Higher PV module prices may point to stable demand and more sustainable pricing trends

The former Trina Solar Chief Scientist has been a forceful voice for the sustainability of PV cell and module materials as the industry grows towards gigawatt scale. Veteran solar researcher Pierre J Verlinden has pointed to silver and indium at the consumption levels in high-efficiency heterojunction cells.

Verlinden’s work on this issue has been advanced in additional work conducted by University of New South Wales (UNSW) researchers.

Additionally, he has argued that sustainability in solar pricing should be considered. He says that if race-to-the-bottom pricing prevails, PV cell and module makers will be unable to invest in R&D to advance PV technology, nor will they have the financial wherewithal to honor warranties.

So, with prices trending from US$0.21/Wp in 2020 up to US$0.33/Wp in 2021, as reported by Rystad Energy, does it make for more favorable market conditions and long-term business sustainability for PV cell and module manufacturers? Indeed, with the analyst predicting that module prices will surge to US$0.41/Wp in 2022 it could be argued that a new era of more sustainable pricing is emerging.

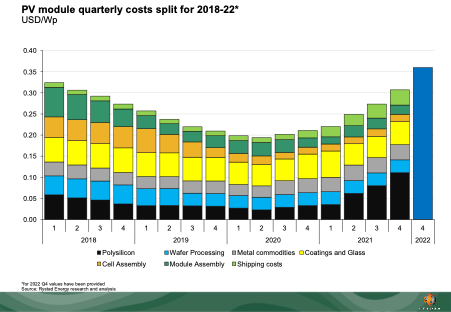

Breaking down costs

A closer look at PV cell and module costs, however, reveals that even with higher prices, margins may remain slim, with manufacturers continuing to be squeezed.

In November, Rystad Energy produced an analysis investigating price trends and cost drivers. It concluded that commodity prices across the board have been significantly driving up costs.

“For the modules some of the key ones, polysilicon, silver, copper, aluminum, and glass [which have gone up in cost],” said Dave Dixon, a senior analyst, renewables for Rystad Energy.

Further upstream, the news is worse. PV wafer and cell producers have had to grapple with the biggest cost increase, in the form of polysilicon – with prices surging throughout the year.

“Polysilicon just blows everything out the water,” says Dixon. The raw feedstock for crystalline silicon ingots and wafers increased by 175% in the first six months of 2021 alone. And while new capacity is set to come online, many see high prices continuing through at least the first half of 2022.

These developments are a particularly bitter pill for PV cell and module makers to swallow, as they have made impressive progress in driving manufacturing costs out of their operations.

“There are three key bars [of the chart above] that have come down rapidly – and that is module assemble, cell processing, and wafer processing,” said Dixon. “Module suppliers have done an excellent job in reducing their costs, also thrifting with their commodity inputs.

“We are now at a stage where manufacturing makes roughly 30% of module costs, while inputs comprise around 70% of the cost and those are out of control for the manufacturers,” he continues.

Given these dynamics, higher PV module prices primarily appear to be the result of surging commodity prices, polysilicon chief among them – far from a sustainable outcome.

A significant caveat to this analysis, however, is that end-market demand remains strong. Burgeoning PV rooftop demand, coupled with government and corporate efforts to decarbonize accelerating, market peaks, and troughs – the latter often the precursor to rapid price declines – appear to be a thing of the past.

Rystad expects some 270GW of renewable energy installations, across all technologies, to be achieved in 2022.

Please login to comment

[…] because raw materials account for 60 percent to 70 percent of the costs to manufacture both solar panels and […]

[…] as a result of minerals alone represent over half the price of fabricating batteries and photo voltaic modules, and about 20% for wind […]

[…] because raw materials account for 60 percent to 70 percent of the cost to manufacture both solar panels and […]

[…] Source: (PV Magazine, 2022) […]

[…] because raw materials account for 60 percent to 70 percent of the cost to manufacture both solar panels and […]

[…] because raw materials account for 60 percent to 70 percent of the costs to manufacture both solar panels and […]

[…] because raw materials account for 60 percent to 70 percent of the costs to manufacture both solar panels and batteries. The United States depends on imports for all of its supply of 17 minerals and […]

[…] Higher PV module prices may point to stable demand and more sustainable pricing trends. Website: https://www.pv-magazine.com/2022/01/04/higher-pv-module-prices-may-point-to-stable-demand-and-more-s…. Last accessed: […]

[…] efficacy has reduced solar module production costs so much that commodity inputs now make up about 70% of the overall price of modules. These inputs include not only copper, silver, and aluminum but also, in no small irony, coal. The […]

[…] “So, with prices trending from US$0.21/Wp in 2020 up to US$0.33/Wp in 2021, as reported by Rystad Energy, does it make for more favorable market conditions and long-term business sustainability for PV cell and module manufacturers? Indeed, with the analyst predicting that module prices will surge to US$0.41/Wp in 2022 it could be argued that a new era of more sustainable pricing is emerging.” https://www.pv-magazine.com/2022/01/04/higher-pv-module-prices-may-point-to-stable-demand-and-more-s… […]

[…] Gifford, J. (04/01/2022). Higher PV module prices may point to stable demand and more sustainable pricing trends. PV Magazine International. Visitado el […]