Uzbekistan is steaming ahead in the race to carbon neutrality

Uzbekistan can be described as a “good performer.” Since 2016, it has enacted significant economic, social, and political reforms and changes, and has promoted renewables, including solar. How are these actions paying off today?

An immediate, tangible, example of the dire need to act against climate change in Uzbekistan are the projected reductions in water resources and changes in rainfall patterns that are expected to lead to long droughts, thus putting significant portions of its population at risk of food and water insecurity.

Water shortages are causing diminishing crop yields that will be insufficient for the country’s fast-growing population. This problem is magnified by the drying up of the Aral Sea which has already lost 57% of its area, 80% of its volume and 64% of its depth over the past four decades.

To tackle this, the country has set very strong climate change targets via several initiatives that aim to reshape the energy mix. They include:

- Reducing GHG emissions per unit of GDP by 35% compared to 2010 levels, by 2030

- Increasing the share of RE sources to 25% of total power generation – double the energy-efficiency indicator relative to the level of 2018

- Halving the energy intensity of GDP

- Decreasing industrial consumption of natural resources

- Achieving carbon neutrality by 2050

Uzbekistan has understood the challenge and the need for support in terms of funding and technology providers, hence the need to attract foreign investors. It is therefore worth exploring how the country has successfully managed this transformation and what is the current status of its renewable energy and PV markets there. This could offer interesting international growth opportunities to potential strategic partners.

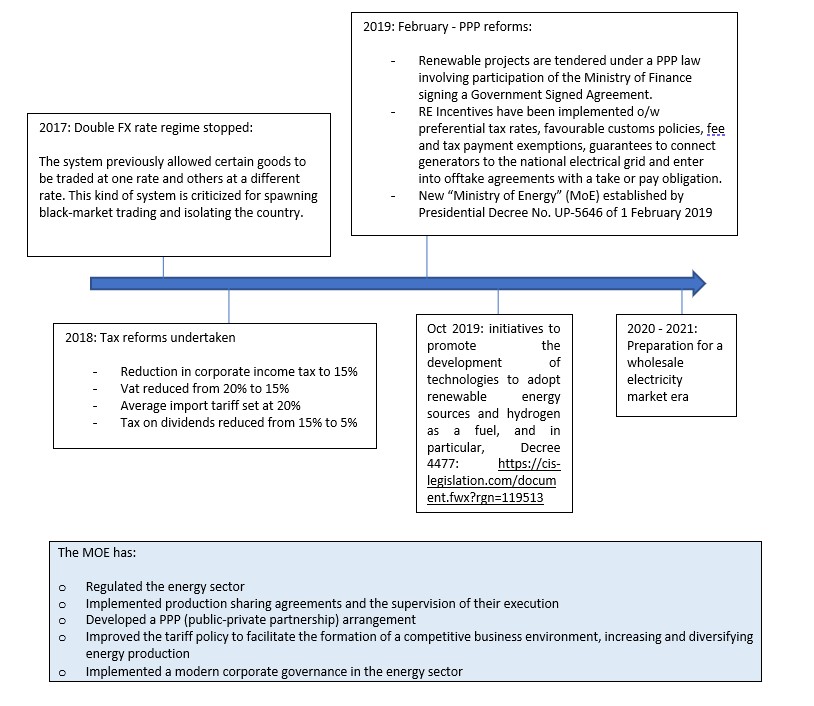

Resetting the energy legal and regulatory framework

Since arrival of the current President Shavkat Mirziyoyev in 2016, who was the former Prime Minister, re-elected in October 2021, the Government of Uzbekistan has adopted a mid-term development strategy, “The Strategy of Actions for 2017-2021.” In general, thanks to the comprehensive and deep economic reforms, the country’s economy has shifted from its former Soviet model to a more dynamic one, where the living standards of the population have significantly improved.

The reforms have also improved the investment climate, removed major market distortions, and unlocked potential for private entrepreneurship. As a result, Uzbekistan’s economy has become a much more open and market-oriented economy.

