Lazard, Lazard, LCOE – what’s the cheapest energy?

From pv magazine USA

The headline information making the rounds with this analysis is that building new wind and solar power, in some cases, is cheaper than running already built fossil and nuclear facilities. Well, we already knew that at pv magazine.

For instance, Indiana finalized their plans to shut down coal plants and exchange them renewable facilities because its “the most viable option for customers”. Colorado recently voted for retiring Xcel’s coal-fired Comanche Generating Station ten years early, which represents 660 MW of total capacity for two separate units at the site – again, for economic reasons. Carbontracker.org noted that all of the wind bids for the above Xcel RFP were cheaper than coal, and 74% of the solar bids were.

Yesterday, Lazard released its Levelized Cost of Energy (LCOE) analysis version 12.0 for Energy (.pdf), and Version 4.0 for Energy Storage (.pdf). The document shows that utility scale wind, solar offer the cheapest absolute electricity pricing – without subsidies. When federal tax subsidies are applied, essentially politically palatable forms of a carbon tax, we see all thin film solar cheaper than all gas, and the majority of crystalline silicon solar cheaper than gas.

Rooftop solar for residential and commercial, with its broad price ranges representing the broad classes of projects they cover, shows higher pricing. However, this analysis doesn’t consider the additional benefits including avoided costs achieved with behind-the-meter installations, and as such it isn’t a pure apples-to-apples comparison.

Nonetheless, even with this calculations handicap – unsubsidized rooftop commercial and industrial solar power is quite comparable to almost all new coal construction, cheaper than most nuclear, and even touches on the upper costs of combined gas. When considering federal, and state incentives where available, we start to see why rooftop corporate procurement was a growing solar sector in a mostly flat first half of 2018.

The document does make reference to emissions once – in the slide Cost of Carbon Abatement Comparison. The costs considered in the document were not pollution, health or social costs – but instead carbon avoidance costs. The document defined these values as ‘$26 – $34/Ton vs. Coal and $10 – $25/Ton vs. Gas Combined Cycle’. Lazard hypothesized, that if policy makers were to apply these market values to utility scale wind or solar, they would be great drivers toward renewable deployments.

The document notes a much lower price per kilowatt-hour (kWh), after applying carbon avoidance costs, of wind between 6.3-15.1¢/kWh lower vs gas and coal, respectively, and 2.5-11.7¢/kWh lower for solar vs gas and coal, respectively. These numbers are for unsubsidized wind and solar.

The analysis above assumes 60% debt at 8% interest rate and 40% equity at 12% cost. The document does describe its fundamental values that fed its calculations on the page, “Levelized Cost of Energy Comparison—Sensitivity to Cost of Capital“.

