From pv magazine 10/2021

In June, the U.S. Customs and Border Protection (CBP) issued a Withhold Release Order (WRO) against the world’s largest silicon metal manufacturer, Hoshine Silicon Industry, and its subsidiaries, without granting a grace period. Manufacturers exporting goods to the United States are required to provide documents on trade, manufacturing, and shipping methods of the products.

InfoLink’s research showed that some modules which had arrived in the U.S. between July and September were detained or sent back. As the FAQ regarding WRO does not include a list of required papers, it remains difficult for manufacturers to provide certificates of origin for silicon and silicon powder. Manufacturers mostly provide a declaration statement, PO, and bank slip for product traceability; no manufacturer has thus far provided a certificate of origin for silicon powder. In the face of increasingly high export risks, some Tier-1 module manufacturers have temporarily stopped shipments to the U.S. and have lowered their annual targets to the country.

Southeast Asia-based facilities, where manufacturers mainly ship products to the U.S., saw significantly lower OEM and in-house capacity utilization, which fell to 50% to 70% in September.

In addition to the impacts of the WRO, a group consisting of U.S. solar manufacturers filed petitions to the U.S. Department of Commerce in August, requesting investigations into Chinese cell and module companies circumventing tariffs by manufacturing in Malaysia, Vietnam, and Thailand. While measures against the circumvention remain unclear, some Chinese manufacturers expect to build a complete supply chain overseas, while other manufacturers are in wait-and-see mode, slowing their capacity expansion projects in Southeast Asia for now.

Solar manufacturers in Japan, South Korea, and Taiwan are watching closely for opportunities amid the China-U.S. trade dispute. According to our research, some manufacturers may shift some OEM orders to other manufacturers overseas. In fact, some have started to arrange this, or will come up with solutions before policy details are announced.

Indian optimism

Module demand in India stood at 4.5 GW to 4.8 GW in the first half, despite the Covid-19 pandemic and price increases across the supply chain, growing by more than double from 2.2 GW in the corresponding period last year.

Moreover, the 14.5% safeguard duty expired at the end of July, allowing a window to avoid punitive tariffs, as no additional tariffs were introduced by mid-September, before the basic customs duty is imposed in April 2022. India thus becomes a key market for module manufacturers in the second half of the year. Strong demand is expected in the fourth quarter to the first quarter of 2022, with module demand in the second half of this year likely to exceed 5.5 GW.

However, high module prices and ocean freight rates will affect the internal rate of return (IRR) of projects worldwide. It is reported that the Indian government will allow projects to postpone installation, although official documents have yet to be released as of mid-September.

Demand outlook

The United States and India saw more policy changes this year. Xinjiang-related legislation and the Chinese circumvention issue in the former case caused uncertainties for the market, slowing Chinese module makers’ shipment activities to the United States. Therefore, demand is slightly lower than expected in the last quarter due to module supply, and is estimated to come in at 12 GW to 13 GW. Driven by the window period of punitive tariffs in India, module demand is likely to surpass 5.5 GW in the second half.

Foreign policy changes aside, expensive modules and shipping rates will hit project returns in China and abroad. Experience in previous years suggests that inventory draw normally begins after the end of the summer holidays in Europe. This year, however, module inventory draw is moderate, thanks to high module prices and shipping delays. EU module demand in the second half is therefore projected to be around 20 GW.

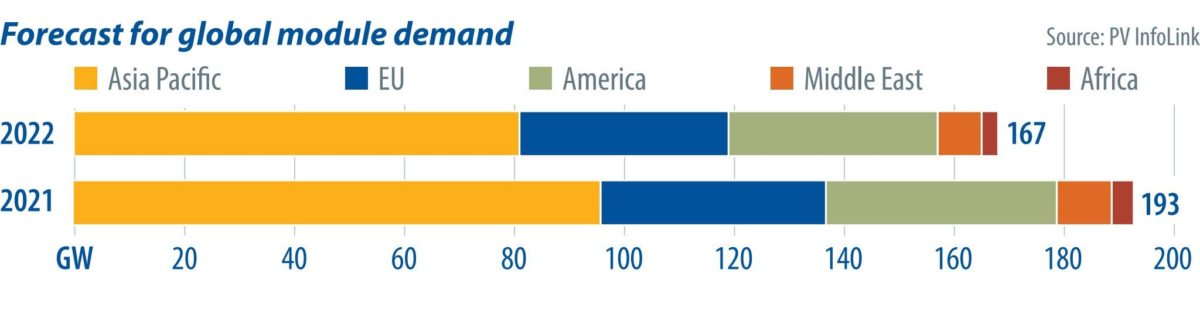

End users’ low acceptability for module price increases in China and overseas markets led to the postponement of some orders to the first half of 2022. Demand in the fourth quarter therefore turns from optimistic to uncertain. With high module prices, demand this year is expected to hit 165 GW to 170 GW. In 2022, demand will be sustained in the first half by projects deferred from this year, enabling prices in the supply chain to hold ground instead of turning weak, as forecast earlier.

Driven by the province-wide promotion of distributed PV projects, Chinese demand looks bright and will likely grow robustly next year. By then, China’s share of global PV demand may grow even further. In light of this, InfoLink raises its demand forecast to 190 GW for 2022.

As per observations in the first half, end users could hardly accept glass-backsheet modules rated beyond 500 W being priced higher than CNY 1.80/W ($0.28/W), with demand being impacted to some extent. Given trade disputes, the time required for new polysilicon capacity to come online, and the impact of raw material factors on module prices, module makers are conservative about price quotes for 2022.

For now, 182 mm and 210 mm glass-backsheet modules are projected to stay at CNY 1.78-1.80/W and $ 0.245-0.25/W. In the fourth quarter, the FOB prices of glass-glass modules rated beyond 500 W in the U.S. range from $0.29/W to $0.30/W. Prices for 182 mm and 210 mm glass-backsheet modules in India saw little difference from the international level, sitting at $0.245-$0.255/W. The rate of price decline in the first half of 2022 will be rather slow. The profits of module makers are likely to recover in the first half of next year when polysilicon and wafer prices begin to slip.

About the author

Amy Fang focuses on research and analysis of the solar cell segment of the supply chain. She supports PV InfoLink in producing market trend analysis and works across price forecast and production capacity data services. Fang continues to contribute to solar cell technology research efforts, analysis of market trends, and timely market information.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.