Oil-dependent markets in the Middle East have a strong incentive to diversify their economies and have all set ambitious renewable energy goals. If they are to be realized, the region will have to deploy more than 50 GW of solar PV by 2030.

The development of PV has also been driven by public sector support. Even though the industry experienced a slowdown during the global Covid-19 pandemic, solar energy is once again at the heart of economic recovery efforts. Oil prices are now back at a higher level and supply chain issues are not as severe.

In this article, we profile the large PV markets in the Middle East that are expected to lead the region in solar PV deployment.

United Arab Emirates

The UAE has been at the forefront of the clean energy transition in the Gulf region in terms of PV deployment and ambitious renewable targets. The Emirates aims to generate 50% of its electricity from carbon-free sources, driven mainly by solar PV, by 2050. Abu Dhabi, for instance, plans to install 5.6 GW of PV capacity by 2026 and Dubai aims to source 75% of its electricity generation from renewables by 2050.

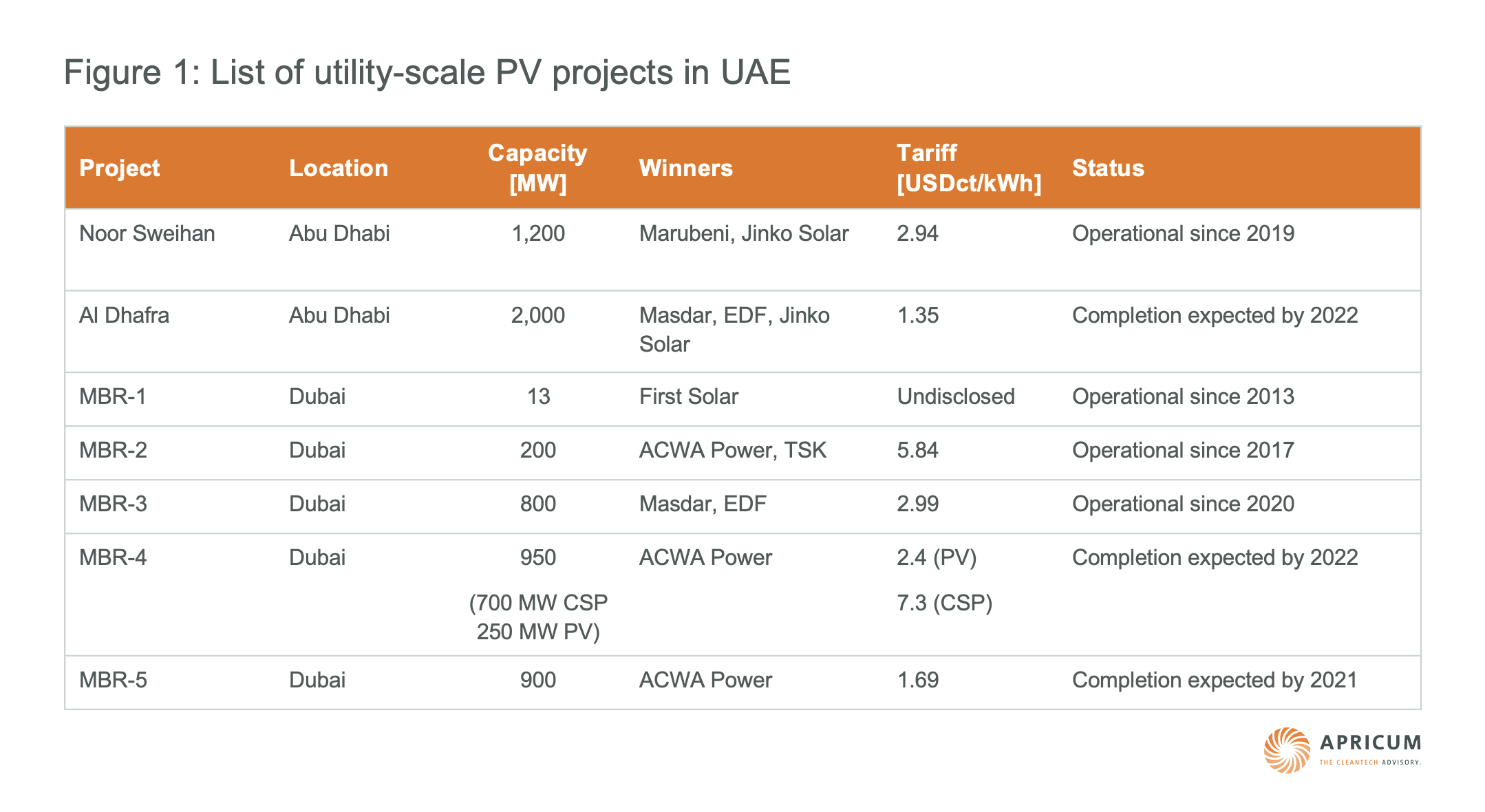

Both have been the frontrunners of the Middle Eastern PV industry. Abu Dhabi hosts the world’s largest operational PV plant, the 1.2 GW Noor Sweihan project, which has been feeding electricity into the grid since 2019. The plant is backed by Marubeni and JinkoSolar and has a 25-year power purchase agreement (PPA) with a tariff of 2.94 USDct/kWh.

Another giant project, the 2 GW Al Dhafra plant, is expected to be operational by Q1 2022. This private public partnership project will be 60% owned by the Abu Dhabi National Energy Company (TAQA) and 40% owned by a consortium comprised of EDF, Masdar, and Jinko Solar. A 30-year PPA will be in place with a tariff of 1.35 USDct/kWh.

