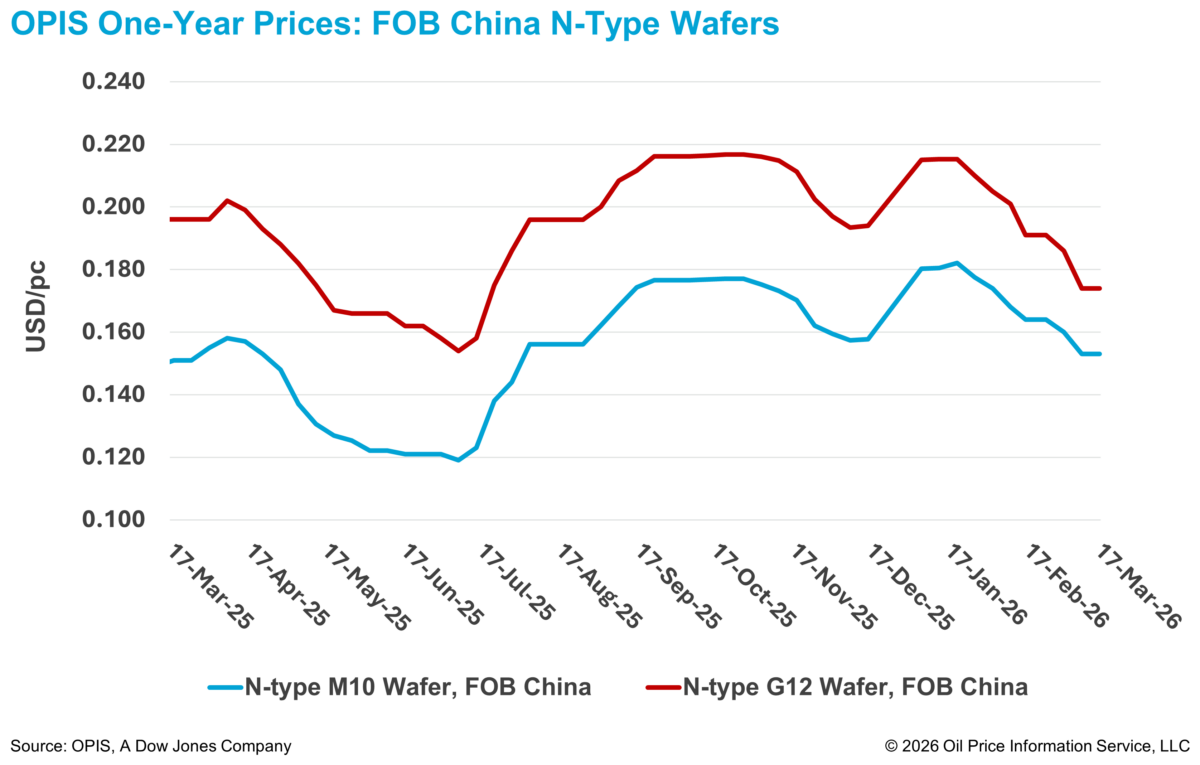

According to the OPIS Global Solar Markets Report released on March 17, Free-On-Board (FOB) China prices for n-type M10 and G12 wafers showed no week-to-week changes, holding steady at $0.153/pc and $0.174/pc, respectively.

Market participants indicated that the stability of wafer prices this week reflects weak demand and unresolved price negotiations between buyers and sellers, rather than signaling a stable overall market trend.

A wafer supplier noted that some cell customers had canceled orders in early March but have recently resumed purchases, driven by overseas orders and domestic end-user projects. However, while the pickup has helped reduce inventory, it has not supported upward price movement, the supplier added.

An industry source explained that at current market levels, wafer manufacturers often incur losses when purchasing polysilicon, processing it into wafers, and selling the products. As a result, manufacturers focus on fulfilling orders from key customers or accepting OEM contracts that avoid cash losses. Integrated manufacturers with polysilicon capacity are particularly favored, as they require wafer producers to convert their own polysilicon into wafers for downstream cell and module production.

Industry insiders also indicated that the current price of n-type 183 mm wafers in China, slightly above CNY 1 ($0.14)/pc, is unlikely to drop to 2025's mid-year historical low of CNY 0.80–0.90 ($0.116-0.131)/pc. A source said that after prolonged undervaluation, manufacturers have adjusted expectations and generally maintain a price floor near cash cost levels, excluding labor and operating expenses.

Meanwhile, in the global market, India's Ministry of New and Renewable Energy (MNRE) has amended the Approved List of Models and Manufacturers (ALMM) framework to extend mandatory domestic sourcing requirements to solar ingots and wafers from June 1, 2028, according to a March 17 office memorandum.

The latest amendment introduces a new List-III for ingots and wafers, extending the framework further upstream. From June 1, 2028, ALMM-listed modules used in covered projects will be required to incorporate cells listed under ALMM List-II and wafers listed under ALMM List-III. According to the amendment, the initial List-III will not be issued unless at least three independently owned manufacturing units are enlisted with a combined capacity of no less than 15 GW per annum. Manufacturers seeking wafer enlistment must also hold equivalent ingot capacity.

An integrated Indian manufacturer with ongoing investment into domestic upstream capacity has welcomed the move, describing it as a policy that rewards early commitment to backward integration. Even so, the manufacturer expects upstream expansion to remain more difficult than downstream buildout, citing higher capital requirements, longer lead times, and greater technical complexity.

To address some of these constraints, the government last week introduced a 60-day processing timeline for land-border-country investment proposals in specified manufacturing sectors, including polysilicon and ingot-wafer. In December 2025, it also streamlined visa procedures for foreign professionals needed for factory installation, commissioning, maintenance, and production.

While the effects of these policy efforts are yet to be seen, progress in upstream capacity development is emerging. Earlier this week, a major Indian solar manufacturer announced the groundbreaking of a 10 GW integrated ingot and wafer facility in Nagpur, Maharashtra.

Industry feedback indicates that, among ingot and wafer projects announced outside China over the past two years, this project stands out in terms of implementation feasibility. Market participants noted its development could have meaningful implications for global trade flows, including providing potential offtake channels for emerging non-China polysilicon capacity and alternative supply options for downstream manufacturers in regions such as Africa and the Middle East that are targeting exports to the U.S. market.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.