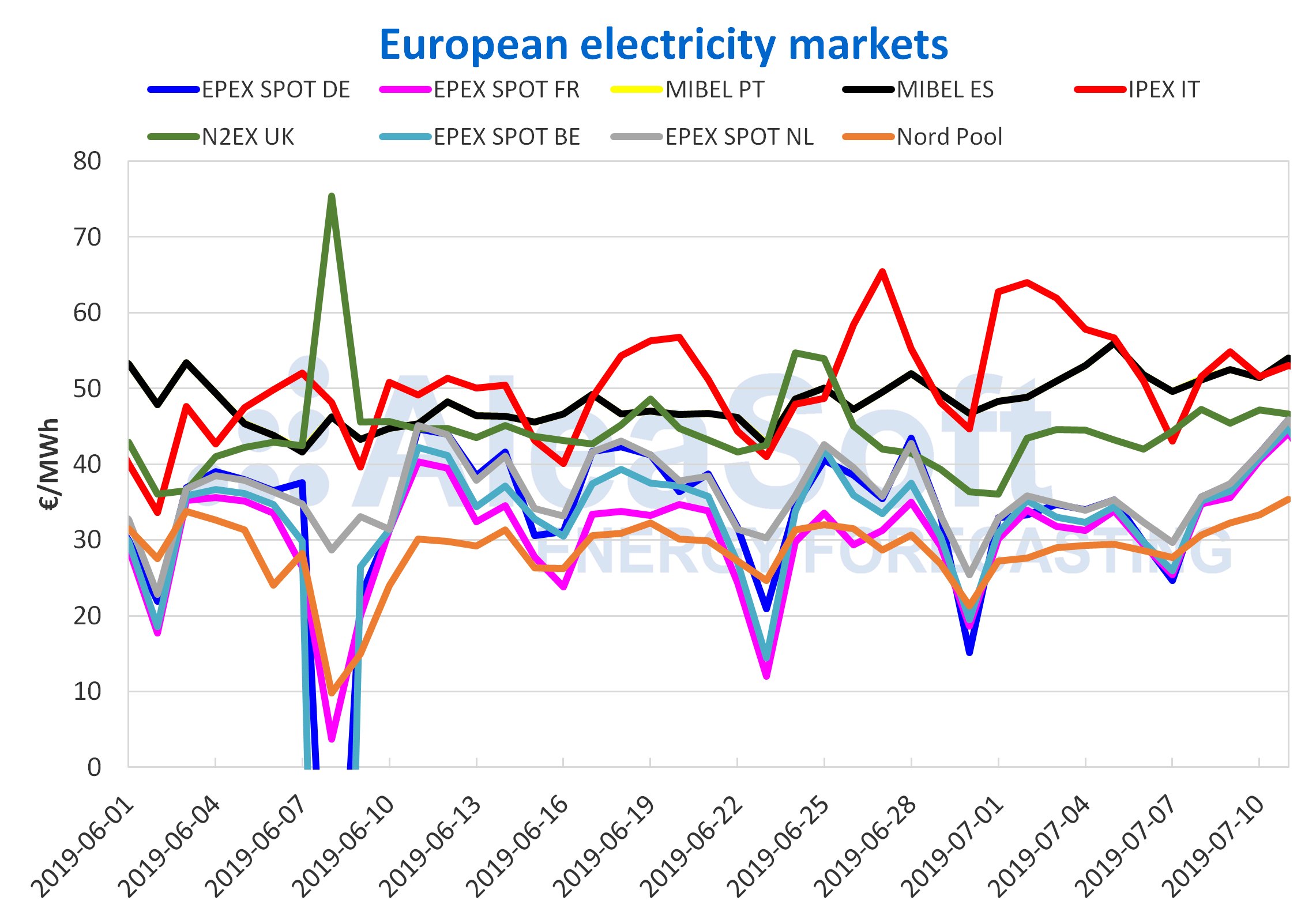

On Saturday and Sunday, the MIBEL electricity market in Spain and Portugal had the highest average price in Europe, with €51.78/MWh and €49.62/MWh respectively. And, since the beginning of the week prices continued to be among the highest in Europe as is usually the case. Between Monday and Wednesday, although MIBEL was not the market with the highest price on the continent, it was close, trailing the IPEX market in Italy, until yesterday when it again led electricity prices in Europe, with €54/MWh. In the first four days of the week the price increased by 4% compared to the same days of last week.