Here is a summarized list of the main reforms and investment-related laws necessary for promoting renewables that have been adopted over the last five years:

These reforms immediately translated into a radical restructuring of Uzbekenergo JSC, the State-owned, monopolistic, utility company. Three joint-stock companies have since been organized under the umbrella of the latter: Thermal Power Plants, National Electric Networks (Transmission operation) of Uzbekistan, and Regional Electric Networks (Distribution operator).

A new Decree 4477 has also been introduced to foster a green economy transition. It:

- Increases the energy efficiency of key branches of the economy

- Imposes diversification of consumption of energy resources and development of the use of renewable energy resources

- Proposes adaptation and mitigation of the consequences of climate change, increases efficiency of use of natural resources, and preserves natural ecosystems

- Supports development of financial and non-financial mechanisms for establishing a “green” economy

Adapting tariffs to new consumption and power demand

Changes to the country’s law in 2020 rapidly led to an overhaul of the tariff structure for the electricity and natural gas sectors. Like in many other countries, a differentiated flexible electricity tariff for the population by the time of day, working/weekend days was approved.

Thus, consumers now receive the right to conclude contracts either at a tariff differentiated by the time of day (when, as a rule, electricity is cheaper at night), or at a single rate tariff (that is, the same price of electricity during the day). In addition, a tariff differentiated by consumption volumes (using the base rate) is used.

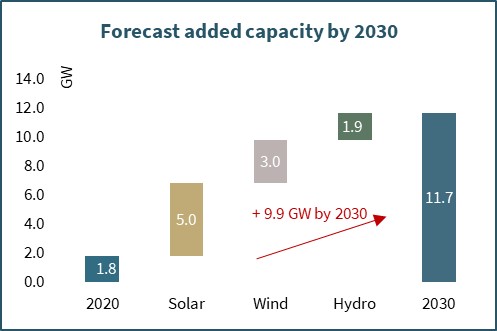

At the end of 2020, the Concept Note for Ensuring Electricity Supply in Uzbekistan in 2020-2030 was also approved. This envisages an increase in generating capacity from 12.9 GW in 2019 to 29.3 GW in 2030. It is also planned to achieve up to 8 GW of electricity generated from renewables, comprising 3 GW of wind farms and 5 GW of solar farms.

However, these targets were not sufficient, so 2021 was announced as the year of the launch of country’s wholesale electricity market. In Q1 2021, a draft of Presidential Resolution “On Additional Measures to Reform the Electric Energy Industry” was announced which aims to establish a competitive electricity market in Uzbekistan between 2020 and 2025.

The draft provides for the establishment of an independent regulator in charge of electricity and natural gas, which will not be part of the government as it is today but will be subordinate to the president and the parliament. Beyond standard control and licensing roles, some relevant functions of this institution envisaged in the draft resolution are:

- Developing and approving tariffs for generation, transmission, distribution, and sales of power

- Reducing the government’s share in the energy sector, creating favorable conditions for attracting private capital, and preventing unreasonable price increases in the supply of electricity to end users

- Unbundling the JSC “National Electric Grid of Uzbekistan” and establishing a new “Uzpowertrade” JSC in charge of the export and import of power, with the right to directly purchase power from energy producers and place it for sale online at free prices

These changes open the doors to the implementation of the Concept of Transition to a Competitive Electricity Market for 2021-2025 which could lead to a competitive electricity market, improve the quality, reliability, and stability of power supply through effective management of the power industry by the transformation of state-owned companies, and form a competitive wholesale and retail power market.

The concept establishes the following models for the competitive wholesale electricity market:

- Trade under bilateral agreements (monthly trade): This first stage provides for the liberalization of electricity companies and obtaining of licenses for private enterprises wishing to sell electricity. This market-based approach is expected to improve product quality and help reduce prices.

- Day-ahead trade: During the second stage transition to a competitive wholesale electricity market, an operator of the electricity distribution system will be set up, and the functions of selling electricity to consumers will gradually be transferred to suppliers. These suppliers will be entitled to sell electricity to consumers via a license. Consumers will be able to purchase electricity through an online trading platform or through any supplier.

