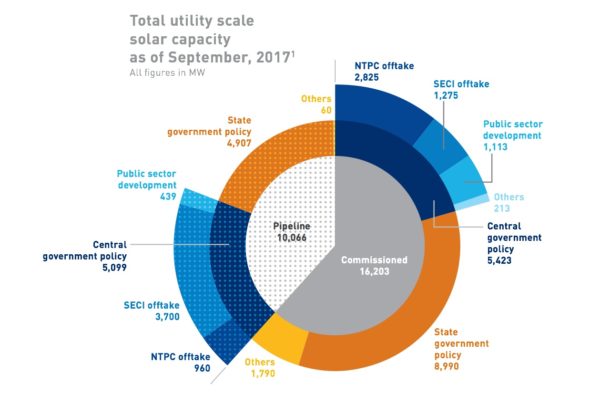

India's total utility scale solar capacity reached to 16.2 GW in September 2017. The enormous growth is demonstrated by the fact, that 84 % of the installations were added in the last 4 quarters, in total 7.5 GW. Additionally, 10 GW of solar capacity have been allocated to developers, According to Bridge to India's India Solar map 2017 September edition.

Southern states have emerged as top performers with a 57% share in the added capacity. Among them, Telangana has surpassed Rajasthan, Andhra Pradesh and Tamil Nadu, to become India's top state for Solar deployment. Also 62% of pipeline projects are concentrated in Tamil Nadu, Andhra Pradesh and Karnataka.

Graphics: Bridge to India

“It is a curious time for solar sector in India”, sais Vinay Rustagi, Managing Director of Bridge to India. “We are coming off a period of exceptional growth of 80% over last 3 years.” The tariffs have fallen to a low of INR 2.44/kwh ($0.03/kWh) level, “making solar power the cheapest source of power in India”. Nevertheless he is sceptical that the growth will continue in this way. “The future looks subdued”, he adds.“ He expects that utility scale capacity addition will slow down to about 5 GW per annum. One consequence could be that investors shift their attention to the secondary market where, where Bridge to India observes some large M&A transactions are in pipeline.

Discuss quality at REI

Greenko and ReNew Power emerged as top developers according to basis of capacity commissioned during last 4 quarters. ACME has increased its ranking to 3rd position. Project developers NTPC, Azure, Adani, Mahindra Susten follow these 3. India's 7 project developers now have the portfolio of more than 1 GW (commissioned and pipeline). Trina solar with 16.6% market share, JA solar with 9.2 % market share followed by Canadian Solar with 8.75% market share dominate the Indian market with.

On the domestic manufacturing side, according to the report, Waaree was the biggest manufacturer last year, followed by Vikram Solar and Tata Power Solar. There has been a marginal increase in the market share of Indian manufacturers but the Chinese suppliers continue to hold over 80% of the total market share, sais Bridge to India.

In the inverter market, ABB is dominating with 26.7% market share and has retained its position as the top inverter supplier. As pv magazine has recently reported, the company has big plans for the future and is going to supply the solar inverters for solar projects at 750 railway stations in India. Also, TMEIC and SMA have significant market share with around 15% each.

Author: Ajinkya Waradpande

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.