Utility-scale PV installations in Dubai are clustered in the giant Mohammed bin Rashid Al Maktoum Solar Park (MBR solar park), the development of which is planned over several phases. Once fully complete, this mega solar park will reach 5 GW in capacity. The Dubai Electricity and Water Authority (DEWA) holds the majority equity share in the project. Each phase sees a growing installed capacity with declining tariffs.

The fourth phase will include a large share of concentrated solar power (CSP). There is also interest from the northern Emirates to become involved with Etihad Water and Electricity having set targets of executing 100 MW of solar PV projects. No further details have yet been revealed, however.

As the level of solar penetration increases in the grid, we expect regulations to expand allowing for small-scale, behind-the-meter storage in association with time-of-day tariffs. Utility-scale tenders mandating a specific size of storage to allow for power plant ramp up and ramp down in coherence with other generation assets are expected. Such regulations would allow for better use of the distributed energy sources that exist on the grid and enable the economical and reliable operation of the electrical network with mixed generation assets working side by side.

Saudi Arabia

Saudi Arabia

In 2019, Saudi Arabia dramatically increased its 2023 renewable energy targets from 9.5 GW to 27.3 GW under its National Renewable Energy Program (NREP). This program divides the 27.3 GW goal into 20 GW of solar PV and 7.3 GW of wind. In addition, the Vision 2030 program sets another ambitious target of 60 GW of renewable electricity capacity by 2030 that will include 40 GW of PV and 2.7 GW of CSP capacity, and the sourcing of 50% of electricity generation from renewable technologies.

The bulk of the target capacity is expected to be reached via large-scale tenders and other mega projects such as NEOM, a sustainable zone in northwest Saudi Arabia that is planned as the hub for the Saudi green economy and a landmark for sustainability.

