From pv magazine 08/2020

Downward price trends have reached the polysilicon segment, dragging down prices for mono-Si wafers to a new low in the second quarter. With downstream demand continuing to grow, polysilicon prices for mono- and multi-Si wafers will rise steadily amid an ongoing supply shortage.

Electricity accounts for more than 30% of polysilicon production costs. This has driven producers to expand capacity into regions of western China where electricity prices can be as low as RMB 0.26/kWh ($0.033/kWh). China now hosts 85% of global polysilicon capacity.

The past year has seen polysilicon manufacturers in other regions withdraw from the market as their manufacturing costs are too high. Those with multi-grade polysilicon capacities are unable to upgrade to mono. At present, only a few producers run the business, but at low profit margins.

TBEA and Daqo New Energy each brought new capacity online in the second half of 2019 and the first six months of this year. The cash costs of these new lines range from RMB 35-40/kg before tax, or even lower. This is 40% to 50% lower than overseas producers.

Industrial accidents

In response to the downward price spiral in the second quarter, manufacturers planned reduced output and equipment maintenance in a bid to stabilize prices, but halted this plan after South Korean producer OCI announced the closure of its domestic solar-grade polysilicon plants. Germany’s Wacker also cut production. As a result, polysilicon prices continued to trend downward.

Daqo New Energy encountered an accident during maintenance at the beginning of July. That affected the Phase-1 5,000 MT production line, which is around 400-500 MT of monthly production. As the scale of the accident was small, the company is expected to resume full production soon.

An explosion occurred at GCL Poly’s Xinjiang facility in mid-July, as it was undergoing equipment maintenance. The manufacturer has suspended production and is investigating the cause of the explosion. The accident has heavily impacted its capacity, and there will likely be no production until the fourth quarter.

The market saw an escalated shortage of mono-grade polysilicon in the second half, due to the accidents and delivery hiccups in Xinjiang. With inventories in the upstream and downstream segments still low in the second half, and mono-Si wafer producers running at full clip and bringing new capacity online, mono-grade prices slightly rebounded. Multi-grade also rose due to growing demand, as well as diminished supply due to a shift to mono-grade production. Over the past year, Tier-2 and Tier-3 producers focused on multi-grade polysilicon – including Orisi Silicon, Hoshine Silicon, Dunan, Combo, and Jingyang – have all ceased production. Foreign manufacturers including Elkem, Hanwha Chemical, and OCI’s facility in South Korea also followed suit. Meanwhile, OCI’s Malaysia plant has been under maintenance since early June and expects to resume production at the end of July. Overall, global polysilicon capacity was 543,000 MT in the second quarter, and will rise 5% to 571,000 MT in the fourth quarter. The additions will mainly come from GCL Xinjiang and East Hope, which are increasing activity on new lines toward the end of the year. At present, Tier-1 producers such as Yongxiang, Daqo New Energy, TBEA, and East Hope account for 52.7% of total polysilicon capacity, and their cash costs are below RMB 45/kg.

Beyond China

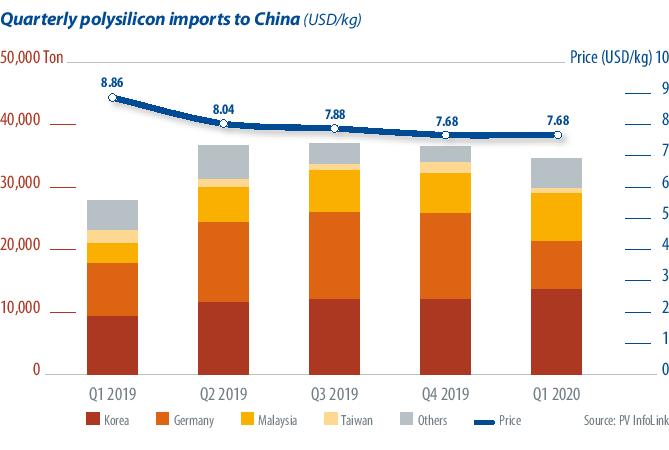

China’s Ministry of Commerce said at the beginning of this year that China will maintain anti-dumping and countervailing duties on solar-grade polysilicon imports from the United States and South Korea. This means imports from the U.S. will shrink compared to previous years. The tariff rate on polysilicon imports from Korea is far lower than from the United States, but Korean manufacturers have still lost their competitive edge in China, as they faced higher costs and falling polysilicon prices in the second quarter.

Most Chinese producers started to increase mono-grade polysilicon by modifying lines from the second half of 2019, to align with stable demand for monocrystalline products. Tier-1 manufacturers can reach around 90% mono-grade capacity, while Tier-2 and Tier-3 players can reach 80%. This has made China less dependent on imports, but has also caused a multi-grade polysilicon supply shortage.

In China, Tier-1 manufacturers’ older lines will likely become a burden on their businesses, and they are likely to cut or suspend activities on these, including TBEA’s first-phase line, as well as Yongxiang Leshan and GCL Jiangsu’s lines.

At present, monocrystalline products account for more than 80% of the market. With a significant increase in demand for mono-grade polysilicon and mono-Si wafers, Tier-1 manufacturers now aim to bring production of mono-grade polysilicon to more than 95%. Tier-2 producers that focused on multi-grade polysilicon are also modifying production lines to increase mono-grade output. However, there is limited room for such upgrades due to technical barriers and product positioning. How much mono-grade these producers can achieve is largely dependent on their overall competence and scale of optimization.

PV InfoLink projects that mono-grade polysilicon prices will come in at RMB 66 ($9.45)/kg, while multi-grade will reach RMB 39 ($5.58)/kg by the end of the year. For now, inventories are low, and with polysilicon supply running increasingly short and downstream demand growing gradually, prices for both mono- and multi-Si grade polysilicon are likely to rise.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.