European electricity markets

However, the rise of the MIBEL market may seem insignificant compared to those observed in most European electricity markets, where the average price between Monday and Thursday rose somewhere between the 11% of the N2EX market of Great Britain and the 22% of the EPEX SPOT market of France, compared to the average price between the previous Monday to Thursday period. This week the exception was the IPEX, which fell 14%, after falling down to prices slightly above €50/MWh. Last week prices were above €60/MWh.

The group of markets with the lowest prices, including the EPEX SPOT markets of Germany, France, Belgium and the Netherlands as well as the Nord Pool market of the Nordic countries, is the one that experienced the biggest recovery. On Monday their prices were around €30/MWh in the Nord Pool and €35/MWh in the EPEX SPOT markets. Yesterday their values were around €35/MWh and €45/MWh, respectively. In the group with the highest prices, this week the IPEX and MIBEL markets were above €50/MWh and the N2EX was above €45/MWh.

Sources: Prepared by AleaSoft using data from OMIE, EPEX SPOT, N2EX, IPEX and Nord Pool.

Brent, fuels and CO2

The Brent oil futures prices for September on the ICE market settled on Wednesday at $67.01/bbl, increasing by almost $3/bbl compared to the previous day – 4.4%. Since the end of last week, prices were slightly above $64/bbl and remained at that level for the first two days of this week. Wednesday’s price increase was conditioned by circumstances such as the decrease in United States reserves, possible interruptions in crude production in the U.S. as a result of a storm in the Gulf of Mexico and a new escalation in tensions with Iran after a failed attack on a British oil tanker.

The futures of TTF gas on the ICE market for August continued recovering this week and settled on Wednesday at €12.13/MWh – 20% above the two-year low seen on June 27 and reaching values near those seen at the beginning of June.

API 2 coal futures prices on the ICE market for August settled upwards again on Wednesday at $60.10/t. Since May 23, this product has not traded above $60. The upward trend the market is experiencing since the end of June slowed temporarily on Tuesday, when it was traded downwards, 3% below the settlement prices of the beginning of the week.

CO2 emission rights futures prices on the EEX market for the December 2019 reference contract settled at €28.20/t on Wednesday, after remaining between €26 and €27 during the last three weeks. That price on Wednesday represented an increase of 19% on the lowest prices of the last two months – €23.74/t on June 3.

Electricity futures

The electricity futures of Spain and Portugal on the OMIP market settled on Wednesday 2.9% higher than the previous Wednesday. In the case of Spanish electricity futures on the EEX market, Wednesday’s session ended with an increase of 2.6% in the same period. After those increases, the value of the products returned to be comparable to the first days of June, after settling between June 19 and 20 at their lowest values since the beginning of the month.

The futures for 2020, on the OMIP and EEX markets for Spain and on the OMIP market for Portugal, maintained an increasing trend since early June. That trend increased on Wednesday in parallel with the CO2 emission rights future, settling at its highest value for more than two months of €56.30/MWh in the case of Spanish futures on the EEX and around €57 for Spanish and Portuguese futures on the OMIP market.

French and German futures on the EEX market for the next quarter remained on the rise since last Friday. In France, the settlement price on Wednesday was 6% higher than on the previous Wednesday and in Germany the increase was 7%. The futures of France and Germany for 2020 are maintaining an upward trend since the beginning of June and settled on Wednesday at €52.40/MWh and €50.40/MWh, respectively.