- Intra-day trade: The third stage is “Intraday (hourly) sales” which implies the online purchase of excess or sale of deficient volumes of hourly production and consumption of electricity that will be carried out on the trading floor.

This note has not yet been fully voted on due to the current geopolitical events but is underway.

Renewable projects and funding requirements

Mixing ambitious sustainability targets (like carbon neutrality) and modern energy trading mechanisms requires significant investments whether from a grid perspective, or modernizing Soviet-era infrastructure, raising the quality and storage of power, and the management of technical intermittency.

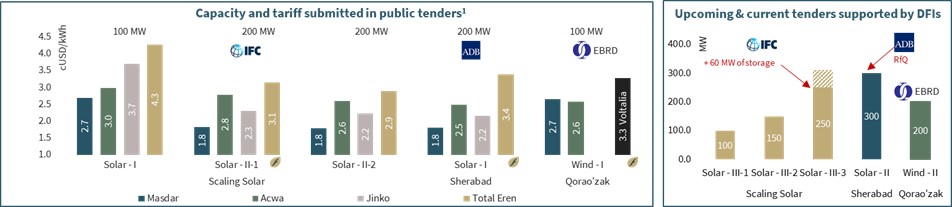

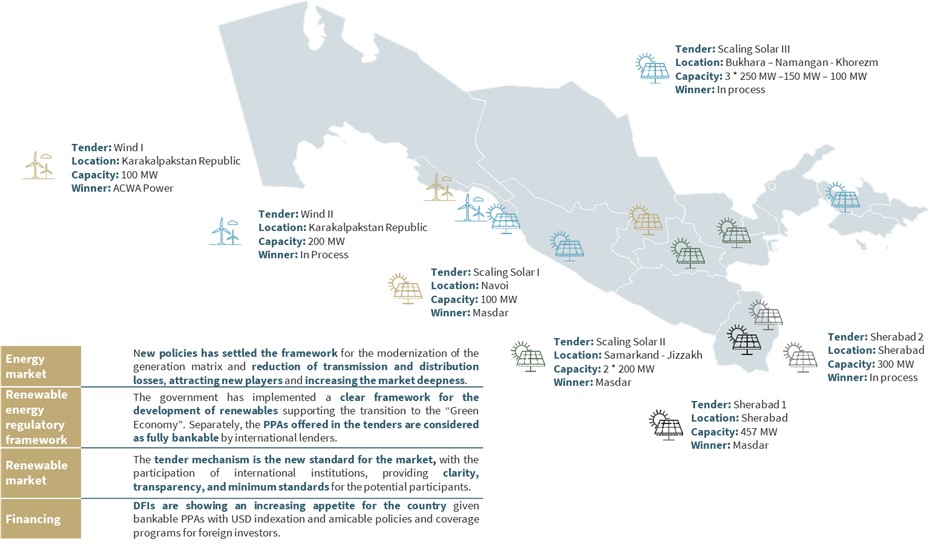

In these respects, the laws passed in 2019 on renewable energy and PPPs have paved the way for numerous build–operate–transfer wind and solar tenders to be organized by 2022. Leading development finance institutions, like the International Finance Corporation, Asian Development Bank, and the European Bank for Reconstruction and Development, are supporting the government in these tenders.

