Growth in residential energy storage systems (ESSs) is driven by customers installing energy storage alongside rooftop solar amid some of the highest global electricity prices, expiring feed-in tariffs (FITs), subsidies, and concerns over resilience.

By adding energy storage, customers can maximize the amount of solar that they self-consume (rather than export to the grid) as well as enjoy off-grid power when power from the grid is cut off. Being cut off from the grid is increasingly becoming a concern from remote communities or homes with the frequency and severity of bushfires increasing.

An estimated 15% of Australian households have had rooftop solar systems installed by 2020. New solar installations paired with an ESS is becoming the new standard, particularly as the Australian Energy Market Commission (AEMC) debates whether to impose charges on exported power from homes at particular times.

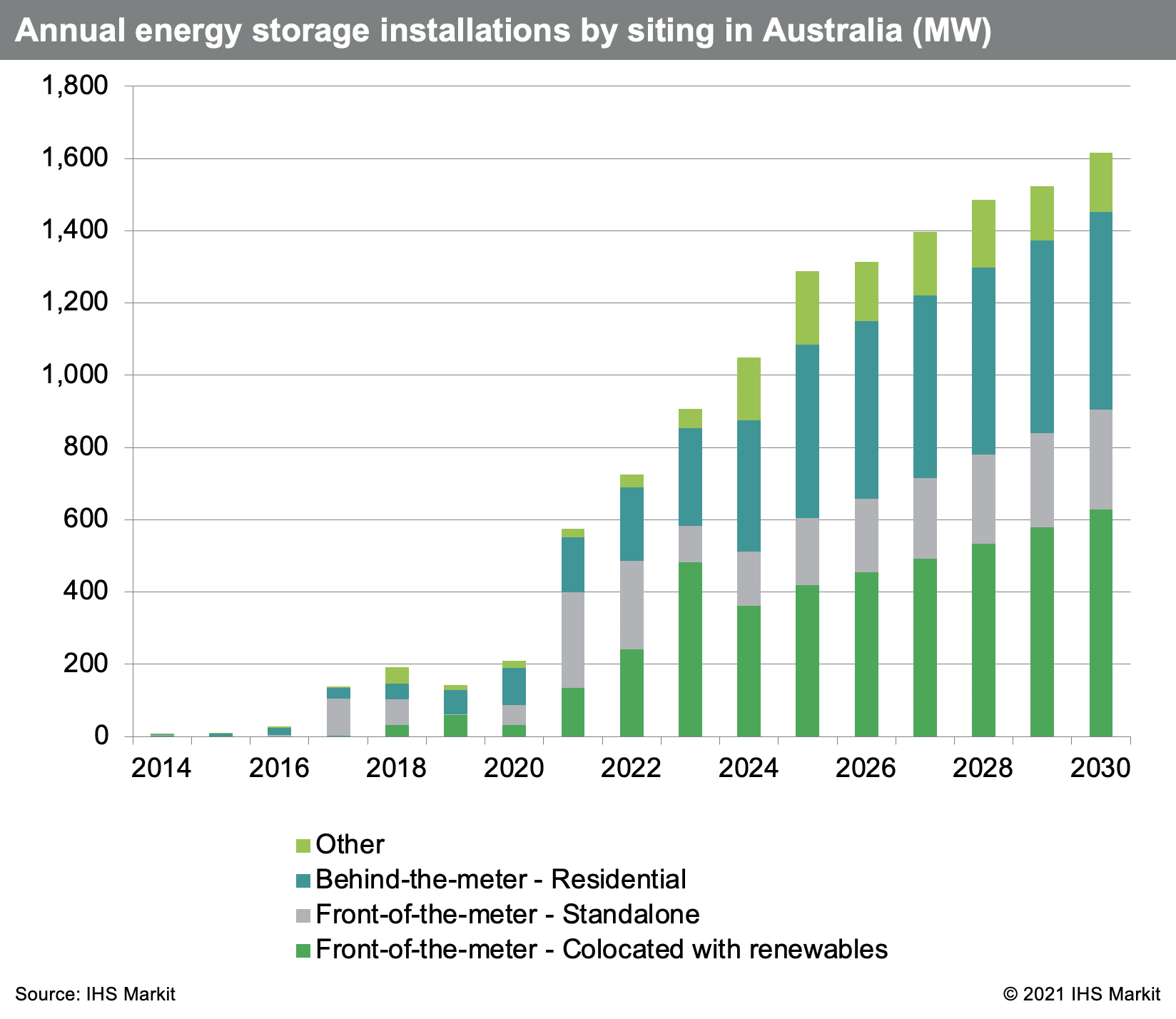

Large-scale FTM projects to account for 58% of installations in next 10 years

Front of the Meter (FTM) installations will be largely driven by projects colocated with solar. ESSs colocated with renewables will drive 55% of the FTM forecast between 2021 and 2030. The value of avoiding curtailment, which occurs when voltage levels fall too low – the plant trips due to sudden changes frequency levels or the network service provider needs to manage congestion on the network – increases the value of having dispatchable solar assets. These are being promoted by the Australian Energy Market Operator (AEMO). This is in part driven by the expected retirement of 7 GW of thermal capacity by 2030 and a further 6.2 GW by 2035.

However, operating hybrid projects under the AEMO’s standards is complex, which creates barriers to entry, and can delay project commissioning. Therefore, for many of the colocated projects the assets will be operated independently, meaning the assets may share a grid connection but otherwise have limited interaction.

Additionally, BESSs can capitalize on the volatility recorded in frequency control ancillary services (FCAS) or wholesale markets. Most battery energy storage systems (BESSs) in Australia will be utilizing merchant markets, primarily focused on the FCAS in addition to arbitraging prices in the wholesale market when prices spike.

On average, frequency services make up 85% of revenues for currently operational BESS, however a wide range of revenues are possible from the wholesale market, where average net returns from price wholesale arbitrage can be anywhere from AU$39/kW to $211/kW (US$27–245/kW) depending on the year, the state, average number of cycles, and duration of the system.

