Energy transition slowly forcing hand of oil, gas, but green investment still low

A new report issued by U.K.-based non-profit charity CDP titled, Beyond the cycle: Which oil and gas companies are ready for the low carbon transition?, has ranked 24 of the largest and highest impact publicly listed oil and gas companies, representing around 31% of global oil and gas production, on their business readiness for a low carbon transition.

European players have been found to lead the way in most areas, with Equinor, Total, Shell and Eni in poll position; while CNOOC, Rosneft and Marathon Oil are being left behind. “The five European Majors and Repsol collectively account for 84% of the disclosed US$22 billion invested in alternative energies since 2010 by all 24 companies,” write the authors.

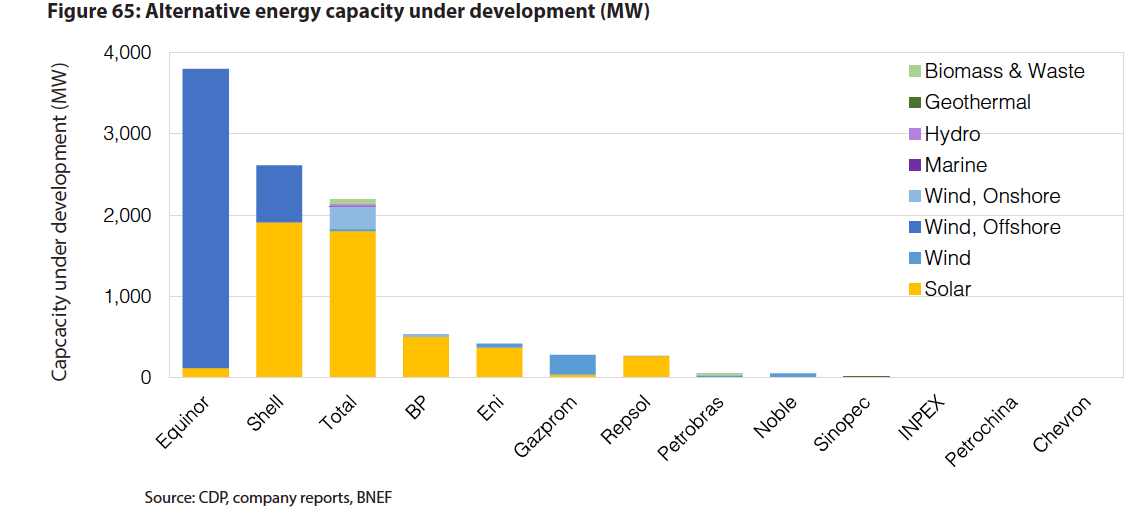

CDP calculates that the companies examined currently have 7.7 GW of renewables capacity in operation, with another 10.2 GW under development. Of this, European companies account for 70% and 94%, respectively.

BP, meanwhile, is said to have the largest alternative energy business, although Equinor, Shell and Total have more plans in their pipelines.

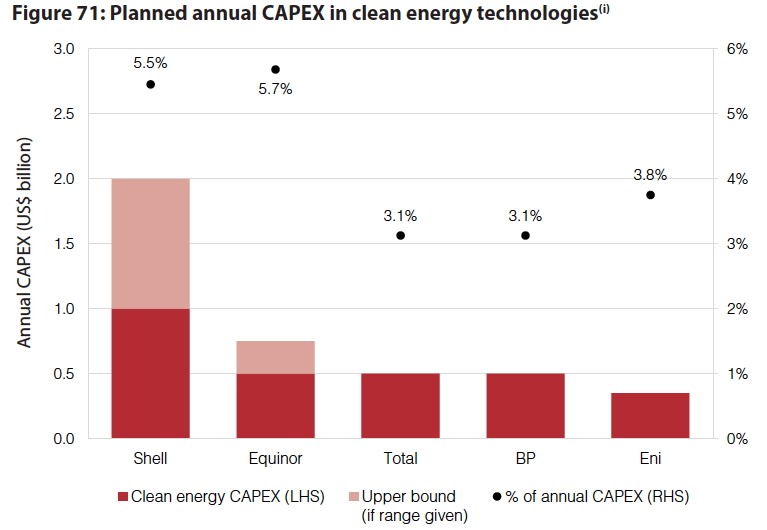

In terms of planned annual CAPEX in alternative energies, CDP finds that Shell leads the pack, aiming to spend 5.5% or between $1 billion to $2 billion annually, with Equinor, Total, BP and Eni each planning between just under half a billion to just over half a billion.

