Spending in the upstream sector may have to increase by 30% to meet the demands of a delayed energy transition, according to new analysis by Wood Mackenzie.

The research firm's latest report, “Taking the strain: how upstream could meet the demands of a delayed energy transition,” examines the extra resources and spending needed to meet prolonged high oil and gas demand.

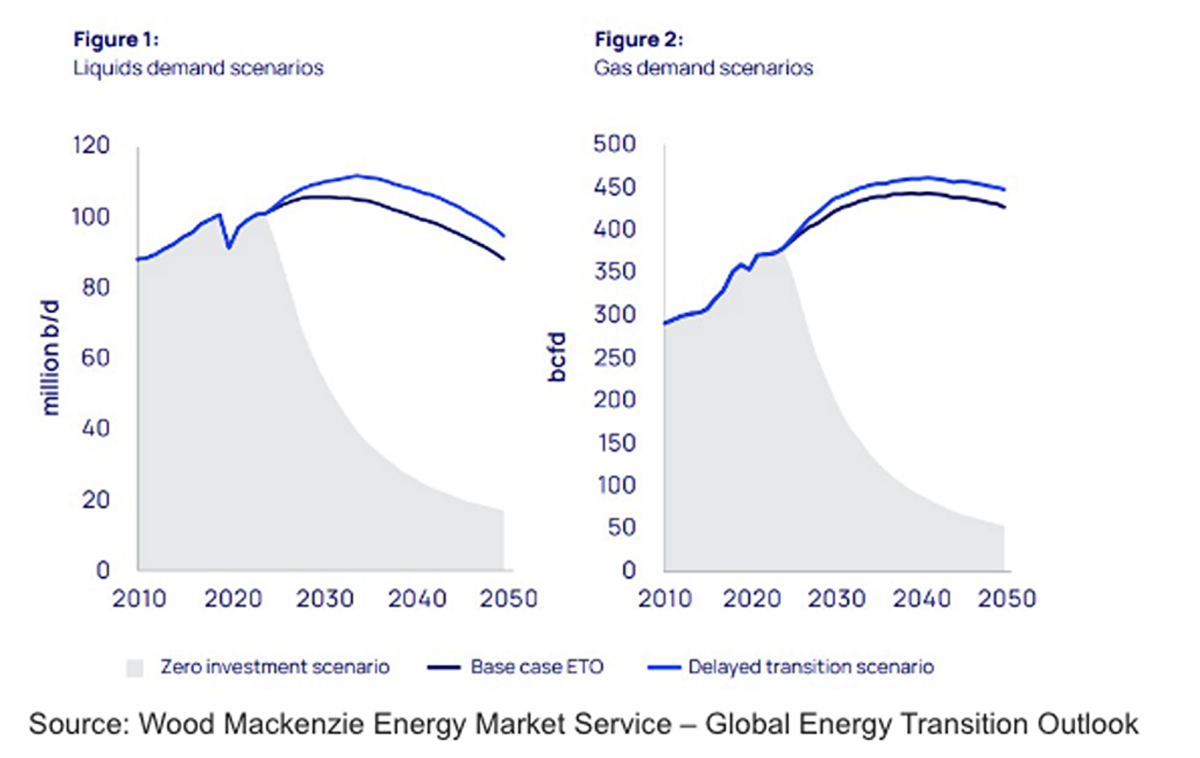

It said a delayed energy transition would increase global oil and gas supply needs by 5% and raise annual upstream capital investment by 30%. Liquids demand would average 6 million barrels per day (6%) higher than Wood Mackenzie’s base case through 2050, while gas demand would rise by 15 billion cubic feet per day (3%) over the same period, said the firm.

Angus Rodger, head of upstream analysis for Asia-Pacific and the Middle East at Wood Mackenzie, called stronger-for-longer demand growth a big challenge.

“A five-year transition delay would require incremental volumes equivalent to a new US Permian basin for oil and a Haynesville Shale or Australia for gas,” said Rodger.

Wood Mackenzie said the global oil and gas sector could meet this demand with existing resources and future exploration, but would need significant investment. The analysts estimate that a 30% increase in upstream spending would push annual development costs to $659 billion, up from $507 billion in the base case.

The company also warned that raising spending won’t be easy, despite signs of increased demand.

“More activity would put significant pressure on the supply chain – parts of which are already running near capacity – and project costs would inflate,” the report said.

Fraser McKay, head of upstream analysis at Wood Mackenzie, said corporate planning prices would rise if market outlooks improve, with greater confidence in demand longevity.

“In that environment, higher development unit costs and breakevens would likely be tolerable,” added McKay.

Wood Mackenzie also predicted that higher supply costs could drive up oil and gas prices. The company’s “Oil Supply Model” forecasts Brent prices rising above $100/barrel during the 2030s in a delayed transition scenario, then falling to around $90/barrel by 2050 – averaging about $20/barrel higher than the base case over the period.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.