Room for US residential solar to reach 41 GW by 2025

From pv magazine USA

When most Americans think of the energy transition, they often picture of the iconic image of solar panels on the roof of a single family home. However, rooftop solar on homes and businesses actually makes up a relatively small portion of the overall electricity generated by renewables.

This portion is very different from state to state. According to EIA data, Hawaii is the leader with plants smaller than 1 MW providing about 7.5% of the island chain’s total electricity in 2017, but these smaller solar arrays also provided about 4% of California’s power.

A new analysis by Credit Suisse indicates that there is still a lot of room for residential solar to grow in both states. The investment bank and financial services company notes that only around 3% of rooftops in the United Staes hosted residential solar last year.

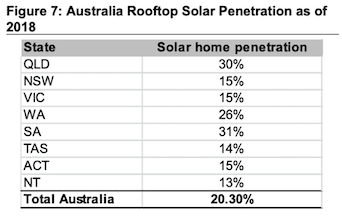

A new analysis by Credit Suisse indicates that there is still a lot of room for residential solar to grow in both states. The investment bank and financial services company notes that only around 3% of rooftops in the United Staes hosted residential solar last year.

The bank compares this to more than 30% in some Australian states. It also notes that levels are higher in Hawaii and California. While there is some uncertainty in the data around which rooftops are being included, trade groups who pv magazine consulted with estimate only 14% of single-family homes have solar in Hawaii and 6% in California – meaning that in these states there is still ample potential.

As such, Credit Suisse has forecast that residential rooftop solar penetration will grow to 5% by 2020 and 11% by 2025, with installations growing more than 3x from current levels to reach 41 GW by that year.

How much potential?

The U.S. Department of Energy’s National Renewable Energy Laboratories (NREL) has done some work on total rooftop solar potential, and in a 2016 report found that even the roofs of small buildings (5,000 square feet or less) have the technical potential to host 731 GW of solar, enough to meet 25% of the nation’s electricity demand.

Incidentally, if you add larger buildings this gets you to 39%, and this number is greater in some states than others, with California, Maine and Vermont showing the highest levels of technical potential at 60% of electricity demand or higher.

It is also worth noting that these estimates doe not include carport systems or building integrated photovoltaic facades, both of which could significantly boost this potential if included.

A bumpy road ahead

Despite the smooth line of Credit Suisse’s forecast, in recent years the U.S. residential market has seen significant hiccups. 2017 saw the first year in at least a decade where this market actually declined from the previous year due to a variety of factors including the pull-back of Tesla and Vivint from business and sales models emphasizing aggressive growth.

Credit Suisse’s forecast also does not mention policy, and here is where the rubber meets the road. With very few exceptions U.S. utilities have fought customer-owned and sited PV tooth and nail, both by trying to dismantle net metering policies and by changing rates to claw back more revenue from their customers who go solar, weakening the economics of installing PV in the process.

However, if regulators value the benefits of distributed solar and energy storage, including deferred spending on transmission and distribution infrastructure as well as the potential for a more stable electricity supply – particularly during disasters – then we can expect to see continued growth as costs decline.

And the black swan in all of this is the potential for mandates for rooftop solar on new buildings, as are being implemented in California for low-rise residential buildings and in a mid-sized Massachusetts town for commercial buildings.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment

[…] room for far more growth. A 2018 Credit Suisse analysis predicts that residential solar could grow more than three times by 2025. Plenty of space exists on rooftops. Even in California, perhaps only 6% of homes have solar […]

[…] room for far more growth. A 2018 Credit Suisse analysis predicts that residential solar could grow more than three times by 2025. Plenty of space exists on rooftops. Even in California, perhaps only 6% of homes have solar […]

[…] recent analysisfrom multinational investment banking giant Credit Suisse puts 2017 rooftop solar penetration at […]

[…] recent analysisfrom multinational investment banking giant Credit Suisse puts 2017 rooftop solar penetration at […]

[…] to a report by Cape Analytics. But interest as a whole is growing with solar power expected to grow three times by 2025 and potentially provide up to 39% of the nations […]