The last decade in PV has been marked by a pronounced and in some ways defining feature: dramatic reductions in module prices. While it has delivered much pain for manufacturers and other companies across the module supply chain, it has also underpinned the record setting project prices and the highly competitive position solar enjoys today. But where are prices likely to head in the next 12-24 months?

On prices

One thing is absolutely clear, according to the analysts: There are no indications that prices will increase at any point soon. On the other hand, more stable international demand and increased maturity across the industry and supply chain will deliver more certainty and stability in terms of pricing, despite the continuing trend of ever-cheaper modules.

“Module buyers, including end-users, governments, and utilities or a combination thereof, expect price decreases and have other electricity options; the acceptance of a price increase is low,” says analyst Paula Mints. She notes that these expectations drive downward price pressures, leaving suppliers with limited control over price.

Edurne Zoco sees prices remaining relatively flat through to the first quarter of 2020, with “moderate” decreases after that. One thing feeding into more stable module pricing in the next 24 months is the increased prevalence and adoption of higher efficiency, or “advanced” modules, with mono PERC and n-type technology forecast by Zoco to increase market share.

“We [IHS Markit] anticipate a much slower price decline trend than we have seen in the last years,” says Zoco. “The industry is becoming more mature and consolidated, volatility is being reduced, and the margins across the supply chain are tight.”

Analyst Corrine Lin also points to tight margins, as there is “barely any profit now” across the multicrystalline supply chain in particular. This will be a constraining factor on price declines through 2020. However, she notes that weak demand in the first half of 2020 is likely to force multicrystalline cell and module makers to make some reductions. On the mono side, Lin reports that the wafer and cell segment is currently the most profitable for manufacturers, and is therefore the most likely sector to see price reductions “in the low seasons” across the next two years.

Jenny Chase says that her take on prices may be seen as “disappointing” in that she expects “not a lot of change” in the next two years. The BloombergNEF benchmark, as reported by Chase, sees prices declining from $0.23/W in 2020, $0.20/W in 2022 and $0.17/W in 2025.

“It just isn’t that easy to shave off costs when they are already so low, and a big gain from a rapid shift to diamond wire saws from slurry-based wafer slicing is now complete,” says Chase.

While there may not be dramatic declines, Chase notes that with mono and bifacial technology becoming more commonplace, developers and installers will “get more bang for your buck” in terms of power output, leading to a continual decline in system costs – and solar’s LCOE.

On future cost reductions

Falling polysilicon prices are shaping up as a major cost reduction driver in the short to mid-term, report the analysts. Zoco points to new polysilicon capacities coming online in China as likely resulting in falling costs. “They have the potential to reach similar levels of polysilicon quality with a lower cost structure,” says Zoco.

Lin says that polysilicon costs will particularly fall in the multicrystalline segment, as cell producers continue to switch from multi to mono. PVInfoLink tips polysilicon prices for multicrystalline wafer production to fall to RMB 55-57 ($7.8-$8.1)/kg in the low season over the next two years. Polysilicon prices for mono, Lin suggests, will remain flat, with new Chinese capacity supplying the market while non-Chinese polysilicon manufacturers exit, resulting in supply-demand equilibrium.

Lin also expects the continuing trend of localized production equipment and materials supply in China to deliver cost reductions – with increased throughput delivering savings. Boosting power output, however, will be key and she cites an increasing emphasis on R&D in recent years as indicative of its importance.

Chase also emphasizes higher performance, with the continuing switch from aluminum back surface (Al-BSF) to PERC cell architecture, along with thinner and larger wafers, and busbar configuration optimization as being cost-decline drivers. “The wonderful thing about the experience curve is that lots of little bits add up,” says Chase.

While the benefit of scale has been a defining feature of the solar production landscape this decade, there are limits to its continued cost benefits, caution the analysts. For many tier-one producers, 5 GW or even 10 GW is now standard.

“Simply being bigger does not always mean cheaper – it will not protect you if you are running at half capacity,” cautions Mints. “A 10 GW facility with 5 GW of demand is pretty darned expensive.”

