From pv magazine USA

SEMA’s “Inflection Point: The State of U.S. PV Solar Manufacturing & What’s Next” report shines a spotlight on the need for policy changes to further support the US solar supply chain.

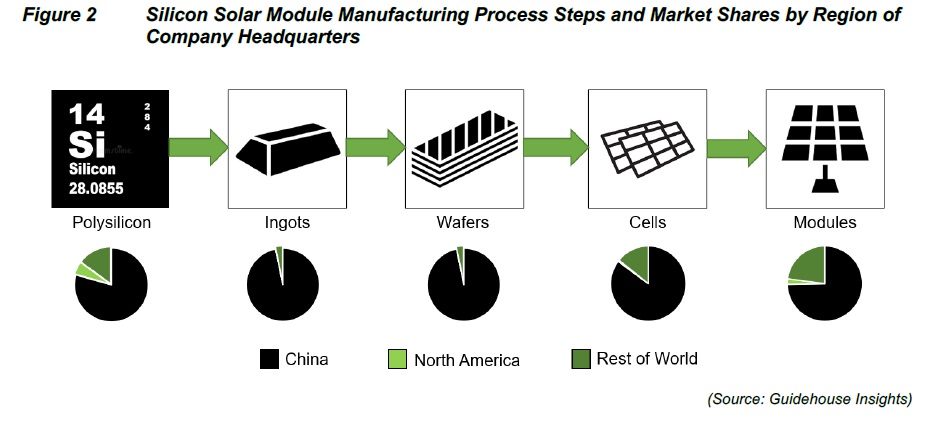

The US Inflation Reduction Act (IRA) has motivated solar module manufacturers to build manufacturing facilities in the United States. However, very few factories are planned for the production of ingots, wafers and cells. This shortage leaves US solar module makers beholden to imports, mainly from China.

“Thanks to the efforts of Congress and the Administration, with the Inflation Reduction Act we have an opportunity to build a sustainable, strong American supply chain for solar that will make sure our country isn’t dependent on China for this critical energy resource,” said SEMA Coalition Executive Director Mike Carr. “This report shows that if we actually want a clean energy future in this country, we will require a continuing whole-of-government effort that doesn’t allow our trading adversaries to derail the reshoring effort.”

The report points out that China is producing most of the polysilicon and wafers needed to make solar modules, producing 99% of the world’s solar wafer and more than 80% of the world’s polysilicon. PV manufacturing advisory Exawatt, now a part of CRU Group, reported that the only notable ingot and wafer production hub outside of China is in Southeast Asia, with a capacity of 35 GW of wafer facilities, potentially expanding to 45 GW by the end of 2024.

SEMA sees onshoring the full solar supply chain as important for energy security and it keeps the US solar industry from suffering from global supply chain disruptions, as experienced during the height of the pandemic. Furthermore, onshoring the full supply chain brings jobs and ensures higher labor standards are applied, in addition to use of cleaner production methods.

The IRA includes tax credit adders for domestic content; however, it also excludes the origin of polysilicon and wafers. The SEMA report calls for policymakers to set “strong standards for getting bonus tax credits for using domestic content and federal procurement in order to incentivize investment in the high-value, capital-intensive parts of the supply chain such as wafer and polysilicon production.” The report authors see the need to enforce the Uyghur Forced Labor Prevention Act and anti-dumping trade laws, which they claim are necessary in order to level the playing field for domestic producers.

In addition to policy changes and trade law enforcement, SEMA recommends that the US government set an example by insisting that any power producers from which the government procures energy from must purchase solar modules with US-made components.

“Solar manufacturers in America are operating well below their full potential because the government is facilitating an over-reliance on China and failing to provide a level playing field to help fuel investment and innovation,” said Carr. “The CHIPS Act and the IRA were game-changing in the tools they provided to the Administration, but they must use the tools to their full effect to break China’s monopoly by onshoring the entire solar supply chain.”

The US solar supply chain is in its early stages with polysilicon facilities currently in Michigan, Tennessee, and Washington, which the SEMA report says could produce enough polysilicon to make about 20 GW of crystalline silicon products each year. However, the country has few facilities to make ingots, wafer and cells.

“These manufacturing steps are the most capital intensive yet among the least incentivized through the provisions in the IRA,” the report notes.

With stronger support for the early stages of the process, US module manufacturers would be less dependent on imports from Chinese-owned companies for these materials.

Alongside Qcells and Norsun, Convalt Energy, which are manufacturing wafers in the United States, CubicPV and India’s Vikram Solar have announced plans to set up shop in the country. Whether the announced factories will come to fruition or not is in question. Exawatt Head of PV Alex Barrows is skeptical.

“I think we’ll get a bit [of ingot and wafer capacity] in the U.S. but nowhere near what has been announced,” said Barrows. “Thirty-five gigawatts of capacity by the end of 2026 has been announced, but I would actually suspect it is more likely that 15 GW to 20 GW will be installed.”

Suniva is one company that plans to begin producing solar cells in its plant in Georgia, and Heliene just signed a three-year contract with Suniva, with plans for made-in-America modules. Suniva is restarting a factory it idled in 2017 when it declared bankruptcy, claiming it could not compete with cheap solar imports. SolarWorld joined Suniva in filing the Section 201 trade petition that prompted the Trump administration to impose duties in 2018 on imported solar cells and panels for a period of four years.

US Treasury Secretary Janet Yellen visited the Suniva factory recently, joining the SEMA Coalition, which is asking the Biden administration to level the playing field for the solar industry by expanding the definition of what makes up domestic content to include the upstream materials.

“We cannot have a sustainable solar manufacturing sector in this country until we break China’s monopoly on wafer supply, which gives cell manufacturers no alternatives,” said Carr. “As intended by the congressional authors of the IRA in recent letters, Treasury should break this monopoly, and spur US wafer manufacturing by refining their guidance for the IRA’s domestic content bonus. We hope they do it quickly.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

3 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.