U.S. utility-scale solar falls below US$1 per watt (w/ charts)

Starting in the second quarter of 2016, PV module prices began a free-fall which has brought great pain to PV makers, and may be the greatest single factor in the bankruptcies of the two largest U.S. crystalline silicon PV makers, SolarWorld and Suniva.

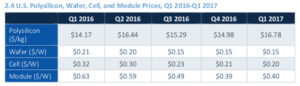

GTM Research and Solar Energy Industries Association (SEIA) are reporting that average module prices fell by a third from Q2 to Q4 2016, to land at $0.39 per watt in the fourth quarter, and only rebounded to $0.40 per watt during Q1, in the latest U.S. Solar Market Insight report.

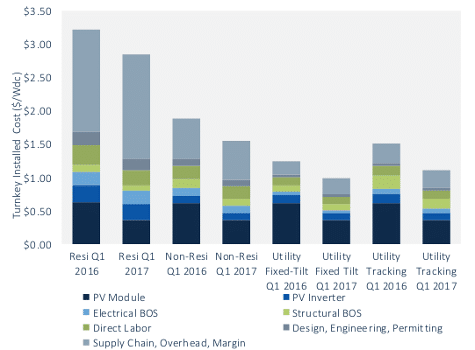

However, this collapse and similar declines in the prices of other components has helped the U.S. utility-scale solar sector to reach a new record. The report found that for the first time, the average price of fixed-tilt solar PV systems has fallen a penny below $1 per watt-DC, a 6% decline from the previous quarter.

The average price of PV systems using single-axis tracking was not much above that at $1.08 per watt, which also represented a 6% fall.

“Primarily driven by the global module demand and supply imbalance, hardware markets produced aggressive component price declines in Q1 2017,” notes the report’s executive summary. GTM Research and SEIA estimate that hardware costs fell 9-10% for utility-scale solar.

“Primarily driven by the global module demand and supply imbalance, hardware markets produced aggressive component price declines in Q1 2017,” notes the report’s executive summary. GTM Research and SEIA estimate that hardware costs fell 9-10% for utility-scale solar.

This is leading to new record low prices for power contracts as well. While prices below $30 per megawatt-hour (MWh) had been reported in the United Arab Emirates and Mexico, in May Arizona utility Tucson Electric Power reported that it had signed a 20-year contract with an affiliate of NextEra Energy for electricity from a solar project at under $30/MWh.

This is the lowest price that pv magazine staff have seen for a power contract in the United States to date. And while this is may be an outlier, GTM Research reports that during Q1 power purchase agreement (PPA) prices averaged between $35 and $50/MWh.

U.S. Solar Market Insight also found ongoing declines in the commercial and industrial (C&I) and residential markets, with prices for the “non-residential” distributed sector falling 4% to $1.56 per watt, and residential rooftop prices falling 2% $2.84 per watt. This fall in the residential sector is despite difficulties in customer acquisition, which have prevented meaningful reductions in soft costs.

And while the residential market has been somewhat hamstrung by a combination of customer acquisition issues and policy changes, the fall in utility-scale costs bodes well for the sector.

While utility-scale procurement in 2017 is being driven primarily by contracts signed under the auspices of the Public Utilities Regulatory Policy Act of 1978 (PURPA), in 2018 GTM Research expects voluntary procurement to replace PURPA as the biggest driver, as utilities seek out solar as a hedge against gas prices.

However, there is one significant caveat to all of this good news. The U.S. International Trade Commission is currently investigating Suniva’s section 201 petition, and if it rules in Suniva’s favor this leaves the door open for any sort of trade action by the Trump Administration. Suniva has asked for a $0.78 per watt minimum price on imported PV modules, and this alone would throw a major wrench into both procurement and projects which are already underway.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment

[…] capacity forecast to be added for this year. Earlier this year, utility-scale solar prices dropped below $1 per watt for the first […]

[…] capacity forecast to be added for this year. Earlier this year, utility-scale solar prices dropped below $1 per watt for the first […]

Doubling the price of modules and setting a fixed cost is ridiculous. Why don’t we just put it back to $2/w and bring back Solyndra and United Solar Ovonics while we are at it.

[…] más alto, vieron sus precios reducirse en un 6 por ciento hasta alcanzar 1,06 dólares por vatio (artículo completo en inglés […]

How much would it cost the rest of the industry to buy Suniva in order to close down the suit?

And can’t the editors of the site find stock photos of solar farms that show some minimal sensitivity to the environment, rather than giving free publicity to yahoos?

[…] energy for society at a very low cost. Utility solar farms are now being installed for less than one US dollar per watt of capacity, and some projects in the United Arab Emirates and Chile are delivering energy for less than 3 US […]