Will we finally buy European PV modules?

For two years, the European PV manufacturing story was straightforward, and grim. Chinese oversupply pushed module prices below €0.10 ($0.11)/W, European production lines halted one after another, and announced gigawatt-scale projects stalled at the financing stage. That story is shifting.

Firstly, the energy prices are rising again. The Iran conflict is one driver, but the underlying pattern is structural uncertainty in our globalized economy, the kind that makes governments and utilities rethink where their supply chains actually sit. Shipping costs remain volatile, adding another layer of unpredictability to the landed cost of imported modules. Secondly, and for the first time, Europe has regulatory infrastructure that goes beyond deployment targets: the Net-Zero Industry Act (NZIA), the Industrial Acceleration Act (IAA), national-level resilience and sustainability criteria, all aimed directly at creating conditions for domestic manufacturing.

The question is no longer whether Europe should reshore PV manufacturing. It is whether the industry can move before the window closes again.

A market that is splitting, not unifying

What the Net Zero Industry Act and the Industrial Acceleration Act actually create is not a single, uniform European market with a “Made in EU” premium. It is something more complex, and more consequential. The regulation gives Member States tools but leaves implementation largely to national authorities. The result is a European solar PV market that is becoming less homogeneous, not more.

In practice, three distinct market segments are emerging. The largest, roughly 60% of total EU demand, remains a free-for-all segment where price is the only differentiator, open to all suppliers regardless of origin. This is the commodity market, and Chinese manufacturers will continue to dominate it on cost. The remaining 40% or so falls under NZIA-type provisions, but splits further: a resilient supply segment, where manufacturers must demonstrate supply chain diversification and meet sustainability criteria; and a narrower “Made in EU” segment, where domestic production (at the moment, focusing on cells and inverters as per the proposed IAA) is explicitly required.

Each Member State is interpreting these segments differently. France’s AOS auctions have specific resilience weightings and scoring that differ from Italy’s FER X design. France has also introduced a reduced VAT for sustainable panels. Germany and Spain are developing their own approaches. The result: the addressable market for a European manufacturer is not “40% of EU demand.” It is a patchwork of national markets, each with different rules, timelines, volumes, and definitions of what qualifies.

For manufacturers, this means the commercial strategy for selling into France is genuinely different from the strategy for Italy or Spain. For developers, procurement just became significantly more complex. For policymakers, the competitive dynamics of your national auction design now matter more than they ever have.

This is not necessarily bad, it creates real, structured demand for domestic production. But it requires a level of market intelligence that simply did not exist when the only variable for PV components supply was price.

A vulnerability that deserves attention

There is a structural risk in the current framework that remains to be addressed. The European Commission’s current proposal allows manufacturers from countries with which the EU has free trade agreements to potentially qualify for the same preferential treatment that NZIA resilience criteria are designed to give European producers.

This is not yet settled. The text still needs to pass through Parliament and Council, and this specific provision will almost certainly be debated and likely modified during the legislative process.

But as things stand in the Commission’s proposal, the risk is real, and significant. If it holds in its current form, the “reserved” market segments designed to give European manufacturers a viable competitive space would also be accessible to producers in countries linked by free trade agreements, countries that may operate under very different cost structures, labour standards, and regulatory environments. Rather than simplifying the competitive landscape, this provision adds yet another layer of complexity: manufacturers and investors must now assess not only which national markets offer resilience-weighted demand, but also who else qualifies to serve those segments and on what terms.

For anyone making investment decisions today, a factory financing decision based on the assumption of a 20 to 30% reserved EU market could look very different if that market is accessible to a much wider set of competitors. The risk is less about undermining the resilience framework outright than about creating a climate of ambiguity that will deter investment. For a manufacturer weighing a multi-tens-of-millions-euro factory decision, uncertainty over the actual size and accessibility of the reserved market can be as damaging as an outright reduction. Certain manufacturing projects may simply not proceed if the legislative text is accepted in its current shape. This point deserves close monitoring as the process unfolds, and honest assessment in every business case being built right now

The opportunity is real

Despite the complexity, the fundamentals are strong. EU solar PV demand is structural, with broad public acceptance of PV, natural rotation between market segments, geographic balance across Member States, and economic competitiveness across all regions.

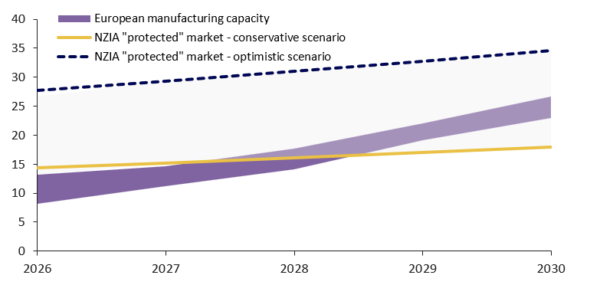

The numbers support this. Annual installations of 60 GW to 70 GW and above are the baseline, not the aspiration. Plus, Becquerel Institute’s current estimates suggest the NZIA framework could reserve between 18 GW and 35 GW of annual EU demand by 2030, spread across three segments: utility-scale auctions (8 GW to 17 GW), commercial and industrial public procurement (6 GW to 9 GW), and residential incentive schemes (4 GW to 9 GW). Today, a gap of roughly 10 GW separates European manufacturing capacity from the lower bound of this reserved market, but that gap is projected to close gradually as announced projects come online. By the end of the decade, EU manufacturers should be able to cover most of these segments.

