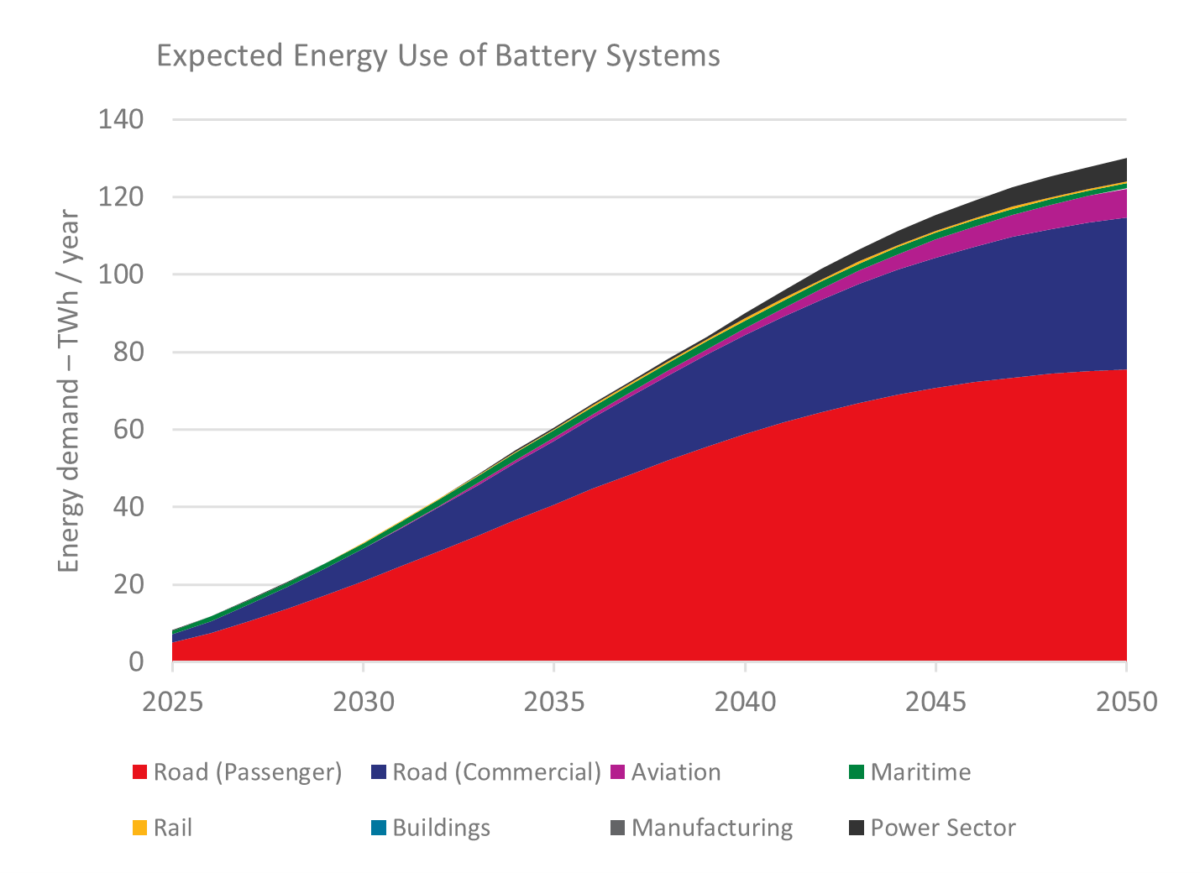

Based upon current government policy positions, total energy carried by battery energy storage systems (BESS) and hydrogen technology (including hydrogen derived fuels) in the future UK energy system will increase rapidly to reach approximately 130 TWh and 105 TWh respectively per year by 2050, according to a new report.

However, considerable uncertainties remain in the relative adoption of both technologies, according to “The Role of Hydrogen and Batteries in Delivering Net Zero in the UK by 2050,” which was authored by Norway's DNV and commissioned by UK-based Faraday Institution.

“Batteries and hydrogen have distinct characteristics and should largely be viewed as complementary rather than competing technologies,” says Faraday Institution CEO Pam Thomas. “Both will require significant technological advance and extensive scale up of manufacturing and deployment if the UK is to meet its obligation to reach net zero by 2050. The varying timescales of their rollout leads to considerable uncertainties in predicted market share profiles over time.”

Specifically, the uptake of the two technologies in different sectors, including: road vehicles, aviation, maritime, rail, built environment, manufacturing and power, will be impacted by the rate of technology development, infrastructure development, capital costs, total cost of ownership, customer perceptions and other policy factors, the report finds.

The primary use of battery technology is focused on road transport, accounting for 88% of all battery usage by 2050 with aviation and the power sector making up most of the remaining energy use, the report finds. Only limited use of batteries is expected in the rail and maritime sectors, and no significant use in manufacturing or the built environment, with vehicle-to-grid (V2G) and behind-the-meter solar PV applications captured within the power sector.

For hydrogen, the use of energy is more evenly distributed with aviation, maritime, and manufacturing providing 79% of all hydrogen use by 2050, in addition to contributions from road transport and the power sector. The overlap between batteries and hydrogen is expected to be limited in the power sector, with hydrogen used to balance demand over a longer seasonal period.

Popular content

Utility-scale BESS is forecasted by DNV to increase to 24 GW, with average energy duration of BESS modelled to increase from one hour today to almost four hours by 2050, in addition to 45 GW of V2G energy storage coming from electric vehicles.

However, DNV’s calculation is looking conservative when compared with recent figures released by Norwegian consultancy Rystad Energy, which expects 24 GW of utility-scale batteries to be installed already by the end of this decade and attracting investments of up to $20 billion.

“Large-scale battery developments will soon be the norm in the UK, solving the problem of balancing short-term power demand with the intermittency of wind and solar generation. And this could just be the start. Further growth could soon be on the way if the government introduces additional incentives to spur investments,” says Pratheeksha R, renewable energy analyst at Rystad Energy.

Of the 4.7 GW of installed energy storage capacity in the UK today, BESS account for about 2.1 GW. Most of the current capacity, 2.8 GW, comes from pumped hydro storage. The UK government is eyeing 30 GW of capacity by 2030, including batteries, flywheel, pumped hydro, and liquid air energy storage.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.