Increased demand during the summer months paired with generators tripping under hot conditions or as a result of bushfires or storms, often causes summer prices to spike as high as AU$14,500/MWh (US$9,974/MWh) in wholesale markets. For example, on January 31, 2020, when transmission lines in South Australia unexpectedly tripped when a tornado hit, FCAS prices spiked to over AU$1,000/MW (US$691/MW) multiple times throughout the day. This event alone created over AU$60 million (US$41 million) of revenue for all operational BESS in Australia.

One significant issue often overlooked is the challenge in securing financing for these large scale BESS. In fact, despite making up the majority of revenues for existing operational systems, FCAS revenues are often not considered bankable enough to be taken into account in the business case – meaning some other revenue stream must form the basis. This has meant that the majority of operational FTM BESS today have some form of government funding, usually from the Australian Renewable Energy Agency (ARENA), or are turning to fixed contracts for system security services to provide a fixed baseline revenue.

Other opportunities for energy storage in Australia

Another growing trend in Australia is the utilization of ESS to defer investments into network infrastructure. This is applicable to both FTM and BTM solutions. Where BTM standalone power systems (SAPS), typically solar PV plus a storage system, are replacing new lines to the fringe of the grid homes and farms (buildings or towns are often only connected by a single electricity line). Or FTM where large-scale ESS are aiding with congestion and mitigating outages on transmission lines. This is an issue that will only grow as the amount of renewables installed increases in a grid with such a dispersed population.

Overall, IHS Markit continues to see Australia as a key growth market for both BTM and FTM ESS driven by the fundamental need to support such a distributed electricity network that is rapidly transitioning away from thermal power to renewables. However, the market remains volatile as federal level policies still do not fully align with rapid transition that state governments are pushing for.

Additionally, the slow – relative to the speed of renewable installations – transition in market structure paired with the perceived risk in merchant markets creates challenges to develop bankable business cases for large scale BESS.

* The article was amended on June 1, 2021 to correct the figure 2.8 GW to 12.8 GW: “In its latest report, IHS Markit predicts that energy storage installations in Australia will grow from 500 MW to more than 12.8 GW by 2030.”

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

2 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.