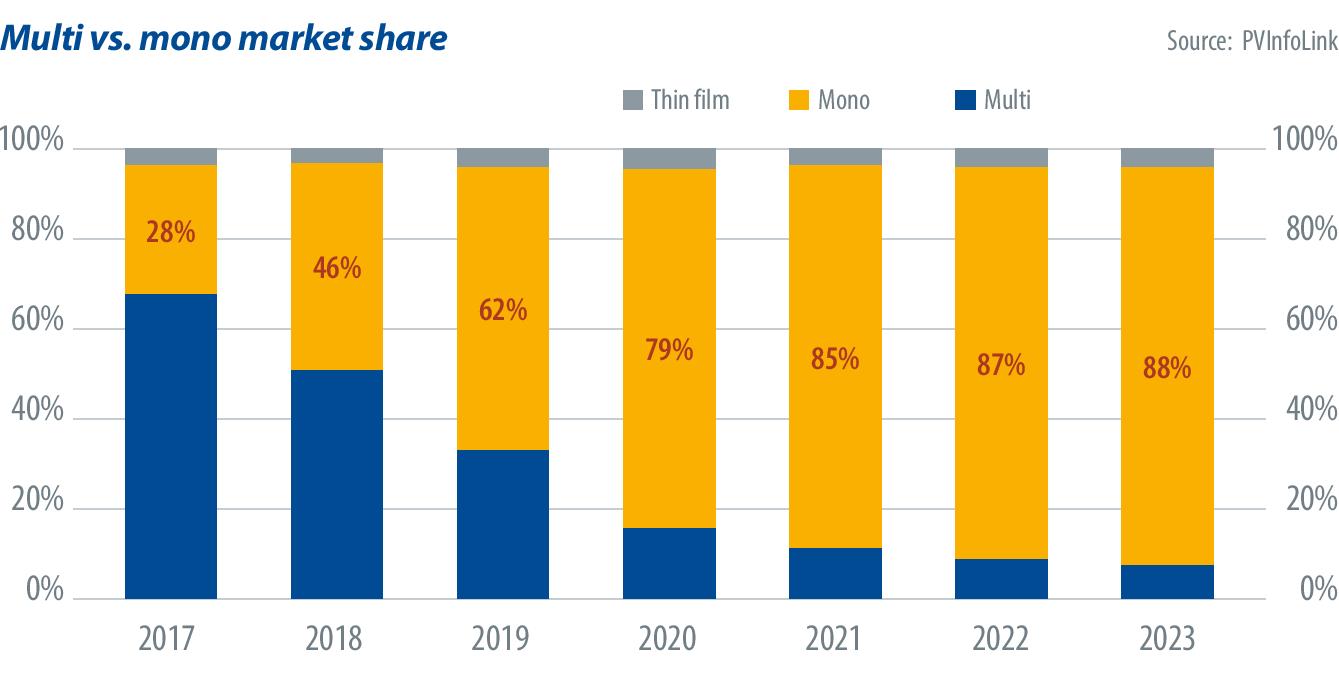

On multi vs. mono

The future is mono, report our analysts – and although this is not new to market observers, there are some caveats. They note that 2019 marked a watershed year for this development, with mono surpassing multi in terms of market share. Throughout the year, mono’s market share is tipped to reach between 60% and 62% according to their forecasts, up from the low- to mid-40s in 2018.

Higher power output at roughly equivalent costs is behind mono’s rise to dominance. But for manufacturers to make the switch to mono, it “takes considerable effort and does not happen instantly,” says Chase.

There are some challenges remaining for p-type monocrystalline PERC cells and modules, adds Mints, primarily in overcoming light induced degradation (LID) issues. Because of this, multicrystalline BSF “has not gone away.”

Zoco suggests that multi-PERC plus black silicon is a potential pathway for competitiveness. However, its production costs would have to decline, which presents a significant mountain to climb in the short term.

On high efficiency cells

The technology to enable higher efficiency solar cells is a perennial discussion topic, and aluminum oxide PERC, tunnel oxide passivated contact (TOPCon) or heterojunction (HJT) are the current candidates in the near term. But it is somewhat difficult to pick winners, and the analysts were somewhat cautious in their responses.

