Roth: Trump administration could end bifacial tariff exemption

From pv magazine USA.

If there is one consistent aspect of the trade actions undertaken by the Trump administration, it is inconsistency.

In June, U.S. solar developers and Asian cell and module makers celebrated when federal trade authorities announced they would exclude bifacial products from the Section 201 tariffs imposed in February 2018.

The prospect of importing tariff-free bifacial modules – which are not significantly more expensive than their monofacial counterparts and offer additional output – offered potentially lower costs for PV systems. That affect is particularly acute for large, ground-mounted projects where the price of solar panels makes up a more significant portion of system costs.

In response, large Chinese PV makers with factories in Southeast Asia began converting a larger portion of their factories to produce bifacial products. However, that activity may slow if a claim by Roth Capital Partners proves true: that the Trump administration has decided to reverse the bifacial exemption.

In a research note issued yesterday, Roth analyst Philip Shen stated the private banking company’s investigations suggest the administration has decided to reverse the exemption for bifacial. At the time of going to press, the U.S. Trade Representative had not responded to the claim.

Manufacturing implications

Roth noted, whether or not the exemption goes will not matter too much for next year, as most of the volume under order to be shipped into the United States is based on standard monocrystalline silicon cells with passivated emitter and rear cell (PERC) technology. That claim is supported by pv magazine’s discussions with PV manufacturers who say they have been sold out for more than a year in advance, meaning contracts being filled for at least the next nine months were signed before the exemption.

The investment bank also stated a policy u-turn would not be good news for bifacial, although it could be argued the technology is likely to mature anyway given the advantages it offers.

However, there is one likely winner from any Trump change of direction: First Solar. Roth described the potential policy change as an “incremental positive” for the thin-film PV maker and its Series 6 technology, which competes against inexpensive Asian crystalline silicon solar for large PV projects.

Roth reiterated its “buy” advice on First Solar stock. It is important to note, though, First Solar is already in an enviable position. The company’s products are sold out years in advance as it continues to build and ramp more factories in Ohio and Vietnam.

The bigger picture

As for the larger U.S. market, removal of the bifacial tariff exemption could threaten projects with marginal economics. However, it is unlikely to be a big deal either way. Section 201 tariffs fell to 25% in February and will fall to 20% in four months time’, after which most orders being made now will be filled.

The tariff – and the uncertainty created by the Section 201 process – definitely hit the U.S. market last year. However the market is back on a growth path this year, with Wood Mackenzie reporting a record 8.7 GWdc of large scale solar under construction at the end of July.

Wood Mackenzie estimates the United States will install 12.6 GWdc of solar this year, and with total U.S. module manufacturing capacity at less than half of that, it is clear module imports will continue, Section 201 or no – and tariff exemptions or no.

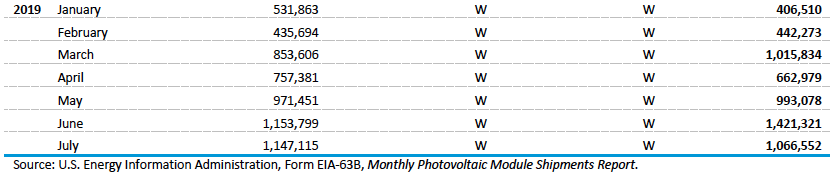

That guess is supported by module shipment data published by the U.S. Department of Energy. The agency’s latest report found more than 1 GW of module imports in both June and July, with imports making up the bulk of shipments.

Please login to comment

[…] revival and their U.S. counterparts have been only partially revived thanks to President Trump’s protectionism. India has thus far failed to live up to its promise of becoming a solar manufacturing superpower […]

[…] has once again been demonstrated by the escalating crisis in the Gulf since U.S. president Donald Trump ordered the drone attack in the early hours of Friday which killed top Iranian general Qassem […]

[…] Roth: Trump administration could end bifacial tariff exemption […]