From ESS News

The opening session of BBDF day two brought project completion into focus, with discussion centering on the very real work required to get a ready-to-build project across the line.

Industry experts detailed the complex negotiations that need to happen between parties, with banks, optimizers, developers, and an engaged industry audience all sharing their perspectives. From working with distribution system operators and navigating flexible grid connection agreements, to securing credible revenue streams, attendees delved into the practicalities of completing a BESS project in 2026.

Real-world examples were the cornerstone of the session, and attendees were treated to presentation detailing two distinct paths to market for projects conceived in Germany.

Marcel Marquart, country manager for Germany at Clean Horizon, presented a 50 MW/150 MWh standalone project, representing a pure merchant approach. Meanwhile Xenia Ritzkowsky, senior consultant at Enervis energy advisors, laid out a co-located model where a 20 MW battery is added to an existing 25 MWp solar farm with a 20 MW grid connection already in place.

The dual focus set the stage for a debate between the higher revenue potential of standalone assets, and the cost savings that can co-located BESS can secure by sharing infrastructure.

The DSO labyrinth

Grid connection is the primary obstacle to BESS deployment, according to recent surveys of developers, followed closely by securing financing. BBDF attendees heard how flexible connection agreements (FCAs) have evolved from simple permits into complex, location-specific documents that dictate how an asset can actually behave on the grid, and that can change at in the project development timeline.

Marcel Marquart illustrated the current climate by setting out three FCA scenarios. Case A was presented as the restriction-free scenario and, in 2026, was deemed unrealistic. Case B was presented as a more realistic scenario, introducing a ramp rate restriction of 10% of installed power per minute and a limit on participation in ancillary services to 50%. Case C was a 5% ramp rate and a two-hour order book freeze before delivery – somewhat unrealistic for being too restrictive, and more of a developer’s nightmare. The presentation continued with the middle road Case B acting as the reference.

One of the major pain points discussed was the instability of rules developers must stick to.

Stephen Stakhiv, fund and investment manager at Flower, shared a cautionary tale from the field in Germany. Stakhiv told the audience that “a few weeks ago, a DSO came back and revised a ramp rate to a level that made the project unfinanceable.”

This kind of pivot is exactly why early-stage engagement is basically mandatory.

Anoucheh Bellefleur, team manager market and strategy at ABO Energy, noted that these major design and technical spec decisions occur pre-ready-to-build (RTB) and require ongoing communication with lenders.

Developers are pushing for better exit strategies to protect against this. Bellefleur suggested negotiating clauses that allow a developer to return the grid connection and recover their down payment (BKZ) if the DSO renders the project technically impossible. It is about de-risking that first down payment, which can often be millions of euros.

The realities of virtual trading

Optimizers can have different views based on the realities of trading and Marcus Fendt, managing director at The Mobility House pointed out that financial models often overestimate the physical impact of these limits. He explained that normally every trade can be thought of like an option, and patterns of actual battery charging and discharging don’t reflect trades.

The Mobility House MD also pointed out that roughly one in every six-to-ten trades are physical, and the rest are virtual, just as in options markets for commodities – essentially, actual delivery is not required. Because virtual trades do not hit the physical grid, the ramp rate does not influence the internal rate of return (IRR) as significantly as an ancillary services restriction would. However, it was emphasized that lenders will only buy into this if advisory explicitly model flexible connection agreement assumptions into the revenue stack from day one.