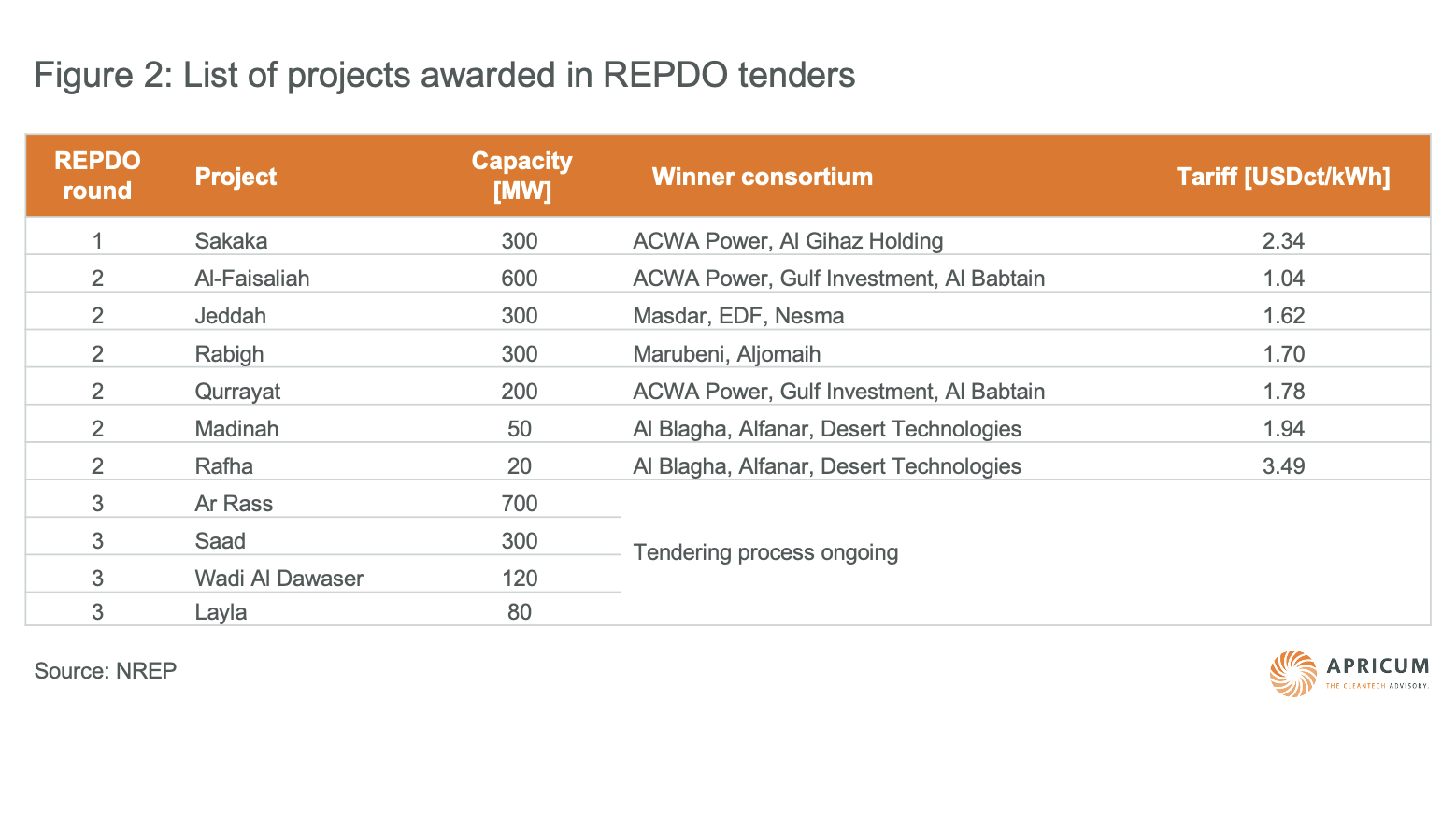

Last year, however, was a slow one for the Kingdom in terms of PV deployment where almost no capacity increases materialized. Following this stall in the industry, the crown prince announced the signing of PPAs for seven PV projects – six of which were from the delayed second round of REPDO (Renewable Energy Development Office) tenders. REPDO has most recently announced the shortlisted bidders for the projects but has not reported any further developments so far. With the addition of the ACWA Power-led 1.5 GW Sudair project, these seven projects will contribute almost 3 GW of solar PV installations.

NREP maps out two main paths for increasing the installed PV capacity: tenders and direct agreements. 30% of the target capacity is expected to be awarded via tenders by REPDO. The Kingdom’s first large-scale PV project (the 300 MW Sakaka) for instance, was awarded a 25-year PPA from the first round of the tenders in 2018.

Most recently, REPDO received bids for the third round for four projects with a total capacity of 1.2 GW. NREP also includes direct bilateral agreements with developers and the Public Investment Fund (PIF) to develop and build large PV projects. The 1.5 GW Sudair project is an example of such projects and many more are expected in the future. Direct agreement projects will make up 70% of the targeted capacity.

Although PV development in the Kingdom has been entirely driven by utility-scale projects, rooftop PV also has large potential. Currently, 50% of the electricity consumption in Saudi Arabia is from the residential sector, with 70% of this used for cooling requirements. This creates an excellent match between electricity consumption and PV generation.

In 2020, Saudi Arabia enacted a law allowing the installation of rooftop systems of up to 2 MW in size. This ushers in a potential gigawatt‑scale market with the right legislative environment.

Oman

Oman

Oman has set the target of sourcing 11% of electricity from renewables by 2023, and 30% by 2030. Even though it is one of the countries with the highest solar densities in the region, it has only very recently joined the solar PV world. Its installed capacity is expected to rapidly increase through bilateral agreements and solar tenders run by the Oman Power and Water Procurement Company (OPWP).

Oman’s first utility‑scale PV project will be the 500 MW Ibri II PV plant. This project is close to completion and is being developed on a build-own-operate (BOO) basis by ACWA Power (50%), Gulf Investment Corporation (40%) and Alternative Energy Projects Co. (10%) with a 15-year PPA for an undisclosed amount.