“N-type+TOPCon and HJT are at the same stage,” says Zoco. “The next technology should combine a significant efficiency improvement with respect to PERC mono technology, which at the same time is able to maintain a reasonable price gap.”

Lin believes that HJT “will be the next step for high efficiency cell production”, but she says that it probably won’t take market share away from standard PERC in the next two years.

“While HJT requires less processing and generates higher efficiencies, the cost is much higher than that of PERC. Moreover, it’s difficult for HJT to accommodate larger wafers as well as half-cut and shingled modules,” says Lin. “With similar power output but significantly higher costs, the market share of HJT will remain at 4-6%. TOPCon is also facing the challenge of costs, similar to HJT.”

Mints advises caution in terms of HJT, noting that there are other technological pathways for n-type, and that higher material costs will continue to remain a challenge for all n-type technologies. But Chase is also not convinced, at this stage, that HJT is an inevitability.

“I’m unfortunately old enough to remember the last time heterojunction was a buzzword in solar,” explains Chase. “This was largely due to failing thin film silicon manufacturers, most of which had bought production lines from Oerlikon or Applied Materials, trying to find a way they could upgrade them to make a saleable product. It didn’t work.” She points to a 40 MW utility scale project in India, in which the HJT modules that were deployed required replacement. “My understanding is that thin film silicon – either amorphous or microcrystalline – is a difficult material to produce in bulk with consistent properties,” says Chase. “Heterojunctions using thin film silicon will need to solve this problem better than the last lot.” Perovskites, Chase continues, are another potential multijunction pathway, but they “seem to be a lab tech being rushed to market. I have seen this before and it ended badly.”

On the manufacturing landscape

The PV manufacturing sector has seen a pronounced period of consolidation in recent years, but the narrative of ever continuing and linear consolidation may be overstated. “If you are an analyst you can basically always predict consolidation, then point at some bankruptcies and acquisitions later on and say you were right,” Chase candidly admits. “I don’t see strong consolidation among the long tail of manufacturers, though there has been some.”

Mints agrees that it’s easy to predict consolidation, but she points to macro-economic factors as likely being important.

“If demand in China accelerates, and as its economy slows, its government needs to stimulate demand and work, and it will, then there will be no need to consolidate inside of China and in Asia. Manufacturers in other countries may not be so lucky,” says Mints.

Looking to the future, it is also far from certain that the manufacturing landscape will feature an ever-decreasing number of producers. “Judging from the market situation now, it’s not necessary for manufactures to consolidate,” says Lin.

“In fact, top-tier vertically integrated companies have arranged their supply chain in a more balanced manner, so there won’t be much consolidation in the future, but we expect to see more cooperation and collaboration among the manufacturing giants, such as the partnerships between Longi and Tongwei or GCL and Zhonghuan.”

“We do not anticipate an acceleration of consolidation,” says Zoco. “The supply chain is much more mature than years ago. Manufacturers are better prepared to changes in the markets and understanding better the risks related to contracts such as government regulations.”

On 2019

When considering what 2019 means for the PV industry, the analysts say there are a number of notable features likely to stand out. In terms of technology, while there has been much discussion of high efficiency cells, Lin sees module-level innovations as having had the most pronounced impact. She points to the jump of 10-15 W in module power output increases, from the 5 W per annum achieved in previous years, as being most significant. She says it was enabled primarily through larger wafer sizes, and maturing half cut and shingled cells.

Along with mono’s watershed moment, bifacial technology’s rise is also of note, says Zoco. In particular, the bifacial module exemption under U.S. Section 201 tariffs is driving acceptance in this market and beyond. Mints, meanwhile, agrees that tariffs and trade disputes will be seen as a defining feature of 2019.

For Chase, it is end-market developments that will rise to the fore. Vietnam’s growth to a 4.5 GW market, when the target was only 850 MW, will be of note, as will U.S. utilities’ adoption of solar+storage – so installations act as if they were a gas peaker. “2019 could be the year where U.S. utilities seriously decided they couldn’t be bothered with managing solar and would just sign PPAs for solar+storage,” Chase suggests.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.