In terms of planned annual CAPEX in alternative energies, CDP finds that Shell leads the pack, aiming to spend 5.5% or between $1 billion to $2 billion annually, with Equinor, Total, BP and Eni each planning between just under half a billion to just over half a billion.

While the headline news is good, when compared to their overall capital expenditure (CAPEX), anticipated to be $260 billion for 2018, a measly 1.3% is set to be invested into low carbon assets this year.

Climate strategy = overall strategy

“Going forward, there can no longer be any difference between overall strategy and climate strategy,” state the authors. Indeed, with mounting pressure from stakeholders including consumers, investors and regulators pushing for an energy transition, the oil and gas industry is increasingly being forced to rethink its strategies.

As proof, the authors write that votes for shareholder resolutions regarding the goal to limit global warming to 2 degrees Celsius grew to 53% this year, up from 21% in 2014. This has led to nine of the examined companies publishing a 2 degrees Celsius scenario analysis, they say, and 15 setting corporate emissions reduction targets.

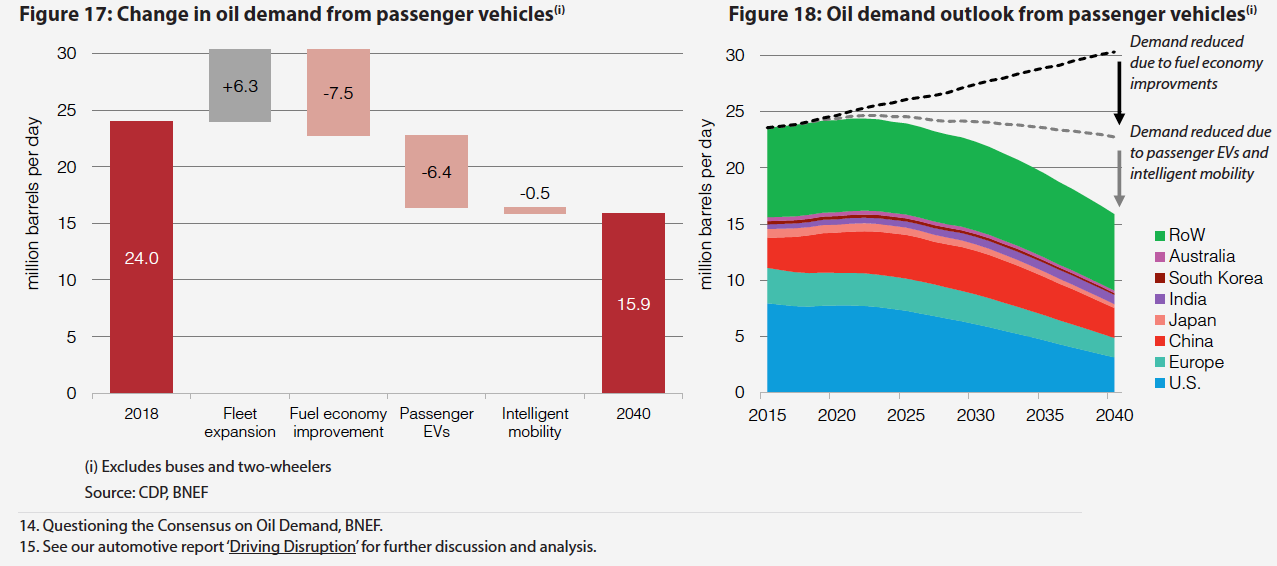

Furthermore, the changing transportation landscape, with electric vehicles and intelligent mobility, will also play a big role in how oil and gas companies operate in the future. While passenger vehicles are currently said to account for 24 million barrels of oil per day, out of the global demand for around 99 barrels, the aforementioned technologies could see this significantly disrupted, with a 34% decline by 2040, according to Bloomberg NEF.

In addition to capitalizing on the dropping costs of renewables – by using on-site solar instead of fuel gas, for instance – the companies reviewed are also looking to digitalization and innovative technologies to improve efficiency and productivity.

Regarding renewables specifically, CDP writes that although returns on solar and wind projects are typically half of what is usually expected from upstream oil and gas projects, the former pose far less risk than the latter, meaning in the longer term, they are “much more attractive”.

“Technological advances are driving costs down and long-term revenues and stable cash flows provide oil & gas companies a hedge against long-term threats to oil & gas demand,” write the authors.

Overall, they conclude, “Engagement, collaboration and innovation will be more crucial than ever. Climate-related targets and alignment of governance and remuneration structures with low-carbon objectives may very well form part of the industry’s social license to operate in the coming years.”

Please login to comment