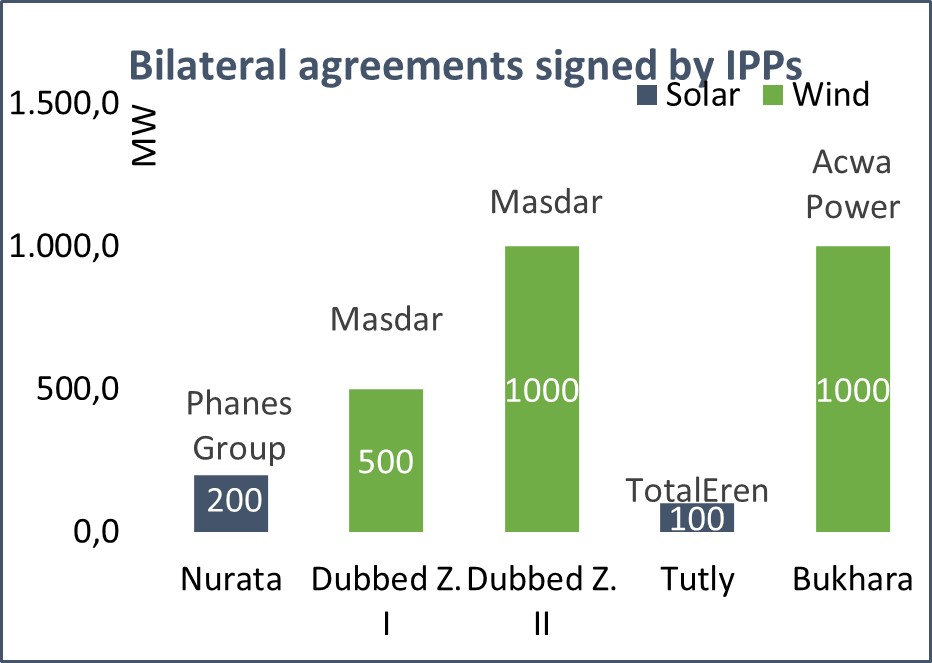

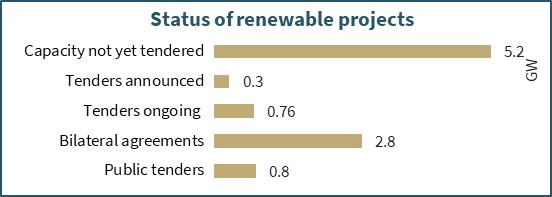

To date, five tenders have been implemented for a minimum of 800 MW in wind and solar. These tenders consist generally in the design, financing, construction, operation, maintenance, and transfer of large-scale power plants. They have thus far been successful for the offtakers as they attracted leading developers such as Masdar, Acwa Power and Total Eren, with record low tariffs.

Having said that, one should not forget the risk for a government to offer a market to a restricted number of players. Allocating 92% of a whole sector to two companies does pose risks. Evidence of that is the bid ratio (number of final bidders to qualified applications) that the tenders attracted, which is low (sometimes up to 25% only) and between 4-10% if compared with Expressions of Interest. This means some partners will be discouraged, considering the competition too fierce and unbalanced.

See tables below for more details:

Uzbekistan plans to develop around 9.9 GW of renewables by 2030, of which 5.24 GW are to be tendered by 2030. Considering the former remarks, the government adapted the rules to more balanced proposals whereby one bidder can only be allocated one project for the segment they qualify have been imposed. This should promote the diversification of power suppliers.

In addition, laws have been adapted to ensure the bankability of projects over the tenders. For example, providing SPV creation was not part of the original model. Today, current tender models propose, among other benefits:

- Government exemption for PPP projects that prohibit foreign-currency indexation for payments made in Uzbek currency. Most PPAs with NEGU will now be indexed to US dollars.

- Modifications to the land code now allow lease rights for land to be pledged as security to international lenders, though land ownership is still restricted to Uzbek nationals.

- PRG, MIGA support is available to encourage commercial banks in a context where the offtaker is an untested entity and suffers from the “limited” creditworthiness of the Uzbek government, which was recently rated BB- by Fitch

All these elements have been successful in mitigating a liquidity risk as individual finance institutes have confirmed appetite for long term PPAs structures.

Conclusion

A general sub-investment grade risk remains, particularly against the backdrop of the Russian invasion of Ukraine which has direct implications for Uzbekistan. These implications include rising external security risks given the potential for deteriorating political relations with Russia.

The war will also impact Uzbekistan economically due to an expected weaker external demand, higher inflation, and lower remittance inflows. However, the government has demonstrated strong resilience and perseverance in reform implementation to reach its targets.

The market appetite appears to be there and confirms the interest in stakeholders to participate in the transformation of the Uzbek power model.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment