From pv magazine India

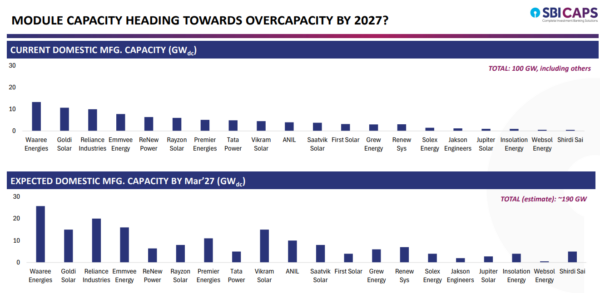

India’s solar module manufacturing capacity has reached about 100 GW, enough to meet annual domestic demand assuming an effective utilization-to-nameplate ratio of 55% to 65%, according to a report by SBICAPS. However, with total module capacity projected to rise to 190 GW by March 2027, concerns of oversupply are emerging, particularly amid shrinking export opportunities, especially to the United States.

Solar power installations in India rose 60% year-on-year in fiscal year 2025, reaching roughly 24 GW. This required about 50 GW DC of modules, based on typical DC/AC overloading ratios of 1.2 to 1.4. The report estimates annual additions will rise to 40 GW to 50 GW through fiscal year 2030 to meet the country’s solar targets, implying a steady-state need of around 100 GW of module manufacturing capacity.

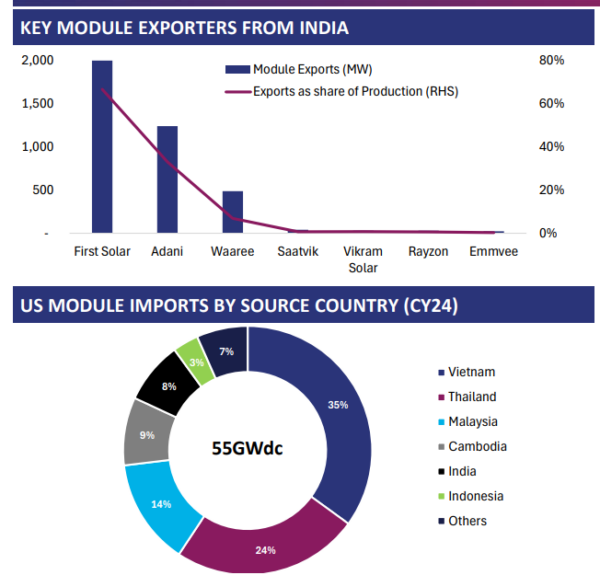

However, with cumulative capacity expected to reach 190 GW by 2027 and export prospects narrowing – particularly following recent US policy changes – an oversupply scenario appears likely. India exported just 4 GW of modules in fiscal year 2025, a year-on-year decline largely attributed to regulatory changes in the United States.

“US administration issued a directive to halt funding from the IRA. The subsequent enactment of the ‘One Big Beautiful Bill’ is expected to phase out investment tax credits and production tax credits for solar and wind projects,” the report notes. “This has reduced exports of modules from India to the US – the major export destination for Indian modules. In response, some players are setting up factories there, to adjust to the new FEOC (Foreign Entity of Concern) rules,” said the report.

Contrasting the maturity in modules, solar cell capacity in India is just 26 GW DC – less than one-third of module capacity – implying import dependence in the near term. However, the report highlights that cell capacity is set to grow rapidly with the implementation of ALMM-II.

Under the ALMM-II order, only cells from approved manufacturers may be used for projects with bid submissions after Aug. 31, 2025.

Additionally, only ALMM cells and modules may be used for projects benefiting from net metering or open access rules, a move that will open up the significant commercial and industrial market to domestic players.

Planned capacity additions are expected to take cell capacity close to self-sufficiency in the medium term, with total 115 GW DC of cell capacity projected by March 31, 2027. In the interim, higher prices for DCR cells could push up project costs until supply-demand dynamics readjust, potentially reducing bid enthusiasm.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.