The weekend read: Out with the old…

From pv magazine, April edition.

In polysilicon production, electricity accounts for nearly 40% of the cost, a higher proportion than in any other segment in the PV supply chain. As a result, Chinese manufacturers have expanded into western and northwestern regions where the electricity rate is around RMB0.26/kWh ($0.039), to lower production costs effectively for new capacity in the past few years.

From the end of 2018 through early 2019, large manufacturers – including Yongxiang’s factories in Leshan and Baotou cities; GCL Poly’s factory in Xinjiang; Xinjiang Daqo New Energy Co., Ltd.; and Asia Silicon (Qinghai) Co., Ltd. – released new capacity from upgrade or expansion plans with production costs 30-40% lower than in the coastal regions or overseas. But as South Korean companies including Hankook Silicon, Hanwha Chemical, and OCI – as well as China’s LDK Silicon, Yichang CSG Poly and DL Silicon – were under equipment maintenance programs, supply and demand for polysilicon remained balanced in the final quarter of 2018, with China’s polysilicon prices for mono-Si at RMB80-86/kg and RMB73-78/kg for multi-Si.

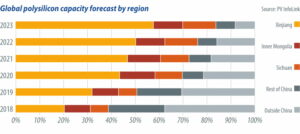

Looking at the first quarter of this year, Xinjiang-based TBEA and OCI’s factories in Malaysia have also started releasing new capacity in addition to that released by Yongxiang, GCL Poly and Daqo New Energy. So far, global polysilicon capacity has reached 119,000 metric tons (MT), a 12% increase on the 106,000 MT seen in Q4, 2018. Newly added capacity in western and northwestern China will represent half of global polysilicon capacity by the end of the year.

Following the release of low-cost capacity in the northwest regions of China, the overall prices for polysilicon are gradually declining, threatening Chinese poly manufacturers saddled with legacy, higher-cost capacity and making it difficult for overseas producers to survive.

Non-Chinese manufacturers

Under the impact of China’s anti dumping and anti subsidy polices, U.S. polysilicon companies were forced to withdraw from the Chinese market. Moreover, the production capacities of mono-Si and multi-Si wafers held by non-Chinese manufacturers are low, causing a stressful situation for U.S. companies. Although the tariff imposed on South Korean producers is much lower than that slapped on their U.S. peers, the cost for exporting South Korean polysilicon to China has also increased.

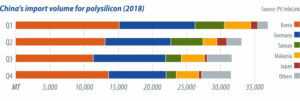

Among China’s newly added polysilicon capacity, that of mono-Si wafer represents 60-80%, helping to reduce China’s dependency on imports in recent years. Since last year, imports of polysilicon have gradually decreased on a quarterly basis, reflecting China’s falling dependency on overseas polysilicon. With high production costs and trade barriers in place, some non-Chinese polysilicon manufacturers can only rely on long-term contracts signed in earlier years. In the long term, polysilicon manufacturers outside China will drop out of the market after the termination of those long-term contracts.

Chinese polysilicon

Compared with overseas polysilicon manufacturers, the production cost for China’s older capacity, and that in coastal regions, is not much lower. Manufacturers with fewer cost advantages may reduce or even suspend production in the first half of this year. Combo, Sino-Si and GCL Poly’s factories in Xuzhou, for example, are likely to decrease output or close old capacities.

If all of such high-cost capacity suspended production at this point, the first half of this year could see a net increase in output of 8,000-10,000 MT from the final three months of last year – still reasonable with 20 GW of global demand growth expected this year. It would also lead to a slight downward trend in polysilicon prices during the low season this year.

If demand starts to increase significantly in the second half, at the same time as some polysilicon manufacturers close lines to conduct equipment maintenance, PV InfoLink predicts polysilicon prices will rebound more than any other component along the entire supply chain.

Despite gradual increases in low-cost capacity in western and northwestern China, high-cost capacity has also withdrawn from the market since the second half of last year, leading to an increase in market concentration. This phenomenon also explains the slight downward trend in polysilicon prices despite continuous production capacity expansions.

PV InfoLink predicts the lowest price point of polysilicon for multi-Si wafer will be RMB66/kg, with RMB76/kg for mono-Si wafer, dropping slightly by 6-7% compared to the prices seen in early March.

As suppliers become concentrated, prices will be contained. Overall prices are likely to rebound dramatically late in the year, reaching a level higher than the RMB87-93/kg seen in the first three months of this year.

As for module supply, due to subsidy cuts worldwide prices for modules are likely to rise slightly despite a demand increase in the second half. Moreover, wafers and cells usually reflect price trends for polysilicon immediately, due to limited profit margins for multi-Si wafer and multi cells, so module profits may decrease a little during the high season in the second half. That is the reason module manufacturers have been actively producing more high-efficiency products this year, and it’s crucial for them to speed up improvement of their profit margins.

By Corrine Lin

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment

The article was obviously written in early March when PV InfoLink still reported polysilicon spot prices of RMB70/kg for multi grade and RMB80/kg for mono grade in China. In the meantime, PV InfoLink’s own data have fallen to RMB58/kg for multi grade and RMB74/kg for mono grade. The price for multi grade already is substantially lower than the predicted RMB66/kg, and this is not yet the end of the road.

In my view, the shakeout of legacy high-cost by new low-cost (subsidized) capacities will not be as smooth as the article insinuates. China’s polysilicon output in the first quarter of 2019 was 15,000 metric tons (MT) higher than the volume in Q4 2018, thus already exceeding the net increase of 8,000 to 10,000 MT projected by PV InfoLink for the first half of 2019 (if one leaves decreasing imports aside). Launching more than 200,000 MT of new capacity within just twelve months simply means brutal cut-throat competition.