Wind up, solar down for Europe in early 2024

PV, solar thermoelectric and wind energy production

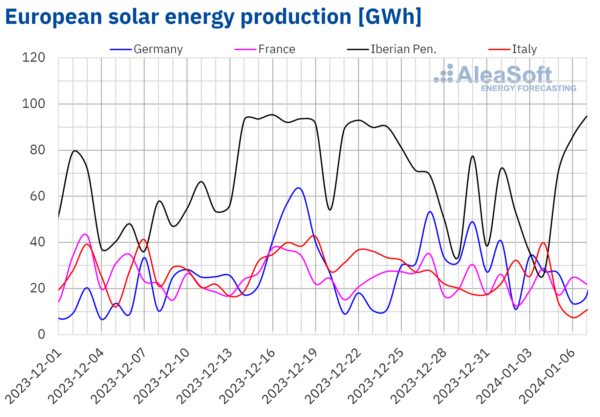

In the week of Jan. 1, solar energy production decreased in most major European electricity markets compared to the previous week. The German market registered the largest drop of 33% while the Italian market registered the smallest drop of 7.7%. The Iberian Peninsula was the exception as solar energy production increased by 4.0% mainly due to a 22% increase in the Portuguese market. On Jan. 7, the Spanish market generated 80 GWh with solar energy, marking the highest production using this technology since the end of November last year.

According to AleaSoft Energy Forecasting’s production forecasts, solar energy will increase in Germany, Italy and Spain in the week of January 8.

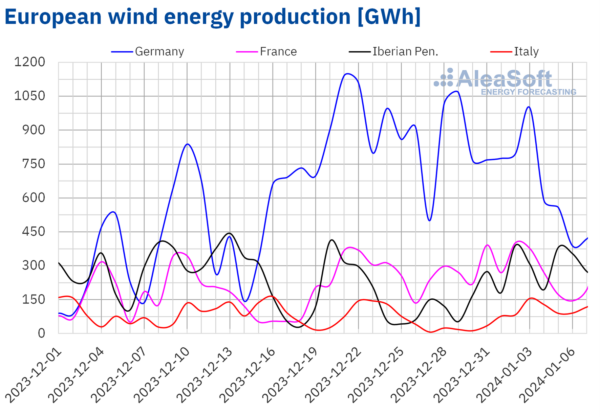

As for wind energy production, in the first week of 2024, it registered increases in most major European electricity markets compared to the previous week. Italy led the increases with 246%. The Spanish market also registered a significant increase of 157%. The French market had the smallest increase of 1.1%. Despite this, on Jan. 2, France generated 402 GWh with wind energy – the highest daily value in the historical series. Although the German market was the leader in wind energy production among the analyzed markets during the week, it registered a 23% decrease compared to the production of the last week of 2023.

According to AleaSoft Energy Forecasting’s wind energy production forecasts, production with this technology will drop in all analyzed markets in the week of Jan. 8.

Electricity demand

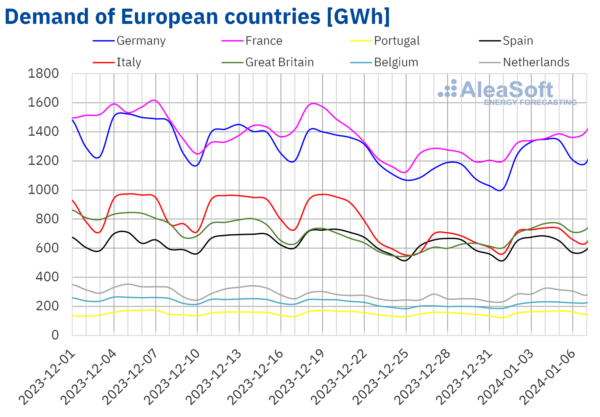

Major European electricity markets registered an increase in electricity demand during the week of Jan. 1 compared to the previous week. It was anticipated that demand would recover after Christmas celebrations the previous weeks. Among all analyzed markets, the British market registered the largest increase, reaching 20%. The Spanish market registered the smallest increase, 1.8%.

In the first week of 2024, most analyzed markets registered decreases in average temperatures. These decreases also favored an increase in demand. Decreases ranged from 1.3 C in France to 2.6 C in Germany. In contrast, in Southern European countries, average temperatures were less cold. Increases ranged from 0.3 C in Italy to 2.2 C in Spain.

According to AleaSoft Energy Forecasting’s demand forecasts, the trend will continue and electricity demand will increase in all analyzed markets in the week of Jan. 8.

