Solar power plants with smart batteries: It’s just a matter of time

At the end of 2021, the total capacity of the solar power plants throughout the world was estimated to be 940 GW. According to the forecasts of solar association SolarPower Europe, the total capacity could reach 2 TW by 2025. With the rapidly growing popularity of solar power plants, experts predict that the next breakthrough in this sector will be smart batteries. In the future, solar power plants will not be able to operate without them.

Strengthening consumer protection in the off-grid solar industry

Almost half a billion people are served by the off-grid solar industry, and a growing number of these via Pay-as-you-go (PAYGo) asset financing. For many consumers, not only is the solar product their first access to modern energy but it may also be their first access to finance. The impact of this can be huge – the 60 Decibels Energy Benchmark reveals that 92% of consumers report an improvement in quality of life after purchasing their off-grid solar (OGS) product. On the other hand, consumers of OGS are exposed to product, service, and financial risk that companies must mitigate and balance with sustainable growth objectives.

Why is green energy infrastructure booming despite global economic woes?

The Covid-19 pandemic and resulting economic fallout have had a variety of impacts on the clean energy transition, with some sectors being more affected than others. Earlier this year, the International Energy Agency (IEA) warned of slowed progress towards sustainable energy goals due to Covid-19 and reversed progress in many areas crucial in reaching net zero, such as energy efficiency, clean cooking, or access to electricity. There is one sector, however, that has shown remarkable resilience since the beginning of the pandemic and has been able to maintain, and even accelerate, its rapid growth since 2020: green energy infrastructure.

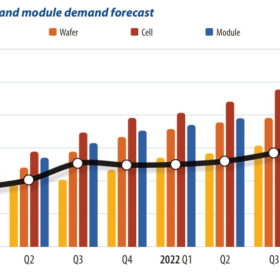

Europe can compete effectively with Asian solar manufacturers with innovative long-term PV technology solutions

The world’s energy sector is concentrated in solar, wind, electricity transmission/distribution and hydroelectric power. For example, investment in solar power plants alone is higher than investment in natural gas, coal-fired and nuclear power plants combined. This is encouraging, but another fact is worrying: China’s exports of solar modules to Europe in the first four months of 2022 were 2.5 times higher compared to 2021. In April alone, nearly 8 GW of solar modules worth more than €2 billion were imported from China into Europe.

Uzbekistan is steaming ahead in the race to carbon neutrality

The war in Ukraine continues to disrupt the global energy sector and, combined with the recent heatwaves affecting Europe, the need to restructure economies is starker than ever. Luckily, there are some countries that have kept working on their energy transition reforms and taking tangible actions towards tackling climate change. Uzbekistan is one of them.

Considerations for solar projects during heat waves

High temperatures can affect different components of PV systems. Inverters can fail, the efficiency of solar modules can decline, and existing cell damage can become worse. However, investors, planners, and operators can adjust to heat waves in a number of different ways.

Italy publishes new national guidelines for agrovoltaic plants

On June 27, the Guidelines for The Design, Construction and Operation of Agrovoltaic Plants were published in Italy by the Ministry of Ecological Transition, in coordination with the Council for Agricultural Research and Analysis of Agricultural Economics (CREA), Gestore dei Servizi Energetici S.p.A. (GSE), the National Agency for New Technologies, Energy and Sustainable Economic Development (ENEA), and Research on the Energy System S.p.A. (RSE). From now on, developers and, in general, RES plant owners will have to consider the principles herein outlined, to have their plants classified as agrovoltaic.

Rays of solar hope for Europe: A Midsummer reflection

For centuries, cultures in Europe have marked their calendars to celebrate Midsummer and the Summer Solstice. Traditionally a time to enjoy bright evenings, and the light and hope of the sun, the Summer Solstice falls on June 21. On the longest day of sunlight in 2022, Europe has much to hope for. After difficult pandemic years, enduring cost of living and energy price hikes, and the on-going, unprovoked, Russian war on Ukraine, Midsummer gives us a small moment to reflect on, and hope for, brighter times ahead.

As EVs drive off with Li-ion supply, the push to stationary storage alternatives accelerates

The throes of a lithium shortage are increasingly upending long-term supply strategies and stoking demand for alternative technologies for stationary energy storage projects. Once seen as synonymous with renewable batteries, stationary Li-ion faces strong headwinds due to rapidly accelerating demand from the automotive sector as EVs capture the mainstream.

No end to solar supply/demand imbalance

The solar supply chain problems that began last year with high prices and polysilicon shortages are persisting into 2022. But we are already seeing a stark difference from earlier predictions that prices would decline gradually each quarter this year. PV Infolink’s Alan Tu probes the solar market situation and offers insights.