Competition heats up

Oversupply is hitting some solar manufacturers hard but grid constraints and labor shortages are unlikely to hold the solar industry back in 2024.

Weekend Read: Connecting HJT

The application of busbarless cell interconnection approaches could unlock the potential of heterojunction (HJT) technology, primarily by reducing the historically high silver usage of negatively-doped, “n-type” cell technology. As HJT manufacturing increases, a wave of applications may very well be on the horizon.

A survival guide for solar SMEs

As solar manufacturing moves toward technological convergence, and rampant production capacity expansion continues, standing out from the crowd is just one of the strategies small- and medium-sized enterprises (SMEs) will have to use to survive, according to InfoLink’s Amy Fang.

Weekend Read: As simple as IBC

The search for ever higher conversion efficiency has driven solar researchers to focus on back-contact cell approaches, and efforts to devise more cost-effective manufacturing are bringing technologies such as interdigitated back contact (IBC) solar into the mainstream, as Mark Hutchins reports.

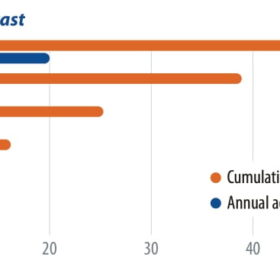

A 200 GW solar year in 2022

Structural imbalances in the supply chain and the energy intensity and consumption controls that China imposed in late September have caused prices for most PV module materials and components to continue to rise. Shipping fees and PV plant construction costs also remain high. PV plants in many regions will therefore be postponed until next year, but it remains unclear when module prices will start to fall. Despite these challenges, the global race to cut carbon emissions continues, and InfoLink’s Corrine Lin forecasts a bright future for PV deployments in 2022.

Post-SNEC storage

China’s battery manufacturing industry is growing robustly in line with the rapid expansion of the electric vehicle market. The stationary storage sector currently lags behind developments in leading markets such as the United States and Europe, but strong growth is expected between now and 2030, driven by supportive policies. Fang-Wei Yuan, a senior analyst at InfoLink, examines the latest developments in China’s energy storage industry and looks at the announcements and product launches made at the Shanghai SNEC exhibition back in June.

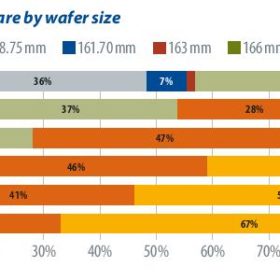

N-type market growth

Several manufacturers recently brought average mono PERC cell efficiency to 22.5%, and efficiencies will likely go beyond 22.6% in the second half of this year. This suggests that p-PERC cell efficiency could be brought closer to that of n-type, making it more difficult for n-type cells to compete in the increasingly challenging market. Taking costs and market conditions into account, most manufacturers have slowed their capacity expansion plans, leading to a gap between actual output and production capacity. PV InfoLink’s Wells Wang sheds some light on n-type trends in 2020.