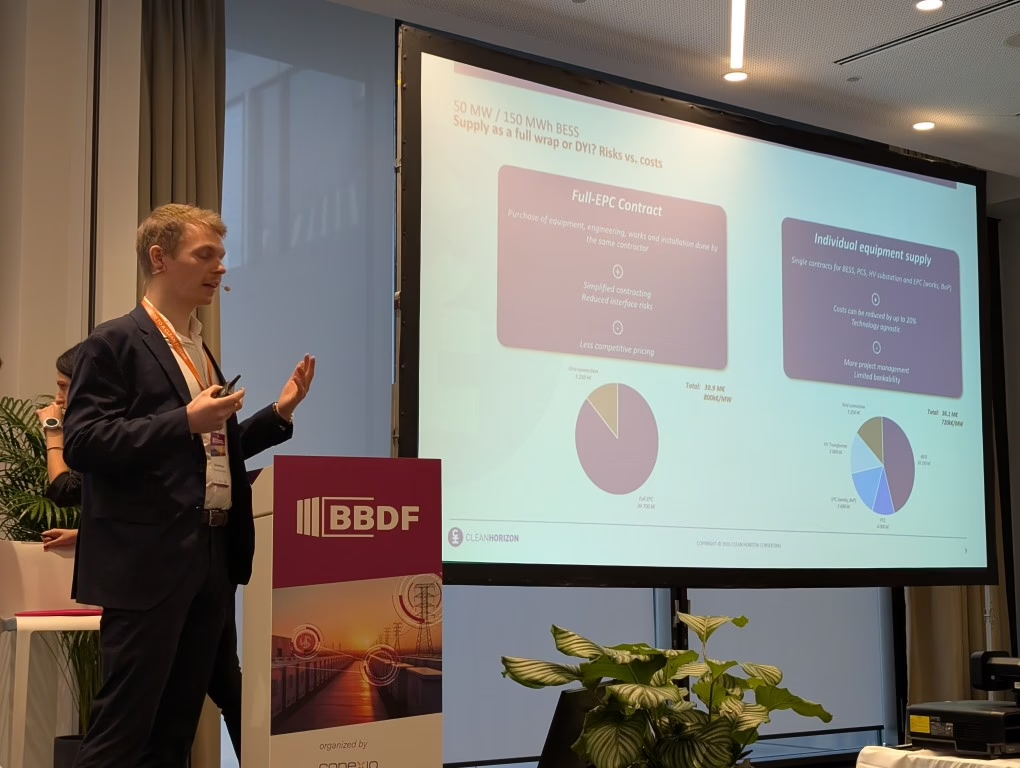

Procurement: Turnkey EPC or DIY?

Attention then turned to engineering, procurement and construction (EPC). Panelists discussed whether developers go with a full EPC wrap deal, a turnkey style contract where the EPC supplies all equipment and charges a margin, or a DIY multi-contract approach.

Bankability is the main catch. Savings can be valuable, but the risks are multiplied. Tim Koenemann, Global Head Green Infrastructure Finance at Commerzbank, said that while BESS is not the most complex thing to build in terms of large infrastructure projects, the interface risk of multiple contracts is a hurdle for debt. From a bank’s perspective, a full wrap EPC is just easier. If a developer goes the individual supply route, the bank needs a very high degree of trust in the sponsor to manage those interfaces.

Developers such as ABO Energy echoed this, noting that moving away from a full wrap requires a strong internal capacity to handle all these different interfaces and make sure you have an airtight strategy for aligning warranties. Audience members also asked how other parties can be involved, such as owners’ engineers, making DIY efforts less risky; and integrators, who can supply more than just the BESS by providing all other power components. There are many other strategies that fall between full turn-key or full DIY.

Multiple panelists agreed that the multi-contract nature of DIY projects can cause issues. Koenemann said that from the bank’s perspective, multi-contracts are tough to finance, especially for new players where “finger-pointing” over performance guarantees can jeopardize the project. Bellefleur of ABO Energy explained that strong internal experience and skill in handling multi-contracts is critical here.

Sizing debt against merchant exposure

Risk-sharing is the name of the game for BESS financing in Germany. Traditional lenders are still wary of 100% merchant exposure, a fact that has been echoed throughout BBDF. Koenemann said that for Commerzbank, a non-contracted strategy is not yet bankable. For non-recourse project finance, the market generally wants to see 50% to 60% of the capacity rented out for five to seven years via a tolling agreement.

This creates a split in how debt is sized. Tolling portions might see a Debt Service Coverage Ratio (DSCR) of 1.15, while merchant portions need a much larger cushion, often a DSCR of 2.0, to handle the volatility.

Both Marcus Fendt and, later, Anoucheh Bellefleur made a gentle challenge to the conservative posture of the banking sector and those operating BESS.

Fendt argued that banks often just look at the downward trend of prices, but in some cases, banks should be aware of upward trends. He cited California, Australia, and the United Kingdom as proof that regulators eventually recognize the value of storage and can offer new products that support the grid and offer additional revenue.

“Our regulator will recognize in five to seven years the value of storage,” Fendt predicted, suggesting that those who bridge the current gap now will reap the rewards later.

Bellefleur also noted that developers may want to retain a minority stake in a project to capture potential upside while spreading risk.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.