Expect the roofs of global distribution facilities, manufacturing plants, industrial estates and retail stores to sprout solar at a steady rate of watts over the coming months. A still relatively underserved market for solar systems, the commercial and industrial (C&I) sector will become increasingly renewable-energy hungry as governments twiddle the dials on incentives that help them deliver on decarbonization targets, and fossil fueled electricity generation continues to ride the price rollercoaster.

“The economics behind solar uptake are based on the retail electricity price versus the cost of putting solar on your roof, the solar resource and the government incentives to go renewable,” says David Dixon, senior analyst for Australian renewables at Rystad Energy.

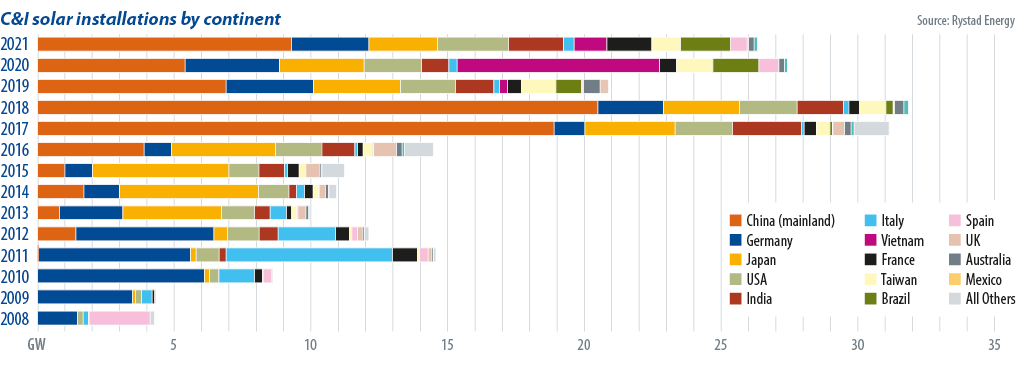

Rystad Energy further observes that the highest uptake regions for rooftop C&I solar have high retail electricity prices and large available rooftop space, which would put Germany ahead of China among countries heading for the sun. And historically that holds true.

Germany’s C&I sector began its rooftop uptake in response to incentives such as high feed-in tariffs way back in the early 2000s, when PV modules were still manufactured in the central European power house, and electricity prices were already high. In the 2010s, however, China took over the major-market mantle (as well as burgeoning module manufacturing). And as Dixon points out, “policy settings can have extreme effects in China, where a couple of percentage points here and there make a huge difference because of the size of the market.”

Different drivers

Going forward, analysts at IHS Markit read the incentivized C&I runes a little differently, placing Brazil a distant second to China, and Germany in third place – at least for 2022. Siqi He, research analyst for clean technology and renewables for IHS Markit, says that figures indicate that China will install 36 GW of C&I rooftop solar in 2022. Brazil will put 4.6 GW on its C&I rooftops, while Germany will pump out an extra 4.1 GW from C&I.

A significant driver in China, says He, has been the National Energy Administration’s mid-2021 call for a number of counties to be nominated for a trial program to promote rooftop solar pilot projects. IHS Markit’s figures indicate that 676 of China’s mostly developed counties or cities have already been approved for the pilot program.

In Brazil, the approval in August 2021 of a new distributed generation regulatory framework will see the gradual rescinding of grid access privileges (such as exemption from grid charges) for existing micro (up to 75 kW) and mini (75 kW to 5,000 kW) distributed systems, up to 2045. But a 12-month grace period will see thousands of systems apply for access in the meantime, so that they can bask in the benefits for as long as possible. “We expect the absolute number of C&I installations in Brazil to slow down from 2024 [at the end of the grace period,” says He.

In Germany, a combination of high retail electricity prices, the adoption of a number of rooftop PV incentives, as well as geopolitical factors are at play. The EU as a whole is seeking to reduce its reliance on Russian gas by diversifying its gas supplies into renewable gases and transitioning heating and power generation away from gas and into renewables. Germany itself, says He, does have a fair bit of C&I solar installations already, but further policy changes will drive a renewed boom. He cites one new policy as Germany’s 2021 raising of the solar system size cap for surcharges payable on self-consumed electricity from 10 kW to 30 kW – which favours C&I systems.

Rising fortunes

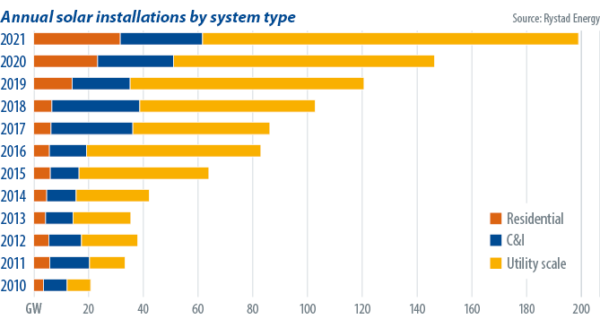

Globally, IHS Markit expects 81 GW of C&I rooftop solar to be installed in 2022, and for this number to increase by 54% by 2026, when it forecasts 125 GW of installations.

Dixon says inverter fortunes largely follow the solar market – both on the utility and smaller scale. However, he adds that any likely dip in solar uptake due to currently higher module and/or shipping costs, may be made up for on the inverter side by an increase in battery sales, where the addition of a battery might require installation of a new, bi-directional inverter system that converts solar energy for storage, and from storage to useable current.

But this potential trend, he explains, also has its subtleties in that many energy storage systems have a built-in inverter therefore discounting the need for an extra inverter purchase, and that consumers of solar systems today are taking advantage of new battery-ready inverters, in anticipation of installing a battery sometime in the future.

IHS Markit’s He adds that inverter manufacturers are “seeing the potential” in growing C&I demand for larger rooftop systems, “and diversifying their product portfolios.” That is, “some suppliers known for their central inverters, or for catering to utility-scale projects are now releasing smaller string inverters for C&I’s upscaled rooftop installations; and suppliers of microinverters that were specified for the residential segment are now releasing larger multi-module micro inverters suited to the commercial market.”

China’s previously mentioned County Rooftop PV Development Pilot Program, she says, is of a scale large enough to have inspired some central inverter manufacturers to amplify their string section.

The global C&I rooftop solar segment still has its challenges, such as system ownership, maintenance responsibilities and distribution of benefits between building owners and tenants, but as countries push to decarbonize, they will strive to make the economics stack up for this energy-hungry sector.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.