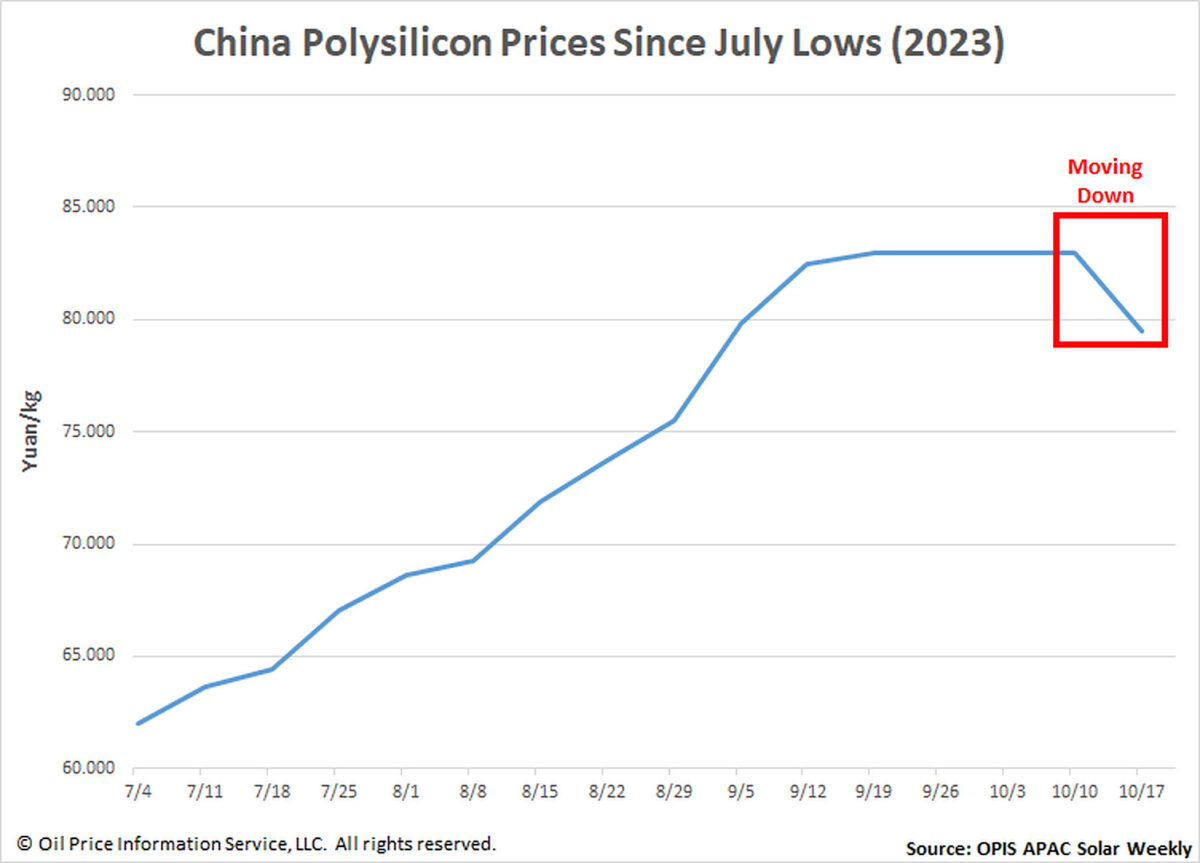

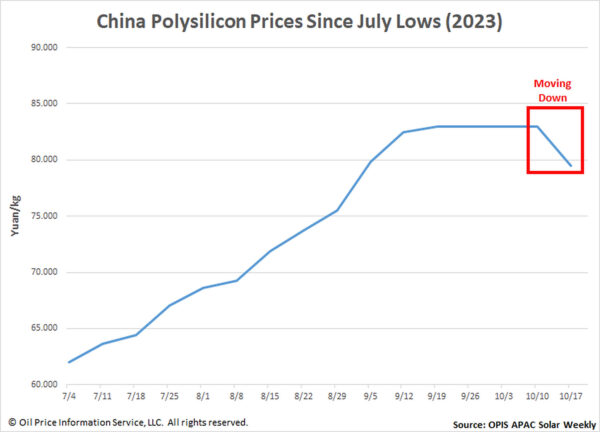

China Mono Grade, the OPIS benchmark assessment for polysilicon prices in the country, fell 4.22% to CNY79.5 ($11.07)/kg week-on-week for the first time in more than three months on the back of weakening demand across the solar supply chain, which has finally impacted the upstream polysilicon sector.

Domestic polysilicon prices were assessed in the range of CNY75-83/kg. While major polysilicon makers hold their price quotes at the higher end of the range, tier-2 producers have cut prices to their lower end, pulling overall market prices down.

Weakening polysilicon demand – driven by lower solar installation rates in the fourth quarter of 2023 – contributes to the move downward, with trade volumes light in the week to Tuesday. Wafer makers have cut their operating rates as module inventories build and solar installations face delays in the fourth quarter. Expecting polysilicon prices to fall further, wafer makers adopting a wait-and-see approach when purchasing the material.

High inventories in both the polysilicon and wafer segments also weigh on prices. According to a solar market veteran, China’s wafer inventories are estimated at 20 GW and polysilicon inventories at around 50,000 MT.

China polysilicon prices are expected to bottom out in the fourth quarter as more polysilicon capacity comes online and building inventories contribute to a supply glut.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.