European electricity markets

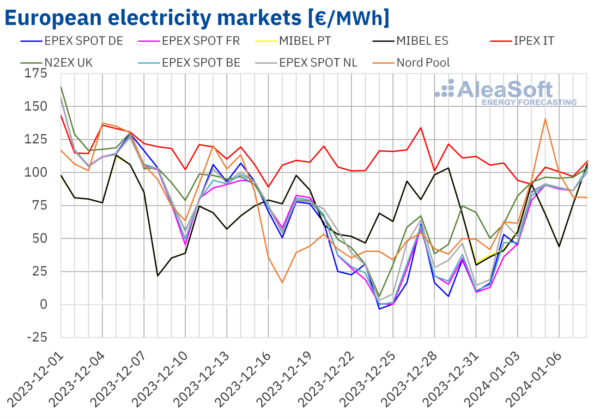

In the week of Jan. 1, prices in most major European electricity markets increased compared to the previous week. The exceptions were the IPEX market of Italy, with a 14% decrease, and the MIBEL market of Spain and Portugal, with a 23% drop. On the other hand, the EPEX SPOT market of Germany registered the largest percentage price rise, which was 222%. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices rose between 49% in the N2EX market of the United Kingdom and 163% in the EPEX SPOT market of France.

In the first week of January, weekly averages were below €85/MWh in almost all analyzed European electricity markets. The exception was the Italian market, which reached the highest average, €100.01/MWh. In the rest of the analyzed markets, prices ranged from €58.88/MWh in the Spanish market to €83.13/MWh in the Nord Pool market of the Nordic countries.

As for hourly prices, the German, Belgian, French and Dutch markets registered negative hourly prices on Jan. 1 and 3. On Jan. 1, the British market also registered negative prices. However, these negative prices were not as low as those reached in these markets during the previous week. On the other hand, on Friday, Jan. 5, from 16:00 to 17:00, the Nordic market price was €254.58/MWh. This was the highest hourly price since December 2022. The MIBEL market registered the lowest daily prices between January 5 and 7, which helped it to have the lowest weekly average compared to the rest of the main European markets.

During the week of Jan. 1, the general increase in electricity demand led to higher prices in European electricity markets. The fall in solar energy production in countries such as Germany and France and the decline in German wind energy production also contributed to the price increases. However, the significant rise in wind energy production in Italy and the Iberian Peninsula favored lower prices in these markets.

AleaSoft Energy Forecasting’s price forecasts indicate that in the second week of January, prices might continue to rise in European electricity markets. The recovery in demand and the general decline in wind energy production might contribute to this behavior.

Brent, fuels and CO2

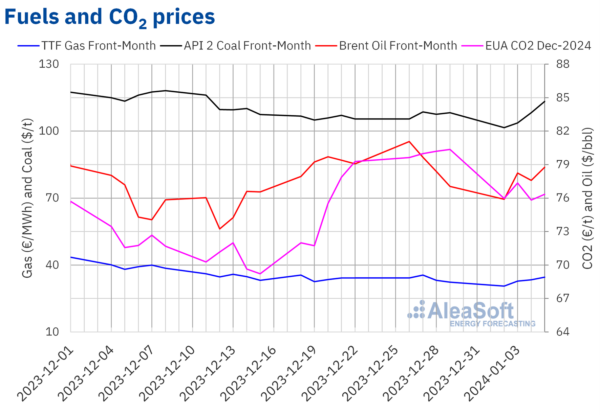

On Tuesday, Jan. 2, Brent oil futures for Front‑Month in the ICE market registered their weekly minimum settlement price, $75.89/bbl. The rest of the week, prices were above $77.50/bbl. On Friday, Jan. 5, these futures reached their weekly maximum settlement price, $78.76/bbl.

In the first week of January, instability in the Middle East exerted its upward influence on Brent oil futures prices. Production disruptions in Libya also contributed to the price increase. However, the announcement of price cuts by Saudi Arabia might exert a downward influence in the second week of January.

As for TTF gas futures in the ICE market for the Front‑Month, on Tuesday, January 2, they continued with the declines of the last sessions of the previous week. On that day they reached the weekly minimum settlement price, €30.57/MWh. According to data analyzed by AleaSoft Energy Forecasting, this price was the lowest since the first half of August 2023. As of Wednesday, Jan. 3, prices started to increase. As a result, on Friday, Jan. 5, TTF gas futures reached their weekly maximum settlement price, €34.55/MWh. This price was 6.8% higher than the previous Friday.

In the first week of January, the forecast of a cold snap in Europe had an upward influence on TTF gas futures prices. However, at the beginning of the second week of January, forecasts of milder temperatures, abundant supply and still high levels of European stocks might exert a downward influence on the prices of these futures.

As for CO2 emission rights futures in the EEX market for the reference contract of December 2024, during the first week of January, settlement prices were lower than those of the previous week. On Wednesday, Jan. 3, these futures reached their weekly maximum settlement price, €77.35/t. In the following session, they fell by 2.0% to €75.82/t. This was the minimum settlement price for the first week of January.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment