From pv magazine 10/2021

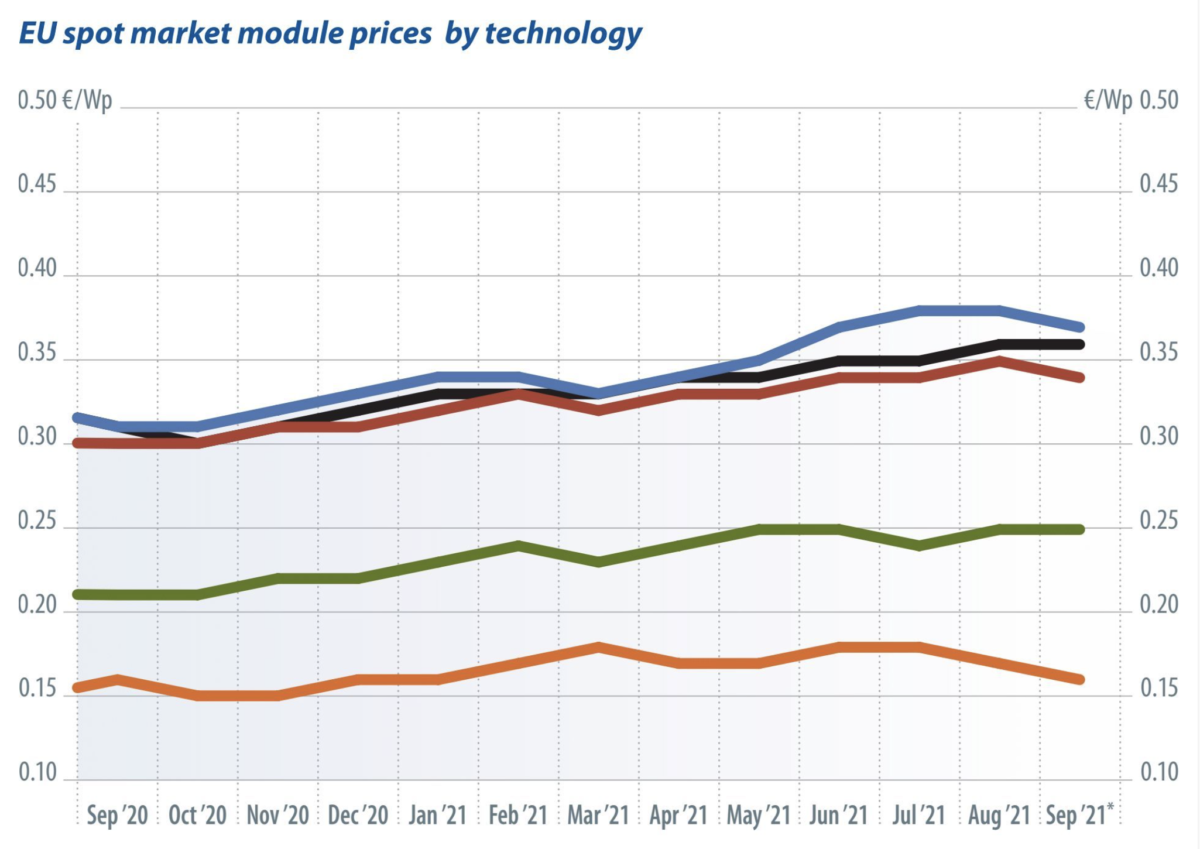

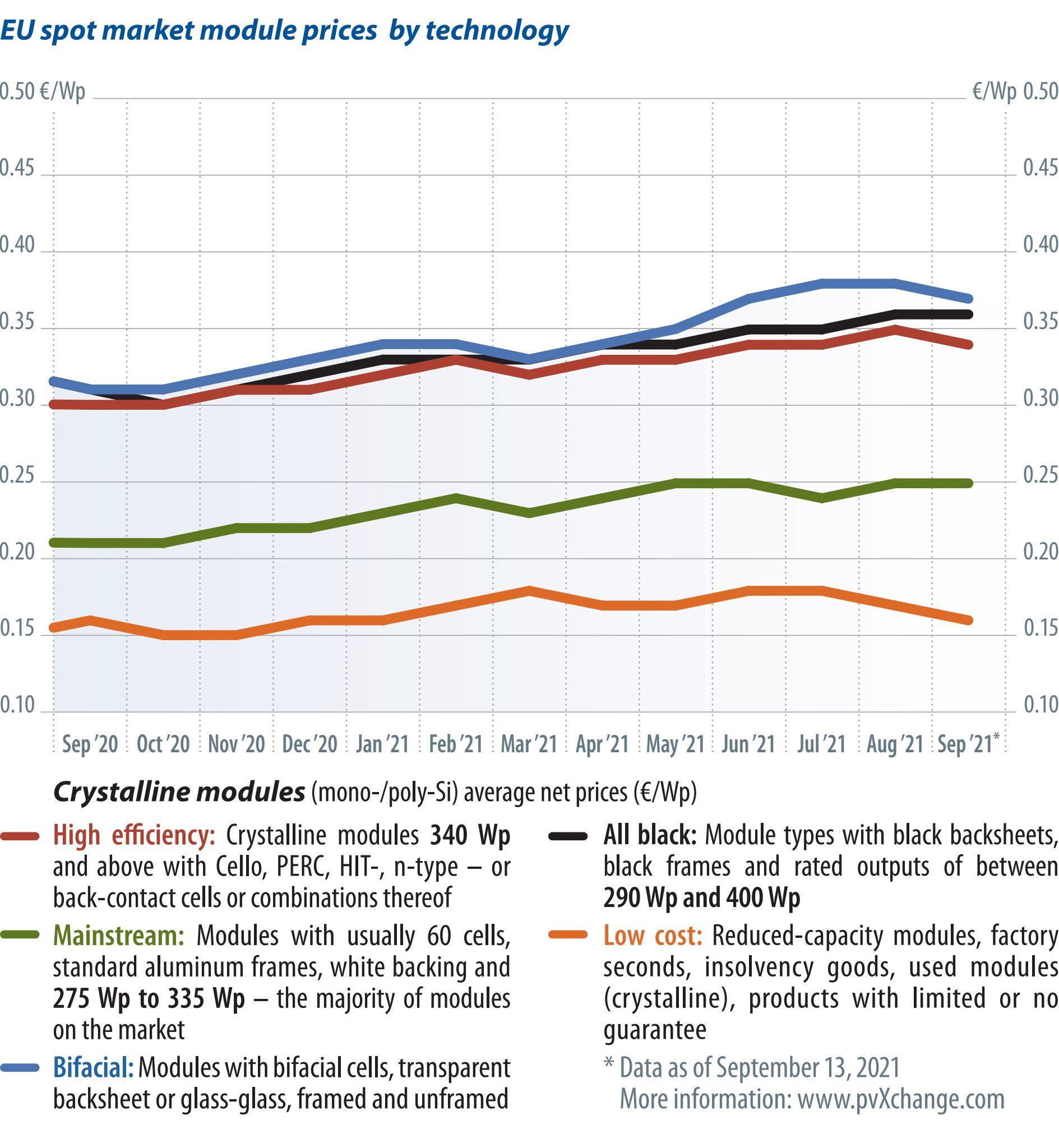

Module prices have stabilized in recent weeks and have even come down for most technologies. I attribute this to a drop in demand in the summer holidays on the one hand and the approaching end of the quarter on the other. Some larger volumes of modules have been released onto the market, which means availability is currently good, and prices are under some pressure as a result. Given that this is inventory adjustment and thus a short-term effect, I expect an upward correction in coming months. It is therefore unlikely that we will see the holding price increase of some 6% to 9% since the beginning of the year again.

The price that has been unchanged since January is in the low-cost category – low-power modules, factory seconds and secondhand panels – as these are usually local offers generally untied to container shipments from Asia.

But how can we step back from the large Chinese manufacturers in other product groups, and break free from prices dictated by freight and shipping companies?

Since Asian manufacturers began their conquest of Europe over a decade ago, all attempts by domestic producers to establish a competitive mass-market solar module have failed. Even the EU Commission’s protectionist regulation of the import of cells and modules from China from 2013-18 couldn’t save domestic industry.

Today, there is no longer any serious production capacity in the EU beyond final module assembly. Silicon, wafers, cells, glass, films, frames, cables and junction boxes are sourced from Asia or outside the EU. Some formerly respected German brands limit themselves to the words “Engineered in Germany” or “German warranty” in their data sheets, since the complete module or at least the finished laminate comes from Asia, and only the frame is pressed domestically.

Absent supply chain

Such “made in Europe” products aren’t much more expensive than Chinese modules, but they have no transport cost advantage because all of the materials come from Asia, too. The situation is not much better for local module manufacturers that still do the laminating themselves – they also import almost all of their upstream products from Asia.

Today, module production itself is highly automated, meaning personnel costs are low. The only disadvantages over Chinese production are energy costs and environmental regulations. But these can be eliminated with a little effort and innovation. The toughest nut to crack – at least over the short to medium term – is the procurement problem for materials. Vertical integration of a large number of production steps, if possible at one location, would be the solution, as would a large production capacity to achieve economies of scale. But this is precisely the crux of the problem, and why European players have fallen by the wayside, or never moved beyond the status of assemblers.

Whether Meyer Burger, the latest candidate in the race for a seat at the table among the otherwise Asia-dominated manufacturers, will succeed in doing the seemingly impossible, remains highly questionable. At least, I’ve been hard pressed to find anyone in the industry over the past few weeks who can imagine that the Swiss company will succeed in capturing a meaningful share of the market with its current setup and price structure. At present, the manufacturer is also struggling with the availability and cost of its raw materials, which has led to delayed delivery of module lots ordered many months ago, and to prices that are nearly double those of the large Tier-1 manufacturers. Even the company’s claim of better module quality and somewhat higher yields through the use of heterojunction technology, as well as the local producer bonus, are not enough to justify much higher module costs, in my opinion.

The Swiss company may be betting on the outcome of the German federal elections in September, for an associated change of government may create significantly better market conditions for domestic, high-priced products. A much higher CO2 price, for instance, could be a game changer. The government would also have to sweeten the pot considerably with regard to renewable energy infrastructure projects to enable the large-scale production of silicon and wafers. But what is clear is that without change, China will continue to dominate the European solar scene.

About the author

Martin Schachinger has been active in renewable energy for more than 20 years. In 2004, he founded the online trading platform pvXchange.com, where wholesalers, installers, and service companies can purchase standard components, solar modules, and inverters that are no longer manufactured, but are still urgently needed to repair defective PV systems.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.