This year should see the tendering of two large PV projects in Oman – bids were submitted for the Manah I & II projects, both of which will have a capacity of 500–600 MW. A shortlist of nine companies has been revealed with OWPW awarding each project to a separate developer.

Kuwait

In the north of the Gulf, Kuwait has so far struggled to implement its PV plans but is now showing efforts to revive the market in the country. Kuwait aims to have 15% of its installed electricity generation capacity coming from renewable sources by 2030. Like the other countries in the region, PV development is dependent on the public sector.

Similar to Dubai’s MBR solar park, Kuwait plans to install PV in the Shagaya Solar Park. The first phase of the park successfully deployed 70 MW of power generation capacity (50 MW CSP, 10 MW PV, 10 MW onshore wind) in 2012.

The much larger second phase, the Al Dibdibah project, was initially set to comprise mostly CSP but was later changed to just PV. The first bids were received in 2019. However, the tender was cancelled in 2020 due to the Covid-19 pandemic. The latest plan is to revive the project, but no official declaration has been made yet. Phase three with mixed technology, known as Al Abrag, is expected to be tendered in several packages. The anticipated capacity is 1,200 MW of PV, 200 MW of CSP and 100 MW of wind.

Kuwait is reviewing a plan to reduce government subsidies for electricity tariffs and has independent institutional programs to encourage rooftop solar, which is now required on all government buildings thus spurring a market for small‑scale solar contracting.

Schemes and regulations for small-scale solar rooftop are being reviewed though the impact and uptake of such schemes will be limited without tariff subsidy removal. It is expected that the delay in the Kuwaiti solar market will soon end, with the country trying to catch up on its renewables targets and keep up with the other GCC countries.

Turkey

Unlike the Gulf countries, Turkey has the opposite motivation to ramp up its renewable efforts. The considerable impact of energy imports on the nation’s current account deficit has directed Turkey to look for ways to generate electricity using domestic sources.

To diversify the imported natural gas dependent energy mix, Turkey provided subsidies for the development of renewable energy. So far, the total installed PV capacity is around 7 GW. The country is aiming to increase the share of renewables within the overall energy consumption to 20.5% by 2023.

The earliest driver for the development of PV was the YEKDEM support scheme established in 2011. Legislation awarded the lucrative 13.3 USDct/kWh purchase tariff for 10 years for all unlicensed PV systems under 1 MW that could obtain a connection permit from the grid operator.

However, the legislation also intentionally allowed for the development of sites next to each other and this led to many collective projects in the range of 5-10 MW that are legally many separate entities with 1 MW capacity, but a single PV plant in reality. This type of unlicensed project development is set to stay as the most common way in the country until the grid connection points are exhausted.

The Ministry of Energy and Natural Resources increased the eligible capacity without a license to 5 MW but decreased the support to 32 kurus/kWh (~3.7 USDct/kWh).

Turkey’s first large tender for solar PV, YEKA GES-1, was held in 2017. Turkish Kalyon Enerji and Korean Hanwha consortium (Hanwha has since left) has been awarded the right to build a 1 GW PV plant in Karapinar at a 6.99 USDct/kWh tariff with a 15-year PPA. As one of the tender conditions, PV panel manufacturing must be established in Turkey and the components locally sourced. The Karapinar project is currently generating electricity at 20% capacity and is expected to be fully functional by the end of 2022.

Turkey cancelled the YEKA GES-2 project, which had an identical structure to the previous tender and instead opted for a different tendering structure for the next PV tender, YEKA GES-3 or Mini YEKA. Instead of a large single site, 74 sites are being tendered separately for a total capacity of 1 GW. Each site has a capacity of either 10, 15, or 20 MW.

After being delayed multiple times due to Covid-19, projects are being awarded in the highly oversubscribed tender in Q2 2021 with the lowest bid being 18.2 kurus/kWh (~2.08 USDct/kWh). Projects will receive a 15-year PPA and be subject to a 70% local content requirement for the PV modules used.

Apricum has been active in the Middle East region for more than a decade and is ready to support both local and international clients in seizing the opportunities arising from the emerging renewable energy market. For enquiries, please contact Apricum Managing Partner Nikolai Dobrott.

* The article was amended on June 30, 2021, to correct the following figure: “The plant is backed by Marubeni and JinkoSolar and has a 25-year power purchase agreement (PPA) with a tariff of 2.42 USDct/kWh.” The correct figure is “2.94 USDct/kWh.”

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Wow, the scales of solar panels are breathtaking