Mainland Spain, wind and PV energy production

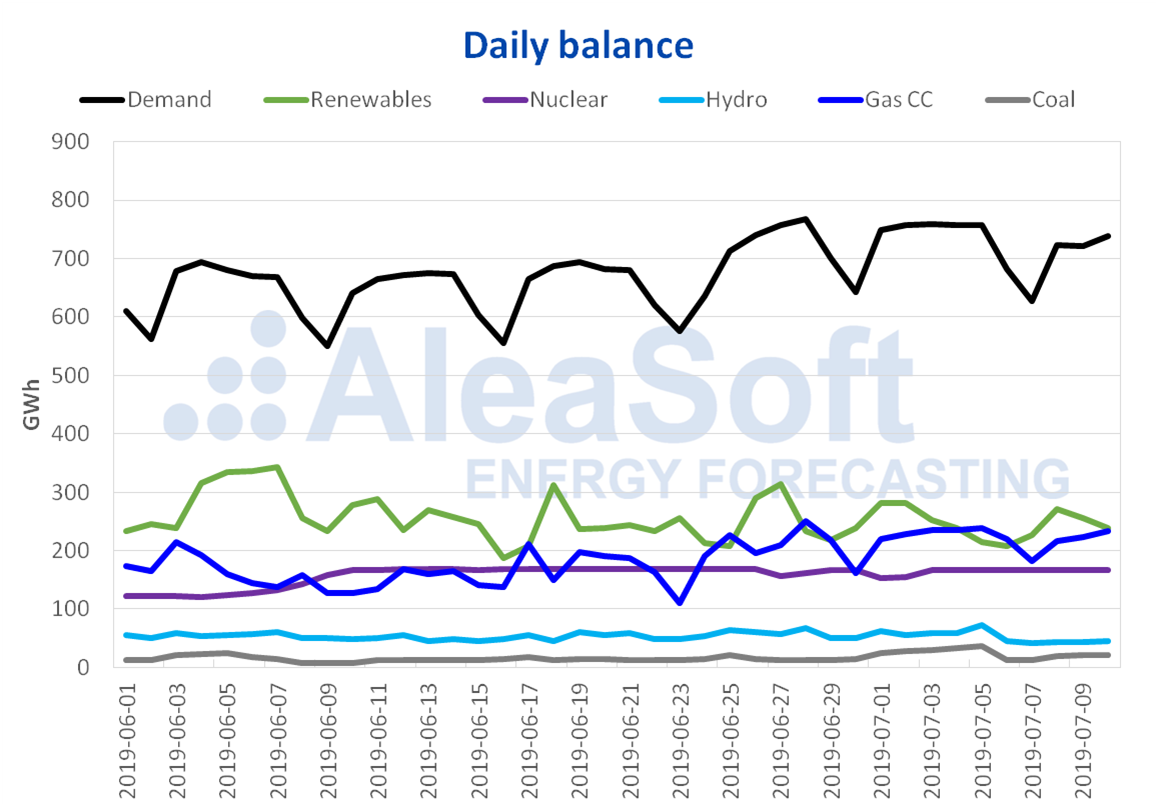

In mainland Spain the beginning of this summer week was less hot, with a fall of 0.3 degrees Celsius in average temperatures compared to the first three days of last week. That caused electricity demand to fall 3.9%.

Wind energy production rose 11% so far to Wednesday, compared to the average values of last week. For next week it is expected it will recover slightly, according to AleaSoft.

For PV and solar thermal energy production in the first three days of the week, output rose 3.1% compared to the average of last week. At AleaSoft it is expected solar energy production will also rise next week.

All nuclear power plants are operating. From Monday to Wednesday, nuclear energy production increased 5.1% compared to the same days of the previous week, in which there was a short, unscheduled halt at the Ascó II plant, on the Monday and Tuesday.

Hydroelectric energy production decreased again in the first three days of the week, compared to July 1-3. This time the fall was 25%.

Sources: Prepared by AleaSoft using data from REE.

According to the latest Hydrological Bulletin produced by the Ministry for an Ecological Transition, the level of hydroelectric reserves is currently 11,487 GWh, representing a decrease of 2.7% and 320 GWh compared to last week. The currently available reserves are equivalent to 76% of those available a year ago. On the other hand, reserves now occupy 49% of the total capacity of 23,281 GWh.