Image: Becquerel Institute

The manufacturing pipeline reflects this. Large-scale projects (3Sun ramping to 3 GW in Catania, Holosolis planning integrated multi-GW site in France, MCPV in Spain) are moving forward with public co-financing secured. But the pipeline is not only about new greenfield factories. Existing manufacturers are also reinvesting: companies like Voltec Solar, BISOL, and others are modernising and expanding their lines, betting that the new market structure will reward those who are already operational and can scale.

Plus, an often-overlooked dimension sits upstream of manufacturing itself: production equipment. Europe retains a strong position in PV manufacturing equipment, a segment that has been quietly suffering as European factories closed. With technology cycles accelerating and production lines typically refreshed every five years, a genuine reshoring of cell, module, and inverter manufacturing in Europe would generate substantial demand for equipment suppliers too. This is a part of the value chain where the benefits of industrial reshoring extend well beyond the factory floor.

The reshoring target is achievable in the medium to long term. But “achievable” does not mean “automatic”. Converting pipeline into operating capacity requires navigating a market where the rules vary by country, the definitions of “European” are contested, the cost gap with Chinese manufacturers is real (though narrowing) and the policy signals, while stronger than ever, are still subject to electoral cycles and implementation risk.

What separates manufacturers who capture this opportunity from others is not ambition. It is granularity: knowing which national markets are moving fastest, where the demand pull from resilience auctions is largest, how cost structures compare segment by segment, and where sustainability, which is increasingly the factor on which European regulators and manufacturers can genuinely differentiate, creates a competitive edge that price alone cannot deliver.

What matters now

The immediate question for anyone operating in the EU solar PV value chain, whether manufacturing, developing, installing, or procuring, is which Member States are actually creating the demand that the regulatory framework promises. France and Italy are ahead on resilience auction implementation. Germany is around the corner. Spain is developing its approach. But across the board, the volumes earmarked for resilience-weighted tenders remain limited, in most cases, too limited to underpin the investment cases that announced projects need. The gap between NZIA ambition and actual auction volumes is the single most important number to track.

Where resilience auctions do exist, they fundamentally change the sourcing equation. The module and inverter procurement decision is no longer just a cost line, choosing the wrong supplier can mean losing the bid entirely. Where a component was manufactured, how its supply chain scores on sustainability criteria, and whether it qualifies under a given Member State’s specific rules now directly determine competitiveness at the tender stage. Most buyers will need to develop a dual-track supply strategy: established import channels for the roughly 60% of the market that remains price-driven, and access to European or resilience-qualified suppliers (with the documentation to prove it) for the 40% falling under NZIA-type provisions. Managing two parallel supply chains with different lead times, qualification requirements, and pricing structures is new territory for most procurement teams.

The cost dynamics are working in favour of this transition, though not for the reasons most people assume. European manufacturing costs are coming down through higher automation and, for new projects, through scale effects that the previous generation of small European factories never achieved. But the bigger driver is on the Chinese side: module spot prices have increased 15–20% year on year, moving closer to reflecting actual production costs after a period of below-cost selling. The gap is narrower than it was twelve months ago. Whether it stays narrow depends on Chinese capacity rationalisation, which is underway but far from complete.

The axis on which European suppliers can most credibly compete is sustainability. In a market where NZIA non-price criteria reward supply chain transparency, carbon footprint, circularity, and labour standards, this is not a nice-to-have, it is the differentiator. Manufacturers and developers who invest in eco-design, responsible sourcing, recyclability, robust documentation and certification, for modules and inverters alike, will be best positioned as resilience auctions scale up. Public entities face a particular challenge: under NZIA and its national transpositions, public procurement of PV systems is subject to criteria that go beyond standard tendering practice. Municipalities, public housing agencies, and infrastructure bodies launching solar PV tenders need to understand what qualifies under their national framework and structure their specifications accordingly, or risk non-compliance, legal challenge, or simply missing the opportunity to use procurement as a lever for industrial policy.

The window is open

Europe has tried to build a solar manufacturing base before, and failed. The difference this time is that the regulatory architecture exists, the demand is structural, and the geopolitical context with energy price volatility, supply chain concentration risk is doing what European industrial policy alone could not: making the case for diversification in commercial, not just strategic, terms.

But the complexity of the new market that will emerge, with three distinct segments, possibly 27 national implementations, contested trade rules, evolving sustainability requirements means that moving fast is not enough. Moving intelligently is what matters. The manufacturers, developers, and policymakers who understand the granular reality of each national market, each auction design, each segment will be the ones who make this cycle different.

The window is open. It will not stay open forever.

Authors: Philippe Macé, COO, Becquerel Institute & Gaëtan Masson, CEO, Becquerel Institute

Want to understand EU solar manufacturing competitiveness? Head to www.solarmanufacturing.eu and compare production costs across European locations and explore optimization scenarios.

About Becquerel Institute

Becquerel Institute is a strategic consulting company and applied research institute specialising in solar photovoltaics and energy transition. Founded in Brussels in 2014, with regional offices in France, Italy, and Spain, the Institute provides strategic advice across all segments of the PV value chain and is a recognised partner in European and international research programmes. Becquerel Institute has recently launched Solarintelligence.ai, an AI-powered platform giving PV stakeholders immediate access to verified, actionable market intelligence.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment