2017: The PV year in review

Overall, the solar PV industry continued to go from strength to strength, with 2017 recording many impressive developments and world-firsts. The biggest news came from China, where its unparalleled installation activity surpassed even the most optimistic of forecasts. Mexico’s record-breaking low auction price was another dominant headline this year, although it was overshadowed by news of insolvency by the two biggest U.S. solar manufacturers, Suniva and SolarWorld, and their subsequent Section 201 trade case.

In the technology realm, monosilicon’s stellar rise to become the dominant module type was definitively a highlight, although half cut cells drew a lot of attention too. On the back of the news that NexWafe attracted even more funding, kerfless wafers are a technology to watch in the coming years.

Read on to discover how the year in solar PV unfolded month by month, and what 2018 is expected to bring:

Cheap as chips

The first month of 2017 brought with it news that solar is on course to become the world’s cheapest source of energy within the next 10 years. The dramatically falling costs from the supply chain to the final product could see the average global price become cheaper than coal within the next 10 years, according to Bloomberg New Energy Finance (BNEF).

A number of hot stories hit the headlines in February, thus breaking the doom and gloom of, arguably, the worst month of the year, including the news that SolarCity would be marketed under the Tesla brand. The announcement came two months after Tesla’s shareholders voted to acquire the U.S. residential solar PV rooftop company.

In the anti-dumping arena, it was announced that the European Commission would propose shorter AD tariffs on Chinese solar firms. An 18 month tariff period proposal was put to the 28 EU Member States. They had just under a month to decide whether to approve the move or not.

Days later, Mexico signed the lowest solar contract to date. Overall, contracts were signed for 1.8 GW, including one at a price of US$26.99/MWh by Fotowatio. The median price for solar in this auction was around $31.70/MWh – the lowest to date in the world.

Not to be outdone, Armenia announced it would make its first foray into the world of solar, with a 40 to 50 MW PV power plant. Over the year, the country saw a flurry of activity – the latest news in December was that work had been completed on Armenia’s third large-scale solar PV plant – with plans for 2018 accelerating development further.

Emerging markets

Flickr:

Hichem Merouche

Continuing the theme of emerging markets, March saw lots of activity in the large-scale project sector, including news of four bidders for Turkey’s 1 GW Konya solar PV plant. Overall, the country aims to install 5 GW of PV by 2023. To date, it has installed around 1 GW. Algeria also announced it would launch a tender for the construction of large-scale PV projects totaling 4 GW. The tender will be held in three 1,350 MW phases and will select projects with an average capacity of 100 MW.

The European Commission also confirmed an 18-month extension of antidumping and anti-subsidy tariffs, with a staged phase-out, after conducting an investigation among member nations in February.

Battle lines drawn

April was characterized by news of impending trade wars. U.S.-based Suniva dominated headlines with the announcements that (i) two weeks after laying off 131 employees without notice and closing its module plant in Michigan, one of the largest U.S. manufacturers filed for chapter 11 bankruptcy; and (ii) it submitted a petition under Sections 201 and 202 of the U.S. Trade Act of 1974.

The petition calls for “global safeguard relief” from imports of crystalline silicon solar PV cells and modules, which it says have driven the company to bankruptcy. Just before all this kicked off, the Turkish Government announced a list of China-based PV manufacturers who will be subject to antidumping fees for PV imports.

Most read

Image: SolarWorld Americas

The most read story of the year – SolarWorld’s insolvency in May – followed Suniva’s April announcement by just weeks, and shortly preceded SolarWorld’s decision to join Suniva’s trade petition. Unsurprisingly, SolarWorld CEO, Frank Asbeck pointed to the role of “illegal price dumping” by Chinese producers in the company’s downfall. SolarWorld has led the charge against what it characterized as unfair competition from Chinese producers in both the EU and the U.S.

A ray of light in the trade case darkness, analysts at Frost & Sullivan forecast that solar will attract more investment than coal, gas and nuclear combined this year. The report, titled the Global Power Industry Outlook 2017 deduced that renewable power investment will reach $243.1 billion globally in 2017, with solar PV investment comprising $141.6 billion of that total.

Falling prices

Image: GT Research

A Q1 report by GTM Research and Solar Energy Industries Association (SEIA) released in June found U.S. PV system price declines across all sectors, following collapses in component pricing. Fixed-tilt utility-scale systems broke the US$1 per watt barrier for the first time during the quarter. They also noted that average module prices fell by a third from Q2 to Q4 2016, to land at $0.39 per watt in the fourth quarter, and only rebounded to $0.40 per watt during Q1.

Meanwhile, in the energy storage sector, a study by McKinsey found that energy storage is already cost-competitive in the commercial sector. With battery-pack costs now down to less than $230/kWh – compared to around $1,000/kWh as recently as 2010 – storage uptake is on the rise across Europe, Asia and the U.S.

Summer sun

To many people in Europe, the height of summer is inextricably linked to Spain, where seemingly half of the continent’s population decamps to in July. The eyes of the PV world were certainly fixed on Spain this month, after the government published details of its renewable energy auction, which saw more than 3.5 GW of capacity allocated to solar projects. In what was termed “an historical day for the PV sector”, the gusto with which developers swooped into Spain served as a timely – and for some, painful – reminder of the vast solar-power potential in this sun-drenched nation.

Image: The Summit 2013 – Picture by Dan Taylor / Heisenberg Media – http://www.heisenbergmedia.com

Australia, another sun-soaked country on the other side of the world, also turned heads thanks to the star power of a certain Elon Musk and his pledge to build the world’s largest battery in South Australia in under 100 days, otherwise Tesla would do it for free. Was he successful? Read on …

Solkiss, meanwhile, said it would build the world’s largest rotating solar plant in South Korea, a 2.67 MW floating solar farm on the Deoku Reservoir. It didn’t say when it expected the project to be completed, however.

GW-izz

The month of the gigawatts: In India, the Ministry of New and Renewable Energy (MNRE) unveiled welcome plans to support 7.5 GW of domestic solar manufacturing capacity; in Argentina, a 1.2 GW renewables tender was launched with solar performing strongly, and back Down Under, Equis Energy secured approval to build a 1 GW solar farm in Queensland. August was also the month in which Ikea teamed up with Solarcentury to announce the launch of a home battery system in the U.K.

Solar dazzles, despite Trump

Image: Wikimedia/Gage Skidmore

Although just a few months have passed since September, it already seems like a more innocent time. The Section 201 case had proven only superficially deleterious to the U.S. solar industry over the summer, but a report by Axios found that President Donald Trump would be “90% likely” to impose tariffs on module manufacturers if the U.S. International Trade Commission (USITC) were to recommend them. Fast forward a few weeks, and the USITC had found “serious injury” in the Section 201 case, setting the U.S. on course for the all-but inevitable introduction of AD duties.

September also saw Tesla begin producing solar cells at its Buffalo gigafactory – a not-insignificant development in the U.S. manufacturing landscape, while in the U.K., Drax announced its plans to build a 200 MW battery storage project at a former coalmine. With coal undoubtedly on the decline, this month also saw the publication of a World Nuclear Industry Status Report that laid bare an inconvenient truth for green energy opponents: renewables aren’t just crushing coal; they’re also trouncing nuclear.

Cash to burn

$5 billion: that’s how much money it took for Global Infrastructure Partners (GIP) to purchase Equis Energy the Singapore-based solar and wind power developer. A record-breaking sum for the sector, the deal set the scene for an October that appeared to be swimming in cash, not least in Saudi Arabia.

The oil-rich kingdom was very active in PV this month, unveiling details of a low-cost 300 MW solar tender and a 3 GW solar and storage project to be developed by Japan’s Softbank Vision Fund. Just over the border in the UAE, meanwhile, Abu Dhabi-headquartered IRENA published a report that suggested solar costs will fall 60% over the next decade.

The Chile winds blow…

After receiving 24 bids in its 2.2 GWh renewable electricity tender, Chile’s government confirmed in November that the winning bid was just $21.48/MWh, submitted by Enel Generacion Chile. To put that stunning price into perspective, the lowest bid received in a similar renewable tender offered in 2016, was $47.6/MWh.

Image: UNDP

Apropos of this, a report by consultancy Lazard, published in late November found that the global cost of utility-scale solar has reached an unsubsidized LCOE of less than $50/MWh, placing PV at scale as the second-cheapest form of new energy generation behind wind, which can deliver at $45/MWh. “In some scenarios the full- lifecycle costs of building and operating renewables-based projects have dropped below the operating costs alone of conventional generation technologies such as coal or nuclear,” said a press release by Lazard.

Finally, according to BNEF, China is on track to install a massive 51-54 GW this year. The world’s biggest solar market reportedly installed 43 GW of solar power in the first nine months of 2017, following an installation rush in the first half of the year ahead of the June 30 FIT reduction deadline.

Comings and goings

Image: Lightsource BP

As December draws to a close, and with it 2017, the month has thrown up a timely reminder of the solar industry’s one certainty – that nothing is certain. Oil giant BP was a long-forgotten fossil of the solar sector; a former heavyweight, some might argue PV pioneer, that turned its back on a shaky solar industry in 2011. Few thought the British company would ever return. But return it did, and in some style too – snapping up the U.K.’s dynamic developer Lightsource for a cool $200 million. BP will give module manufacturing a wide berth this time, focusing instead on building and operating solar plants globally.

ET Solar Inc. experienced rather different fortunes this month, with the firm quietly filing for bankruptcy midway through December. In more bullish news, France’s EDF launched an ambitious 30 GW solar plan that will likely be executed exclusively in France between 2020 and 2035.

The new legal framework for anti-dumping, designed to protect the EU against unfair trade practices was also signed, and came into force on December 20. Across in the U.S., reports stated an unreleased memo circulating within the White House lays out arguments for the strongest of trade sanctions against Chinese solar module makers in what is likely a bad sign for U.S. solar markets.

And finally, yes – Musk made it (was there ever any doubt): on December 1, Tesla commissioned its 100 MW battery in South Australia, completing the project in an impressive 60 days.

And now to the future …

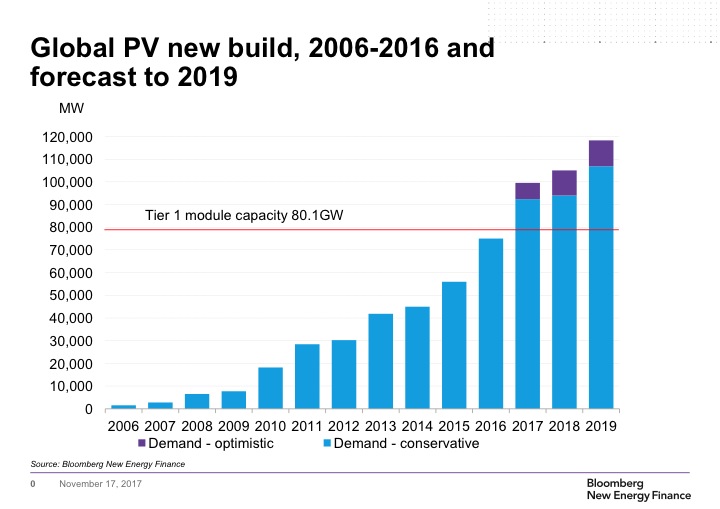

IHS Markit is predicting another recording breaking year for solar in 2018, forecasting installations to hit 108 GW by the end of the year. The analysts state that continued demand from China will be the key driver behind this growth, as the country has successfully diversified its market and achieved strong momentum in the distributed generation segment.

Question marks remain over other leading PV markets, as the U.S. industry awaits the President’s final decision in the section 201 case, and India mulls the introduction of anti-dumping duties.

BNEF has predicted similar installation numbers. With stabilization of the polysilicon market expected, improved cost-efficiencies on the upstream side and increased efforts to meet 2020 energy targets in Europe, demand in 2018 should be between 94 and 111 GW; and 107 and 121 GW in 2019, it said.

BNEF has predicted similar installation numbers. With stabilization of the polysilicon market expected, improved cost-efficiencies on the upstream side and increased efforts to meet 2020 energy targets in Europe, demand in 2018 should be between 94 and 111 GW; and 107 and 121 GW in 2019, it said.

Boom

It also notes that there is currently a global polysilicon factory boom underway, by both new and existing players, with a total 167kT of new capacity planned by the end of 2018. These include Korea’s OCI, an established player, and China-based East Hope, a new entrant, Jenny Chase, head of Solar Analysis at BNEF told pv magazine.

Overall, supply is forecast to increase 10% in 2018, at around 490,000 tons – enough for 118 GW of crystalline silicon PV modules. In comparison, 2017 is expected to see the production of 445,600 metric tons of polysilicon, a 13% increase on 2016.

Module prices, meanwhile, are expected to drop to as low as US$0.30/W for market leaders. With limited movement on polysilicon prices in H1 2018, the report adds, market leaders can expect to see H1 prices of around $0.33/W (Based on 10% gross margin), and $0.30/W by mid-year.

Image: BNEF

Trending

Analyst Corrine Lin outlined her panel predictions for 2018. She sees four major trends: (i) trade wars will affect the market; (ii) there will be no more poly or wafer shortages; diamond and black silicon will drive down costs; and both PERC and half-cut modules will hit the mainstream.

Six trends that will shape the inverter landscape in 2018, meanwhile, according to IHS Markit, include: (i) a continuing Chinese dominance; (ii) a hardening of the module level power electronics (MLPE) landscape, and evolution of growth strategies; (iii) modular design that will make central solutions attractive; and (iv) the threat of component shortages.

A lot is set to happen on the policy front, too, around the globe. Nothing is certain though and, as in 2017, when China pulled a rabbit out of its installation hat, there is potential for anything to happen. pv magazine looks forward to delivering you the newest trends, developments and markets going forward.

Thank you for your support!

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: [email protected].

Please login to comment

[…] the second half of 2017, ReneSola Ltd grid connected over 90 MW of rooftop PV projects in China. The company owns 70 MW, […]

One constant in the PV forecasting landscape: growth will slow down next year, honest. They have always said this, and usually have been wrong.

Who is looking after CSP solar? This site is about PV, but CSP has survived and its despatchability is attracting increasing attention. It deserves systematic tracking.

The photo of the Sahara is pretty but misleading. You can’t build anything on sand dunes. As it happens more than half of the megadesert is stony plains (hamada) not dunes (ergs). The former are available for solar of any type.

Excellent recap of the wild 2017 solar market ride. Agree the big takeaways were the number of large, > .25 GW level projects at incredibly competitive pricing, and in second half of year, impacts of tariffs in USA, India, and other markets. On applications side, trackers have really achieved market acceptance. thx Shug

[…] 2017: The PV year in review (pv-magazine.com) […]

[…] delayed or further delayed. This compares with China’s “eye watering installation rates” (PV Magazine) of solar capacity, as it added over 50 GW to its grid. Even taking into account lower […]