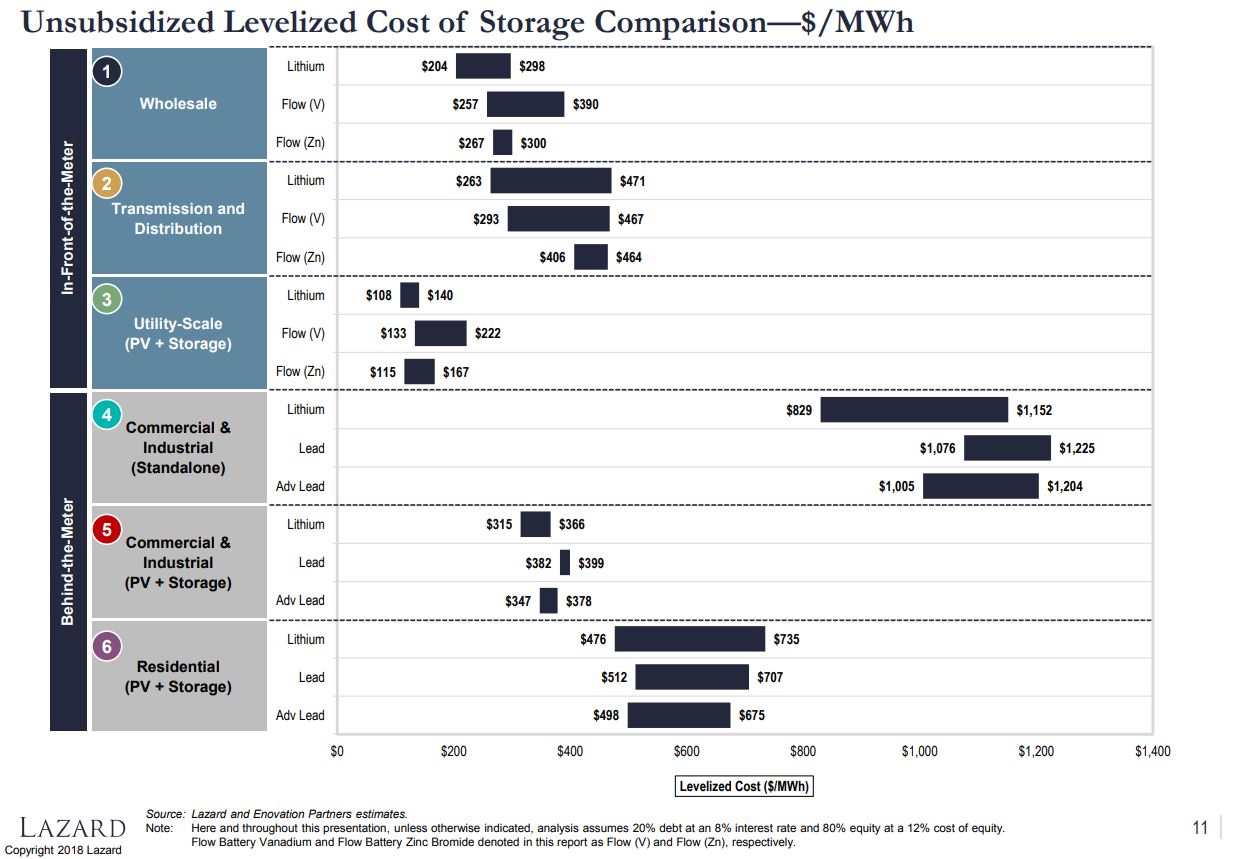

The Levelized Cost of Energy Storage 4.0 (.pdf) version gave significant information about how it came to its current form, and the assumptions that it used in determining the valuation. Additionally, significant time was spent differentiating across the various utility regions in the United States, as each of them have many nuances driving energy storage revenue.

The point that first jumped out from the above unsubsidized analysis was that, over the long term, flow and lithium ion pricing is much closer than headlines showing off projects being deployed are. This probably has much to do with lithium ion product availability due to intertwining nature with electric vehicles. This ought give us insight into a brewing competition that will benefit the industry, and might provide us with complementary technologies offering contrasting benefits – much like wind and solar.

All of these costs come from a history that Lazard also shows. One thing to note is that utility scale solar power is catching up with the ultra low pricing of wind power. Over the last decade the three cost leading energy sources – wind, solar and combined cycle gas – saw price decreases of 69%, 88% and 30%, respectively.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment

“The analysis above assumes 60% debt at 8% interest rate and 40% equity at 12% cost. ” These numbers are wholly unrealistic for the USA and other OECD countries. Lazards only keep them because that’s how they started 12 years ago, and it allows for solid comparisons over time. But today, utility wind and solar farms are pretty low-risk projects routinely organized by big and experienced developers. Once built, and PPAs put in place, most of the risk is sunk and they become *very* low-risk long-term investments for the likes of insurance companies and pension funds. Warren Buffett’s Berkshire Hathaway can borrow for 30 years at around 4%. and other big firms in this space won’t pay that much more. Once you correct to a realistic cost of capital, the lead of wind and solar over coal and gas becomes much larger. Their capital costs are lower too, but the fuel costs are not reduced.